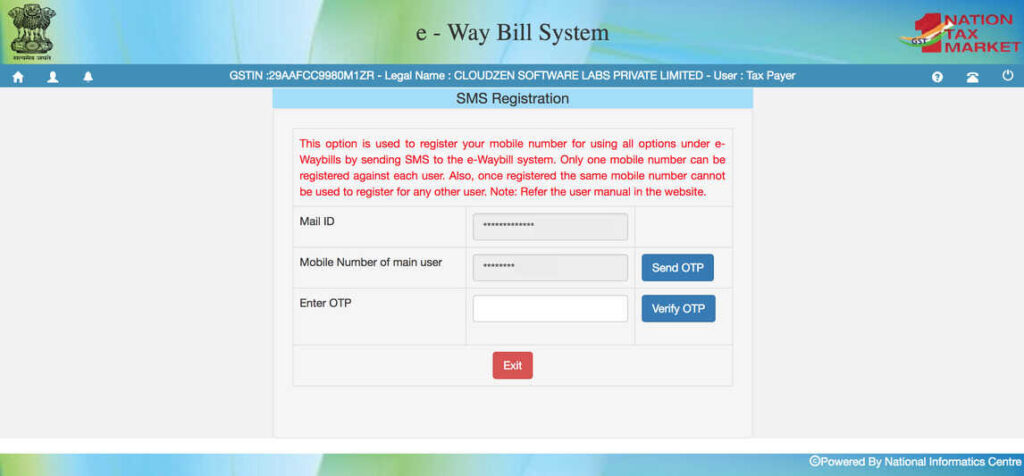

eWay Bill Generation on Mobile through SMS

the EWB is the short form for Electronic Way Bill or E-way Bill. The government of India’s EWay Bill login portal, available at https://ewaybillgst.gov.in, is a website created to facilitate the flow of commodities throughout the nation. For companies that are subject to the Goods and Services Tax (GST) system, particularly those that ship items […]

eWay Bill Generation on Mobile through SMS Read More »