Section 65 – Arbitration And Conciliation Act, 1996

Submission of statements to conciliator

Section 65 – Arbitration And Conciliation Act, 1996 Read More »

Chartered Accountants

Chartered Accountants

Submission of statements to conciliator

Section 65 – Arbitration And Conciliation Act, 1996 Read More »

Appointment of conciliators

Section 64 – Arbitration And Conciliation Act, 1996 Read More »

Saving Notwithstanding anything contained in section 61, any conciliation proceeding initiated in pursuance of sections 61 to 81 of this Act as in force before the commencement of the Mediation Act, 2023, shall be continued as such, as if the Mediation Act, 2023, had not been enacted.

Section 62 – Arbitration And Conciliation Act, 1996 Read More »

All the employees covered under the EPF scheme now have the option to switch to NPS scheme in order to use a number of tax benefits and savings that are applicable under NPS. It is best to compare and analyse the different features of the two options. Employees that are currently covered under the EPF scheme have the option to shift to the NPS scheme and make use of the attractive tax benefits and savings that apply under NPS. Introduction Employee Provident Fund (EPF) and National Pension Scheme (NPS) are essential retirement savings tools for employees that help them build a tax-efficient retirement corpus. These two schemes focus on one objective of creating a corpus for the employees but differ on four parameters: flexibility, risk, returns, and tax. If an employee plans smartly with either or a combination of both, he can retire with a handsome corpus. This choice of NPS v. EPS or both depends on Age and Salary EPF v. NPS EPF is a scheme run by the Employee’s Provident Fund Organization (EPFO) to provide employees with social security and retirement benefits. Employers must register with the EPFO and make an EPF contribution if they employ a workforce of 20 or more whose monthly salary is up to Rs. 15,000. Nonetheless, an employer can voluntarily contribute to the EPF regardless of his obligations due to the non-fulfilment of these conditions. When an employer or employee chooses to contribute to the EPF scheme, 12% of the basic salary (plus dearness allowance) is deducted from an employee’s monthly salary and credited to his PF account. The employer also matches the similar contribution, paid out of his coffers, in the employee’s PF and pension account in the proportion of 3.67% and 8.33%, respectively. The employer has to allocate an additional 0.50% of the employee’s salary to the Employee’s Deposit Linked Insurance Scheme (EDLI) and 0.50% towards the administrative charges. Where the employee’s salary exceeds Rs. 15,000 per month, the employer’s contribution to the pension account is limited to 8.33% of a Rs. 15,000 salary. Therefore, only 8.33% of Rs. 15,000 is contributed to the pension account, while any additional contribution goes into the PF account. NPS is also a voluntary retirement savings scheme administered and regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Unlike EPS, any Indian citizen, employee or self-employed, can join NPS individually or as part of an employee-employer group. The NPS provides flexibility in choosing investments in equity, government bonds or corporate debentures. It also allows subscribers to choose Pension Fund Managers (PFMs) to manage their investments. Subscribers can switch between investment options and fund managers and choose the investment composition from Active or Auto. NPS provides two types of accounts to the subscribers – Tier I and Tier II. Tier I is a mandatory retirement account, whereas Tier II is a voluntary savings account. Unlike Tier I account, Tier II offers greater flexibility in terms of withdrawal. There is no maximum limit on the amount one can invest in Tier I of the National Pension System (NPS) each year. However, a minimum of Rs. 1,000 must be invested every year. Partial Withdrawal The EPF allows employees to withdraw partially during service for specified purposes. Partial withdrawal is allowed after five years for purchasing or repairing a house, seven years for marriage or education, and ten years for paying an existing debt. However, there is no lock-in period for withdrawals in case of medical emergencies or for disabilities. Under the National Pension System (NPS), subscribers must have a mandatory subscription period of 3 years for partial withdrawal only for specified purposes of higher education, marriage, home purchase, specified illnesses, and medical expenses due to disability. EPF members can make partial withdrawals within the limits set by EPFO for each specific purpose, while NPS subscribers can withdraw up to 25% of their NPS contribution at the point of such withdrawal. In NPS, subscribers are allowed a maximum of three partial withdrawals throughout the tenure. In contrast, the number of withdrawals in EPF varies depending on the purpose of the withdrawal. Maturity and Pre-Maturity Exit EPFO allows members to withdraw total funds from the EPF account in the event of superannuation or death. Further, a member can withdraw his entire contribution (including interest) if he has been unemployed for at least two months. However, the contribution to the EPS cannot be withdrawn as it is converted into an annuity to pay a monthly pension. When a subscriber exits from the NPS upon attaining the age of 60 or on superannuation, a complete lump sum withdrawal is allowed if the corpus is up to Rs. 5 lakhs. If the corpus is more than Rs. 5 lakhs, 40% is invested in the annuity to pay the monthly pension, and the remaining 60% is paid as a lump sum. When a subscriber opts for the pre-mature exit from NPS, the withdrawal limit depends on the corpus size. A complete lump sum withdrawal is allowed if the corpus is up to Rs. 2.5 lakhs. If the corpus is more than Rs. 2.5 lakhs, 80% of the corpus is invested in the annuity to pay the monthly pension, and the remaining 20% is paid as a lump sum. For pre-mature exit, a subscriber (with no employee-employer relationship) must have completed a five-year mandatory subscription period of 5 years. EPF vs NPS Rate of returns: NPS returns vary based on the market conditions for stocks and bonds. NPS returns also vary depending on the ratio of investment options and exposure to equity, medium fixed income securities and low fixed income securities. Average returns for NPS investment of 85% in fixed income securities, and 15% in equities is: 2012 – 2013: 9.76% 2013 – 2014: 5.37% 2014 – December 2015: 19.63% From the launch of the NPS scheme: 10.35% Rate of returns: The average EPF rate of returns is between 8.00% – 8.50% Liquidity and withdrawals: Funds cannot be withdrawn until the contributor attains the age of 60. Partial

A national permit is a document issued by the transport authority to indicate that a commercial vehicle is authorised for goods carriage across the country. State governments can issue two different permits for goods carriage: state permits and national permits. Central Motor Vehicles Rules, 1989 Section 86: Application for national permitAn application for the grant of a national permit shall be made in Form 48 to the transport authority. Section 87: Form, contents and duration of authorisation Subsection (1): An application for the grant of an authorisation for a national permit shall be made in Form 46 and shall be accompanied by a fee of ₹1000 per annum in the form of a bank draft. Subsection (2):Every authorisation shall be granted in Form 23-A, in case the certificate of registration is issued on Smart Card or shall be granted in Form 47, in case the authorisation is in paper document subject to the payment of consolidated fees of ₹16500 per annum to be deposited in the national permit account for the permit granted to operate throughout the territory of India. The period of validity of an authorisation shall not exceed one year at a time. What is a Motor Vehicle Permit? A permit is a legal document issued with a motor vehicle and is a mandatory requirement for all those who drive commercial or transport vehicles. Transport authorities check for these permits while highway patrolling as per the Motor Vehicle Act 1988. What are the Different Types of Motor Vehicle Permits? Good Vehicles National Permits: If vehicles move out of their home state, then the vehicle is issued with permits for four states along with home state. For approval of the permit, it is essential to ensure that the age of the goods vehicles should not more than 12 years and age of multi-axle vehicle should not be more than 15 years. Good Carriers: Vehicle can run outside the state if this permit is issued provided the vehicle carries goods. Counter Signature of Good Carriers Permits: This permit is applicable in other states no matter where it is issued from. But Delhi does not issue this permit for those vehicles that do not run on clean fuel and weigh more than 7500 kilograms. Passenger Vehicles Eco-friendly Sewa: This is issued to three-wheeler vehicle with capacity of 11 with driver and runs on battery. Permit for Maxi Cab: This permit is issued in Delhi and the charges are directed by STA to those vehicles with capacity less than 13. Permits for Chartered Buses: Rental vehicles are issued with permits and a contract is signed between the operator and permit holder. This permit requires the driver to have a list of passengers and the vehicle must run on a definite route. Auto Rickshaw and Taxi Permit for Vehicles: This permit is issued in Delhi which allows autorickshaws to impose tariff and calculates the bill as per meter. Phat-Phat Sewa: Vehicle carrying 10 people along with driver and running on a particular route is issued with this permit. Temporary Basis Permits: This type of permit is issued on specific conditions such as: Vehicle running beyond city limit carrying passengers of any religious affair or resolution Vehicle running for any clinical business Vehicle applying for permit renewal Applying for this permit for a motor cab, following conditions should be fulfilled: White vehicle Sitting capacity of five Adequate parking space Booking office with telephone If finances were required by the owner for buying this vehicle Permits for Stage Carriages: All India Tourist Permit (AITP): This permit is provided to the tourist bus depending upon the following conditions: Vehicle must be a white luxury bus Must have 5 cm long blue ribbon at the middle of the body of the bus Both the edges of the bus must have the word ‘Tourist’ School Buses or Institutions: Golden-yellow vehicles owned by educational institutions are exempt from road tax. Permit for Rent-a-cab: Delhi Government issues this permit to private buses and vehicles under Delhi Transport Corporation that travels on various routes in the city. The following are the conditions to get this permit: Should have adequate parking space Passenger tax to be paid where the vehicle runs within the state Should have 24-hour telephone Owner must have minimum of 50 cars on their name out of which 50% should be air-conditioned Requirement for National Permit To obtain National Permit, the owner of the vehicle must make an application to the concerned State Regional Transport Authority. In many States, there is a restriction placed on the age of the vehicle for which National Permit is sought. National Permit can be obtained only for vehicles less than 12 years old. Documents Required for National Permit Registration Certificate of the vehicle. Fitness Certificate of the vehicle. Insurance Certificate of the vehicle. Proof of payment of tax for the current Quarter to the Home State . Fee for National Permit. Demand drafts drawn in favour of the Authorities prescribed in respect of other states towards payment of composite taxes. Payment of green tax wherever applicable. Application Submission Procedure Step 1: Visit the relevant RTO office. Step 2: Obtain the required application forms from the RTO and fill them out with your details. Step 3: Submit the form along with address and identity proof. Step 4: Pay the required fee. Step 5: The RTO authorities will process your application. Step 6: The vehicle’s condition, body, seating arrangements, and other details will be included in the permit and handled by the RTO authorities. Step 7: The application will then be processed further after the vehicle has been examined for appropriateness and compliance with other essential conditions. FAQs Who should be opting for a permit? Any individual who is a registered owner of any transport vehicle can opt for a permit subject to the restrictions as per the notification of the Government. What are the different forms which are required for application of a permit? The different forms which are required for the application of a permit are prescribed under the Motor Vehicles Rules. They are Form 45, Form 46, Form PCA, Form

National Permit Online Read More »

Sec 194Q introduced in the finance act 2021 to cover the high volume transaction in the ambit of TDS. Under this section the buyer is liable to deduct tax on the purchase of goods exceeding threshold limit. The primary motive of this section is to increase transparency and be able to track large transactions. What is Section 194Q of Income Tax Act? Section 194Q of Income Tax Act, 1961 was introduced on July 1, 2021, by the Central Board of Direct Taxes. This section deals with the Tax Deducted at Source on the purchase of goods. It is predominantly a buyer-specific section that specifies the TDS provisions for buyers who purchase goods from Indian sellers. Under section 194Q, buyers having purchases exceeding 50 lakhs in a previous year will have to pay a TDS at the rate of 0.1%. However, the same is not applicable to purchases made from a seller outside India. Let’s take an example –Mr. A., located in Delhi, bought goods worth 60 lakhs from Mr. B in Rajasthan in the previous year. Since the purchases exceed the threshold of INR 50 lakhs, the TDS will be calculated on (60 lakhs – 50 lakhs), i.e., 10 lakhs @ 0.1%. Who does Section 194Q of the Income Tax Act apply to? Section 194Q is applicable to buyers making purchases in India in the following cases – Any buyer with a total turnover, gross receipts, or sales exceeding 10 crores in the previous financial year. The buyer purchases goods from an Indian seller and is liable to make payment to a resident Indian seller. The payment made should be for the purchase of goods exceeding the aggregate value of 50 lakhs. The introduction of section 194Q helps the government to trace the huge amount of transactions without compliance of various tax provisions and to identify the cases of under disclosure of Income What is the role of GST in Section 194Q? GST is excluded from the calculation of turnover GST is included in the calculation of TDS at the rate of 0.1% When to deduct TDS? Particulars Applicability/ Non-applicability of TDS u/s 194Q TDS is deducted at the time of credit of the amount in the account of the seller; and Agreement/ contract between buyer and seller indicates GST component separately. TDS provisions u/s 194Q will not be applicable to the GST component. When TDS has been deducted on the payment basis (as payment is earlier than credit) TDS provisions u/s 194Q will apply to the GST component (i.e. TDS is deductible on the whole amount) Non-furnishing of PAN If a seller does not furnish Permanent Account Number (PAN) to the buyer, deductible tax at source (TDS) would be at 5% instead of 0.1%. **Without PAN, the applicable tax rate in other cases is 20%. For Section 194Q, the TDS rate is 5%.** TDS Return: Form 26Q The due date for filing a TDS return is July 31, October 31, January 31, and May 31, respectively, for a quarter ending 30th June, 30th September, 31th December, and 31st March. What Happens If You Fail to Comply With Section 194Q of the Income Tax Act? If you fail to comply with the provisions and requirements of section 194Q of the Income Tax Act, it might attract severe penalties and consequences. Given below are the penalties for non-compliance on section 194Q – If the buyer does not deduct TDS, it attracts a penalty under section 40A (IA). As per this section, if the buyer fails to deduct TDS, 30% of the total purchases on which TDS has not been deducted will be disallowed as an expense. Consequently, this 30% will be treated as your income and will be liable to tax. 30% of the total purchases will be clubbed into your net income and taxed along with your total income. Exemptions Available Under Section 194Q of the Income Tax Act If the buyer does not primarily reside in India and the goods purchased are not directly connected with India, the buyer does not have to deduct TDS. The buyer does not need to deduct TDS in the year of incorporation. For example, if your company has been incorporated in the current financial year, you are not required to deduct TDS. If the buyer purchases products from a seller whose income is exempt from tax, then the buyer does not have to deduct TDS. If the tax is deducted under section 206C, excep31str transactions on which 206C(1H) is applicable, Such transaction shall not be taxable under section 194Q. Any purchases made by the central or state government institutions are not required to deduct TDS. If any transaction attracts both section 194Q and section 194O, tax shall be deducted under section 194O by the e-commerce platform provider. However, if the e-commerce platform fails to deduct the TDS, the buyer is responsible for the same. If a stock exchange purchases goods or commodities, it is exempted from deducting TDS. Transactions involving renewable energy and electricity are also exempted from deducting TDS. When The Person Is Liable To Deduct TDS? The person being the buyer will deduct TDS at the time which is earlier of the following: At the time of credit of such sum to the account of the seller. At the time of payment which is obtain in any mode. TDS Rate The tax deduction at source(TDS) is deducted at 1% on the purchase of goods if the seller has its PAN If the seller does not hold PAN then 5% TDS will be deducted. Due Date Of Depositing TDS With Government The due date for TDS payment is always the 7th day of the next month, with a few exceptions. For example, if an organization wants to pay TDS for the month of July, then the TDS payment due date for the same will be the 7th of August.For the month of March, the due date will be 30th April. Due Dates Of Returns Quarter Period Due date Q1 April – June 31st July Q2 July –

TDS Under Section 194Q of the Income Tax Act, 1961 Read More »

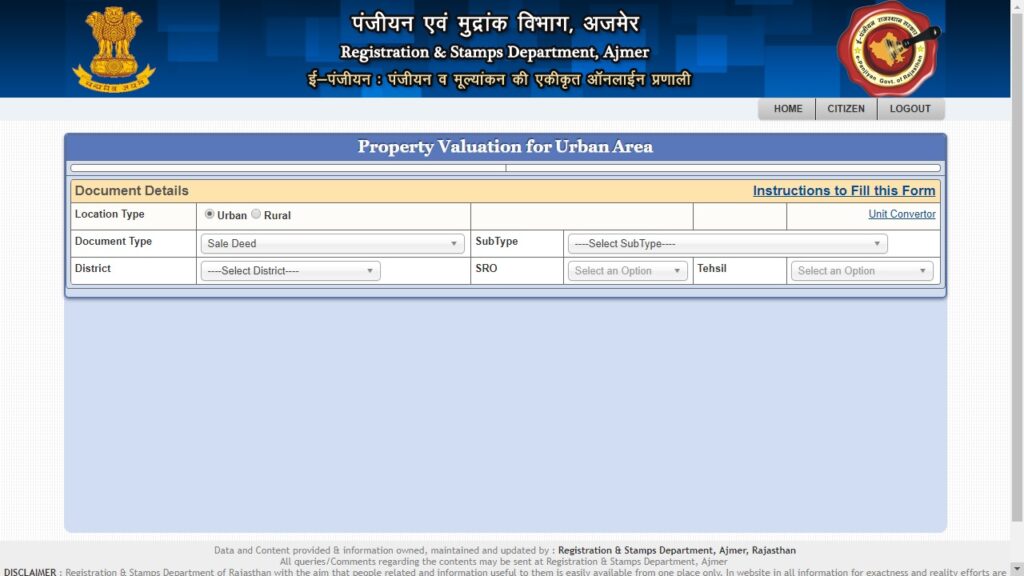

E-panjiyan is the official portal of the Inspector-General of Registration and Stamps (IGRS) of the Rajasthan government, which oversees the property transactions in the State. As per the Rajasthan Registration Act 1955, every property transaction should be registered on the E-panjiyan Rajasthan that holds the digital records of property transfers and registrations. E-panjiyan also provides a plethora of services, such as land records, and encumbrance certificates, among others. Rajasthan Registration Act, 1955 Section 17 of the Rajasthan Registration Act Compulsory registration is provided under the Section 17 of Rajasthan Registration Act such as Instruments of the gift of immovable property, lease of immovable property for any term exceeding one year and Instruments which create or relinquish any right and immovable property of a value of more than Rs.100. Section 18 of the Registration Act Optional registration is provided under Section 18 of the Registration Act: Lease of immovable property for any term not exceeding one year Instruments other than wills which purport or operate to create, declare, assign, limit or extinguish any right, title or interest to movable property Wills Purpose of Property Registration (Deed registration) The document of transfer will be a permanent public record once the property is registered with the office of Sub-Registrar Any citizen can inspect this public record, and a certified copy of the document can be obtained from the Sub-Registrar office Registration of property is providing information to the general public that the ownership has transferred by the owner to the buyer If a citizen plans to buy a property, he or she can verify the record-index available in the sub-Registrar office. A citizen can ascertain in whose name the last transfer deed has been registered What is stamp duty Rajasthan 2024? Stamp duty Rajasthan is the amount that has to be paid by the buyer when he enters into a property transaction in Rajasthan. The Rajasthan Stamps Act of 1908 controls the stamp duty in Rajasthan. The stamp duty in Rajasthan depends on the circle rate in the state. The stamp duty Rajasthan comes under the purview of E-Panjiyan, the registration and stamps department in Rajasthan. As per Section 10 of the Rajasthan Stamps Act, stamp duty in Rajasthan can be paid using adhesive stamps, impressed stamps and franking machine. Stamp duty in Rajasthan Gender Stamp duty Registration charges Total registry charges Men 6% + 20% (of 6%) labour cess 1% 8.2% Women 5% + 20% (of 5%) labour cess 1% 7% Documents Required for Property Registration Proof of Ownership Certified Copy Of Original Old Sale Deed Assessment Of MC or Mutation Release Deed for identification of the ancestral property Lease deed for any term exceeding one year. Proof of Identification PAN Card Form 60 Chain document Photograph of the applicant Verification of GPA from where the property has been registered in case property has been registered out of state NOC – if needed ID Proof of two witness parties Map Plan and description of immovable property Property Registration through e-Panjiyan website Access e-panjiyan portal Step 1: For registering property in Rajasthan visit official website of Registration and Stamp department- epanjiyan. Step 2: Select the property valuation option from the home page. In the new page, enter mobile number and verification code. Click on fresh valuation for registering immovable property. Document Details Step 3: In the document details section, the applicant has to provide the property location type. Select document type as sale deed and subtype as a certificate of the sale deed. Provide District, SRO and Tehsil details. Location Details Step 4: The applicant has to provide the following location details for registering the property: Colony Area Zone Category Type – Commercial or Residential Location – Interior or exterior – DLC rate will be calculated based on this location information Road width in feet Plot or Khasra number Address Details Corner plot detail Property area in Feet – The applicant can use a unit converter for conversion of property area into feet unit Addition Values Step 5: In addition values section, the applicant has to provide details of construction (if applicable) such as floor type, constructed area, type or year. Step 6: Boundary value details such as Length, Tinshade, area, parking details, Tube well details need to be furnished. Based on these values, the property amount will be calculated. Commission Details Step 7: By selecting the appropriate commission (Jail/Senior citizen/others/NA), the commission value will be calculated and displayed on the screen. Land Value Calculation Step 8: After entering all details, click on “Save property details”, by clicking on this option, the system will auto-generate or calculate the Land value based on the plot area and land values. Land value will appear on the screen. After verifying the land value, click on the Next button. Stamp Duty Calculation Step 9: By clicking on the Next button, the applicant will reach the stamp duty page. They have to provide details of the Execution Date, Face value and Evaluate value (will be shown). After providing the details, click on calculate stamp duty. Note: Stamp duty and registration fee details will be displayed. In addition to registration and stamp duty charges, the applicant has to pay the following fees: Stamp duty payable Surcharge Registration fee CSI Penalty if any Step 10: Sum of these fees can be paid for the registration of property in Rajasthan. Click on save button for further preceding the application. Party Details Step 11: By clicking on ‘Proceed for Party Details’ option, the applicant can provide the details of parties such as party type, presenter type, party name, Gender, Category, Contact number ID proof and Address. Upload Documents Step 12: In upload documents, the applicant has to upload all supporting documents. Take a print out of these forms, after providing details scan the documents in PDF format for uploading. Step 13: Click on upload and save button after uploading the documents. Once finished click on ‘done and exist’. Pay Stamp Duty through e-GRAS Step 14: On clicking on the Payment option, the link will be redirected to the e-GRAS page. If the applicant is an already registered user, Login to the

Rajasthan Property Registration Read More »

The Public distribution system (PDS) is an Indian food Security System established under the Ministry of Consumer Affairs, Food, and Public Distribution. PDS evolved as a system of management of scarcity through distribution of food grains at affordable prices. PDS is operated under the joint responsibility of the Central and the StateGovernments. The Central Government, through Food Corporation of India (FCI), has assumed the responsibility for procurement, storage, transportation and bulk allocation of food grains to the State Governments. The operational responsibilities including allocation within the State, identification of eligible families, issue of Ration Cards and supervision of the functioning of Fair Price Shops (FPSs) etc., rest with the State Governments. Under the PDS, presently the commodities namely wheat, rice, sugar and kerosene are being allocated to the States/UTs for distribution. Some States/UTs also distribute additional items of mass consumption through the PDS outlets such as pulses, edible oils, iodized salt, spices, etc. What is Targeted PDS? Targeted Public Distribution System (TPDS) is jointly operated by Central and State Governments. The Targeted Public Distribution System (TPDS) came into operation in June 1997 under the Government of India with a focus on the poor. Under the operations of TPDS, the beneficiaries were divided into two categories: Households Below the poverty line (BPL) Households Above the poverty line (APL) Central Government is responsible for Procurement of food grains Allocation of food grains Transportation of food grains to designated depots of Food Corporation of India (FCI). State Government is responsible for Allocation and Distribution of foodgrains within the state. Identification of eligible beneficiaries. Issuance of ration cards. Who Introduced the PDS System? PDS was introduced during the time of World War II. It was before the year 1960 that the distribution through PDS was dependant on imports of food grains. The Public Distribution System was then expanded in the 1960s to handle food shortages and take care of distribution. The Food Corporation of India and the Commission of Agricultural Costs and Prices were also set up by the government of India to improve domestic procurement and storage of food grains. It was during the 1970s when PDS evolved as a universal scheme for the distribution of food. What is the Use of PDS? It helps in maintaining the Food Security of the nation. It helps in making sure that food is available for the poor at affordable prices. Maintains buffer stock of food grains which will help during the lean season of crop production. Importance of PDS It helps in ensuring Food and Nutritional Security of the nation. It has helped in stabilising food prices and making food available to the poor at affordable prices. It maintains the buffer stock of food grains in the warehouse so that the flow of food remain active even during the period of less agricultural food production. It has helped in redistribution of grains by supplying food from surplus regions of the country to deficient regions. The system of minimum support price and procurement has contributed to theincrease in food grain production. FAQs How does the public distribution system (PDS) work? The Public Distribution System contributes significantly in the provision of food security. The Public Distribution System in the country enables the supply of food grains to the poor at a subsidized price. It also helps to control open – market prices for commodities that are distributed through the system. What are the objectives of the public distribution system (PDS)? The basic objective of the public distribution system in India is to provide essential consumer goods at cheap and subsidised prices to the consumers so as to insulate them from the impact of rising prices of these commodities and maintain the minimum nutritional status of our population.

public distribution system ration Read More »

The Non-Creamy Layer (NCL) certificate, also referred to as the Other Backwards Class (OBC) certificate, is granted to individuals who meet specific eligibility criteria. It was introduced by former Prime Minister V. P. Singh in 1993. Holders of the OBC certificate are eligible for reservation benefits and specific allocations in prestigious universities as well as public and private sector jobs. What is a Non Creamy Layer Certificate? In India’s affirmative action system, certain government jobs, educational institutions, and scholarship programs offer reservation benefits for Other Backward Classes (OBC) communities. But to be eligible for these advantages, an individual from an OBC background must obtain a Non-Creamy Layer Certificate (NCL). The ‘creamy layer’ refers to OBC individuals or families whose economic situation is considered relatively well-off. The NCL certificate essentially verifies that the applicant belongs to an OBC community and comes from a family with a total annual income below a specific threshold, typically set at ₹ 8 lakh (subject to change). Eligibility for Non-Creamy Layer Certificate Citizenship: You must be a citizen of India. Income Criteria: Your parents’ annual income should be below Rs.8 lakhs. This places you in the non-creamy layer of the Other Backwards Class (OBC) category. Parent’s Employment: Either of your parents should be employed as a Group C or Group D Central Government employee. Spousal Consideration: If your husband is a Central Government employee and your parents do not have a stable source of income, you may still be eligible to apply for an NCL certificate. Who is not eligible for the Non-Creamy Layer Certificate If you belong to the Other Backwards Class (OBC) category, you will not be eligible to apply for a Non-Creamy Layer (NCL) certificate if any of the following conditions apply to you: Caste Not Mentioned: If your caste is not included in the Central Government’s list of OBC, even if it falls under Backward Class (BC) or Most Backward Class (MBC). Parent’s Employment: If either of your parents is employed in Group A services of the Central Government, such as IAS (Indian Administrative Service), IPS (Indian Police Service), or IFS (Indian Foreign Service). Income Exceeds Rs.8 lakh: If your parent’s annual income exceeds Rs.8 lakh. Parent’s Employment Category: If your parents are employees of Group B in the Central Government or Group I in the State Government. Basic Requirements You must be a citizen of India. You must belong to an Other Backward Class (OBC NCL) community as recognized by the government. You must not fall under the creamy layer category, which is defined by income and other criteria. Income Criteria The current income ceiling for the creamy layer is ₹8 lakh per annum. This means if your parents’ combined gross annual income from all sources (including salary, agriculture, business, etc.) exceeds ₹8 lakh in the preceding three financial years, you are considered a creamy layer and not eligible for the Non-Creamy Layer Certificate. Some states might have slightly different income limits, so it’s important to check with your local authorities for the specific criteria in your area. Other Eligibility Criteria Employment: If your parents hold certain positions in the government or public sector, it might affect your eligibility. For example, in some states, children of Group A and Group B Central Government officers are considered creamy layer regardless of income. Land Ownership: In some cases, ownership of substantial landholdings could also affect your eligibility. Previous NCL Certificate: If you have already held a Non-Creamy Layer Certificate in the past, its validity period (usually one year) and the reason for needing a new one might be factored in determining your eligibility. Exceptions on Applying for Non-Creamy Layer Certificate While the basic eligibility for a Non-Creamy Layer Certificate revolves around income and caste, there are some exceptions and situations where individuals might not be eligible even if they meet the basic criteria: Caste Categories Non-Central OBC Castes: Castes categorized as Backward Classes (BC) or Most Backward Classes (MBC) in some states might not be included in the Central Government’s OBC list. This means individuals belonging to such castes wouldn’t be eligible for a Non Creamy Layer Certificate, even if they meet other criteria. Parental Occupation & Income Group A Central Government Officers: Children of parents holding positions in Group A services like IAS, IPS, and IFS, regardless of income, are considered creamy layer and cannot apply for the Non-Creamy Layer Certificate. Group B & C Central Government/Group 1 State Government: In some states, children of parents employed in Group B or C of the Central Government or Group 1 of the State Government might also be considered a creamy layer, irrespective of income. Private Sector Professionals with High Income: If your parents are professionals like doctors, lawyers, engineers, or business owners in the private sector and their combined income exceeds ₹8 lakh per annum, you wouldn’t be eligible for the NCL Certificate. Other Exceptions Landholdings: In some states, owning a substantial amount of land could lead to ineligibility, even if income is below the limit. Previous NCL Certificate: If your previous Non-Creamy Layer Certificate was obtained through fraudulent means, you might be ineligible for a new one. Documents required for obtaining a Non-Creamy Layer Certificate Identity Proof (any one document from the following): Aadhaar Card PAN Card Passport Driving License Voter ID Card Address Proof (any one document from the following): Aadhaar Card Ration Card Passport Telephone Bill Electricity Bill Voter ID Card Property Tax Receipt Caste Proof of the Parent or Relative (if parents are not present) Proof of Caste before and after Marriage (if applicable) Proof of Name Change for Married Women (if applicable) Certificate from Muslim Societies (for Muslim applicants) Documents of Home State (if applicable for migration) Applicant’s Photograph How to Apply for a Non-Creamy Layer Certificate Offline Step 1: Obtain the application form from your nearby Tehsildar or Revenue office. Step 2: Fill in the application form accurately with the required information. Step 3: If you have migrated, provide the relevant documents related to your home state. Step 4: If the father is not available, submit a blood relative’s caste certificate. Step 5: Sign the self-attestation section, attach a passport-size photograph, and submit the form along with the necessary documents. Step 6: After

Non-Creamy Layer Certificate Read More »