LUT

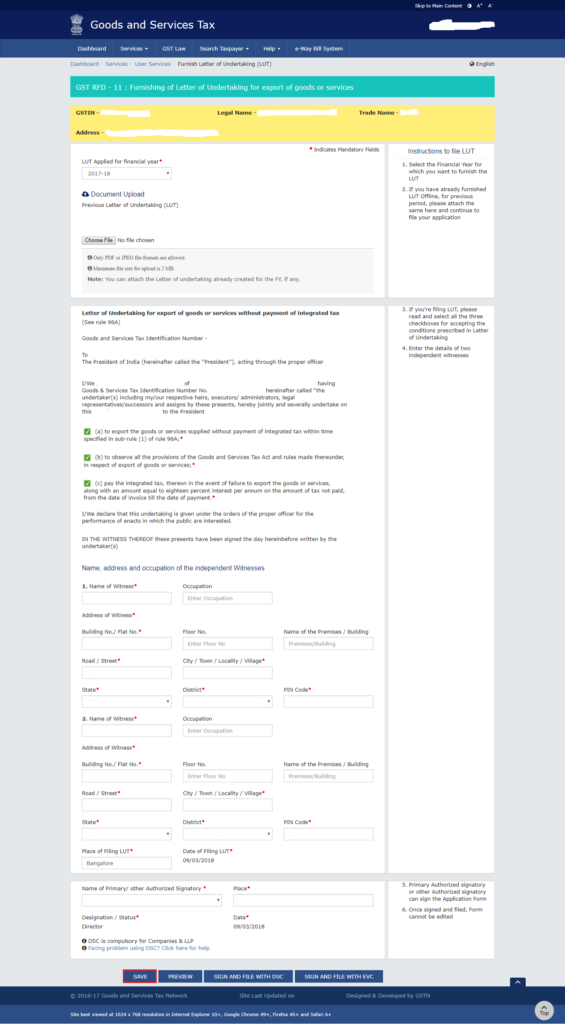

Introduction Are you a business owner involved in exporting goods or services? If so, you must be familiar with the complexities of Goods and Services Tax (GST) compliance. Among the various aspects of GST, the Letter of Undertaking (LUT) plays a significant role in facilitating exports. In this comprehensive guide, we will demystify the concept […]

section 276B of Income Tax act 1961

Failure to pay tax to the credit of Central Government under Chapter XII-D or XVII-B If a person fails to 64[***],— (a) 65[pay to the credit of the Central Government, the tax deducted] at source by him as required by or under the provisions of Chapter XVII-B; or 66[(b) “pay tax or ensure payment of tax to the credit […]

section 276AB of Income Tax act 1961

Failure to comply with the provisions of sections 269UC, 269UE and 269UL Whoever fails to comply with the provisions of section 269UC or fails to surrender or deliver possession of the property under sub-section (2) of section 269UE or contravenes the provisions of sub-section (2) of section 269UL shall be punishable with rigorous imprisonment for a term which may extend to […]

section 276AA of Income Tax act 1961

Failure to comply with the provisions of section 269AB or section 269-I [Omitted by the Finance Act, 1986, w.e.f. 1-10-1986. Original section was inserted by the Income-tax (Amendment) Act, 1981, w.e.f. 1-7-1982.]

section 276A of Income Tax act 1961

Failure to comply with the provisions of sub-sections (1) and (3) of section 178 If a person— (i) fails to give the notice in accordance with sub-section (1) of section 178; or (ii) fails to set aside the amount as required by sub-section (3) of that section; or (iii) parts with any of the assets of […]

section 276 of Income Tax act 1961

Removal, concealment, transfer or delivery of property to thwart tax recovery Whoever fraudulently removes, conceals, transfers or delivers to any person, any property or any interest therein, intending thereby to prevent that property or interest therein from being taken in execution of a certificate under the provisions of the Second Schedule shall be punishable with […]

section 275B of Income Tax act 1961

Failure to comply with the provisions of clause (iib) of sub-section (1) of section 132 If a person who is required to afford the authorised officer the necessary facility to inspect the books of account or other documents, as required under clause (iib) of sub-section (1) of section 132, fails to afford such facility to the […]

section 275A of Income Tax act 1961

Contravention of order made under sub-section (3) of section 132 Whoever contravenes any order referred to in the second proviso to sub- section (1) or sub-section (3) of section 132 shall be punishable with rigorous imprisonment which may extend to two years and shall also be liable to fine.

section 275 of Income Tax act 1961

Bar of limitation for imposing penalties (1) No order imposing a penalty under this Chapter shall be passed— (a) in a case where the relevant assessment or other order is the subject-matter of an appeal to the58-59[Joint Commissioner (Appeals) or to the] Commissioner (Appeals) under section 246 or section 246A or an appeal to the Appellate Tribunal under section 253, after […]

section 274 of Income Tax act 1961

Procedure (1) No order imposing a penalty under this Chapter shall be made unless the assessee has been heard, or has been given a reasonable opportunity of being heard. (2) No order imposing a penalty under this Chapter shall be made— (a) by the Income-tax Officer, where the penalty exceeds ten thousand rupees; (b) by […]