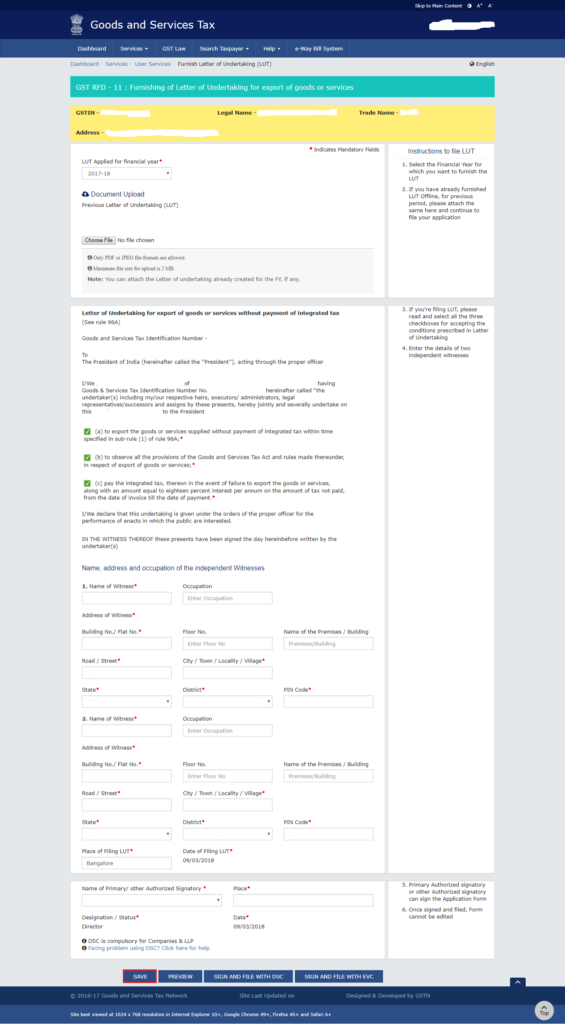

Introduction Are you a business owner involved in exporting goods or services? If so, you must be familiar with the complexities of Goods and Services Tax (GST) compliance. Among the various aspects of GST, the Letter of Undertaking (LUT) plays a significant role in facilitating exports. In this comprehensive guide, we will demystify the concept of LUT under GST and shed light on the process of filing Form GST RFD-11. So, let’s delve into the world of LUT under GST and equip ourselves with the knowledge necessary to navigate this vital aspect of export bonding. What does LUT under GST mean? The Letter of Undertaking (LUT) is a crucial document that serves as an alternative to the payment of Integrated Goods and Services Tax (IGST) on exports. Under GST, exporters can opt to furnish an LUT instead of paying the IGST at the time of exporting goods or services. This undertaking assures the authorities that the exporter will fulfill their obligations and adhere to the provisions of the GST Act. Who needs to file LUT in Form GST RFD-11? Not all exporters are required to file an LUT. It is essential to understand the eligibility criteria to determine whether you need to file an LUT in Form GST RFD-11. Here are the key points to consider: Exporters of goods or services: If your business is engaged in the export of goods or services, you may be eligible to file an LUT. Exporters with no tax liabilities: To qualify for filing an LUT, your business should have a record of compliance and have no tax liabilities or pending arrears. Registered under GST: You must be a registered taxpayer under the GST regime to apply for an LUT. No prosecution initiated: If there is no prosecution initiated against you or any of your partners, directors, or proprietors, you can proceed with filing an LUT. It is crucial to assess your eligibility carefully to ensure compliance with the GST provisions and avoid any legal implications. Documents Required for LUT under GST When filing an LUT in Form GST RFD-11, certain documents need to be furnished to complete the process. Here is a list of essential documents required: GST Registration Certificate: A copy of your GST registration certificate is necessary to establish your eligibility for filing an LUT. Bank Account Details: You will need to provide the bank account details, including the account number and IFSC code, for the purpose of verification and validation. PAN Card: Your Permanent Account Number (PAN) card, which serves as a unique identifier, is a mandatory document when filing an LUT. Undertaking on Letterhead: A signed undertaking on your business’s letterhead, stating that you will abide by the provisions of the GST Act and fulfill all export-related obligations, is an essential part of the documentation. Export Invoice and Shipping Bill: Copies of export invoices and shipping bills are required to substantiate your export activities and establish your involvement in the export of goods or services. Ensuring you have these documents readily available will streamline the process of filing an LUT and help you avoid unnecessary delays or complications. Process for Filing LUT in GST Now that we have a clear understanding of the Eligibility for Filing LUT in GST, let’s dive into the step-by-step process of filing an LUT in GST: Prepare the LUT form: Begin by downloading Form GST RFD-11, the official form for filing an LUT. Ensure that you have the latest version of the form to avoid any discrepancies. Fill in the required details: Provide all the necessary information in the LUT form, such as your business’s name, address, GSTIN (Goods and Services Tax Identification Number), and details of authorized signatories. It is crucial to fill in the form accurately and double-check all the information to avoid any errors. Attach supporting documents: Gather the documents mentioned earlier, such as your GST registration certificate, bank account details, PAN card, undertaking on letterhead, and copies of export invoices and shipping bills. Make sure to attach these documents along with the filled LUT form. Submit the form: Once you have completed the LUT form and attached the supporting documents, it’s time to submit the application. Submit the form physically or electronically, depending on the prescribed mode of submission in your jurisdiction. Verification and approval: After submitting the LUT form, the tax authorities will verify the information provided and examine the supporting documents. If everything is in order, they will approve your LUT application. You may receive an acknowledgment or confirmation of approval from the authorities. Validity period and renewal: A valid LUT is typically granted for a specific period, such as one financial year. It is essential to keep track of the validity period and renew the LUT before it expires to ensure uninterrupted export activities. It is worth noting that the exact process and requirements may vary slightly depending on the specific jurisdiction and applicable rules. Therefore, it is advisable to consult with a tax professional or refer to the official GST guidelines for accurate and up-to-date information. FAQs (Frequently Asked Questions) Q: Can I file an LUT if I have pending tax arrears? A: No, to be eligible for filing an LUT, your business should have no tax liabilities or pending arrears. Q: Is an LUT mandatory for all exporters? A: No, an LUT is not mandatory for all exporters. It is required for those who meet the eligibility criteria and wish to avail the benefit of not paying IGST at the time of export. Q: How long does it take to get an LUT approved? A: The processing time for LUT approval may vary depending on the tax authorities and their workload. It is advisable to submit the application well in advance to allow for any necessary processing time. Q: Can I make amendments to the LUT after it has been approved? A: Yes, you can make amendments to the LUT if required. In such cases, it is recommended to inform the tax authorities and