What Happens If Pan Card Is Not Linked To Aadhaar Card

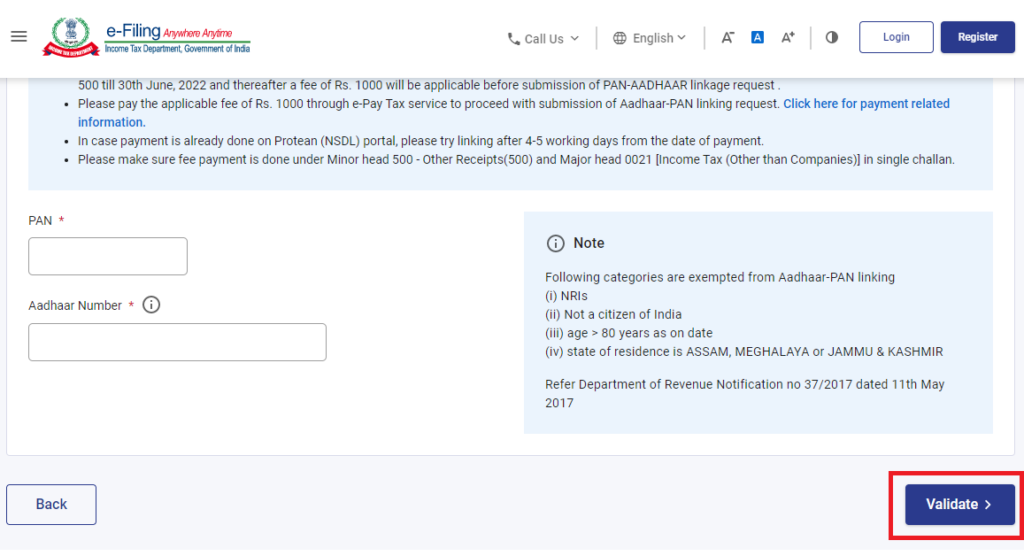

PAN unlinked with Aadhaar could get deactivated. This will result in higher taxation, penalties, and problems for the persons in financial transactions. The article presents advantages to the government and people through this linking exercise, sets out a step-by-step procedure for linking Aadhaar with PAN before the deadline of June 30, 2023, What is the Meaning of PAN Aadhaar Link? According to the mandate of the Indian government, every resident shall link Aadhaar with PAN, except NRIs, non-citizens, those above the age of 80 years, and residents of the exempted areas. This is basically a policy move aimed at helping avoid tax evasion by giving each taxpayer a unique identity. Non-linking of PAN and Aadhaar can impact financial transactions related to daily life and may impact access to governmental facilities. PAN is the unique tax identity number issued by the Income Tax Department to individual taxpayers and becomes necessary for filing income tax returns as well as a whole lot of other activities like opening bank accounts, making real estate investments, purchasing jewelry, applying for loans, or creating Demat accounts. The UIDAI brought forth the Aadhaar card that would give every Indian a unique identification number. It identifies persons through their biometric data and hence is more secure. Circular on PAN-Aadhaar Linking Section 139AA This section mandates that linking of PAN with Aadhar is mandatory for all taxpayers to provide the Aadhar card details when filing their income tax returns. The IT department issued a circular that it is mandatory for all PAN-holders (except those who fall under the exempt category) to link their PAN-Aadhaar within 30th June 2023. Initially, the IT department mandated to link PAN-Aadhaar by 31st March 2022 and then extended it to 30th June 2022. However, people who linked their PAN-Aadhaar between 1st July 2022 to 30th June 2022 had to pay a fine of Rs.500. Subsequently, the IT department extended the last date to link PAN-Aadhaar to 30th June 2023. PAN holders who link PAN-Aadhaar between 1st July 2022 to 30th June 2023 must pay a penalty of Rs.1,000. PAN card will become inoperative from 01st July 2023 if PAN holders do not link it with their Aadhaar card. The IT department has mandated linking PAN-Aadhaar to regulate and curb tax evasion. Importance of linking PAN with Aadhaar card The PAN card of a person will become inoperative when it is not linked to an Aadhaar card. PAN-Aadhaar linking is required when filing the Income Tax Return (ITR). The IT department may reject the ITR when PAN and Aadhaar are not linked. PAN and Aadhaar cards are required to be submitted to get government services, such as applying for a passport, obtaining subsidies and opening a bank account. Thus, it is difficult to access government services when PAN and Aadhaar cards are not linked. When the PAN-Aadhaar is not linked, getting a new PAN card may be difficult if the old one is damaged or lost since it is mandatory to mention the Aadhaar card number while applying for a new PAN card. Consequence of Not Linking PAN with Aadhaar PAN Card stops functioning A person’s PAN will stop working if they fail to connect it to Aadhaar by the deadline. It won’t be feasible to provide, disclose, or quote the PAN number anyplace once it stops working. This might also lead to: Applying a higher tax rate on income taxes Increased TDS gathering Inability to complete income tax forms, which may result in additional interest charges, fines, and legal ramifications if information about earned income is withheld. Penalties for failing to quote PAN in certain banking transactions Interchangeability of PAN and AADHAAR is prohibited The Income-tax Act says that Aadhaar and PAN can be used instead of each other if they are linked. This means that you can use either PAN or Aadhaar, based on the situation. But these numbers can’t be used in place of each other if they’re not linked. Furthermore, no one would be able to cite Aadhaar instead of PAN or vice versa since PAN will become inoperative in the event of non-linking to Aadhaar. PAN Aadhaar Link: Section 234H Penalties In the event that an individual doesn’t connect their PAN and Aadhaar by the deadline, they might be given a punishment of ₹1,000 for failing to connect their PAN and Aadhaar. Non-filing of pay returns would bring about a punishment of ₹ 10,000. Formerly, there was a Rs. 500 fee to connect PAN to Aadhaar. As of right now, taxpayers must connect their PAN to Aadhaar by June 30, 2023, or face a ₹ 1,000 late fee. As a result, before registering for the PAN-Aadhaar link on the Income Tax website, they must pay the penalty. To pay the fine, they must, however, make sure they have a working PAN, Aadhaar, and cellphone number. How to activate inoperative PAN card and link with Aadhaar card? Step 1: Visit the Income Tax e-Filing Portal. Step 2: Click the ‘e-Pay Tax’ option under the ‘Quick Links’ heading. Step 3: Enter the ‘PAN’ number under ‘PAN/TAN’ and ‘Confirm PAN/TAN’ column, enter mobile number and click the ‘Continue’ button. Step 4: After OTP verification, it will be redirected to e-Pay Tax page. Click the ‘Continue’ button. Step 5: Click the ‘Proceed’ button under the ‘Income Tax’ tab. Step 6: Select Assessment Year as ‘2024-25’ and ‘Type of Payment (Minor Head)’ as ‘Other Receipts (500)’ and select ‘Fee for delay in linking PAN with Aadhar’ and click the ‘Continue’ button. Step 7: The applicable amount will be pre-filled against ‘Others’ option. Click ‘Continue’ button and make the payment. FAQs If I miss the deadline, can I still connect my PAN to my Aadhaar? It is still possible to connect your PAN and Aadhaar even if the June 30, 2023 deadline passes. However, if you miss the deadline, your PAN card will stop working. It must be connected to the Aadhaar number before it can be turned on. If PAN-Aadhaar is linked after the deadline, there is a ₹1,000 fine. How long is the validity

What Happens If Pan Card Is Not Linked To Aadhaar Card Read More »