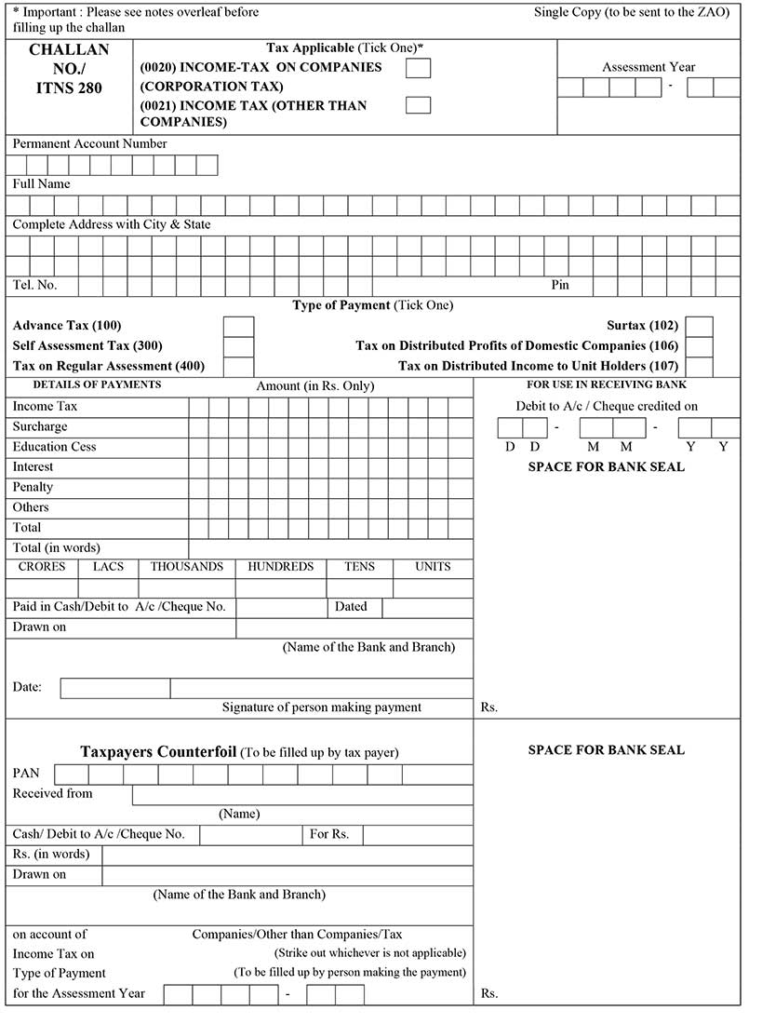

Challan 280

Introduction Income tax payment is a vital component of every taxpayer’s life. Whether you are a salaried employee or a business owner, you need to pay your taxes on time to avoid any penalties or legal complications. One of the most popular methods for making income tax payment is using Challan 280. Challan 280 is a form that taxpayers can use to pay their income tax dues. In this blog, we will cover everything you need to know about Challan 280, including its procedure, verification of payment, correction of details, and more. What is Challan 280? Challan 280 is a form used for income tax payment. It is used by taxpayers who are not required to pay their taxes through TDS (Tax Deducted at Source). It is used to pay taxes such as advance tax, self-assessment tax, or regular assessment tax. Procedure for Making Income Tax Payment using Challan 280 The procedure for making income tax payment using Challan 280 is straightforward. Here are the steps you need to follow: Download Challan 280: You can download Challan 280 from the official website of the Income Tax Department or NSDL. You need to select the appropriate assessment year, type of payment, and mode of payment. Once you have filled in the required details, you can download the Challan 280 form in PDF format. Fill in the Details: The next step is to fill in the details required in the Challan 280 form. You need to fill in your name, address, PAN, and assessment year. You also need to mention the type of payment you are making, such as advance tax, self-assessment tax, or regular assessment tax. Calculate Tax Amount: After filling in the required details, you need to calculate the tax amount that you need to pay. You can use the tax calculator available on the Income Tax Department’s website to calculate the tax amount. Make the Payment: Once you have filled in all the required details and calculated the tax amount, you can make the payment. You can make the payment using any of the available modes such as net banking, debit card, credit card, or through a bank. Proof of Payment of Tax: After making the payment, you need to keep a copy of the Challan 280 form as proof of payment of tax. Verification of Challan Tax Payment Once you have made the payment using Challan 280, you need to verify the payment to ensure that it has been credited to your account. Here are the steps you need to follow to verify the payment: Visit the NSDL website: You need to visit the NSDL website and select the “Challan Status Inquiry” option. Enter the Required Details: You need to enter the required details such as your Challan Identification Number (CIN), your PAN, and the assessment year. Verify the Payment: After entering the required details, you can verify the payment status. If the payment has been credited to your account, you will see the payment details such as the amount, date of payment, and mode of payment. Correction of Details If you have made a mistake while filling in the details of Challan 280, you can correct it. Here are the steps you need to follow to correct the details: Visit the NSDL website: You need to visit the NSDL website and select the “Online Correction” option. Enter the Required Details Fill in the Correct Details: After entering the required details, you need to fill in the correct details. You can make corrections in the name, address, PAN, or any other details as required. Submit the Correction: Once you have filled in the correct details, you can submit the correction. After submission, you will receive a confirmation message on your registered mobile number and email address. FAQs Q. Can I use Challan 280 for all types of tax payments? A. No, Challan 280 can be used only for income tax payments such as advance tax, self-assessment tax, or regular assessment tax. Q. Can I make an online payment using Challan 280? A. Yes, you can make an online payment using Challan 280. You can use any of the available modes such as net banking, debit card, credit card, or through a bank. Q. How can I verify my tax payment using Challan 280? A. You can verify your tax payment using Challan 280 by visiting the NSDL website and selecting the “Challan Status Inquiry” option. Enter the required details such as your Challan Identification Number (CIN), your PAN, and the assessment year to verify the payment. Q. Can I correct the details of Challan 280 after making the payment? A. Yes, you can correct the details of Challan 280 after making the payment. You need to visit the NSDL website and select the “Online Correction” option. Enter the required details and fill in the correct details to submit the correction. Conclusion Challan 280 is a popular form used for income tax payment by taxpayers who are not required to pay their taxes through TDS. The procedure for making income tax payment using Challan 280 is straightforward, and you can make the payment using any of the available modes such as net banking, debit card, credit card, or through a bank. After making the payment, you need to keep a copy of the Challan 280 form as proof of payment of tax. You can verify the payment using the NSDL website and correct the details if required. By following the steps mentioned in this blog, you can easily make yo