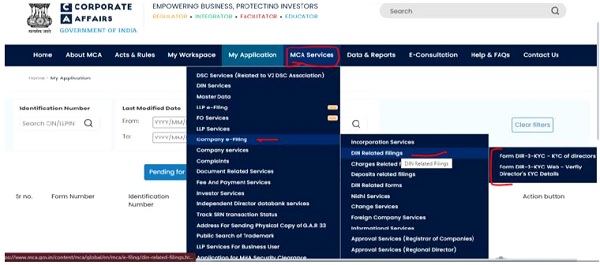

Application for surrender of DIN in e-form DIR-5 can be filed for any reason such as DIN is unused and not intended for future reference also or multiple DINs are allotted to the same person or DIN the holder is no more/has become of unsound mind or insolvent etc. eForm DIR-5 is required to be filed pursuant to Section 153 of the Companies Act, 2013 & Rule 11 (f) of Companies (Appointment and Qualification of Directors) Rules, 2014. According to Section 153 of the Companies Act, 2013 every individual who is intending to be appointed as director of a company shall make an application for allotment of DirectorIdentification Number to the Central Government in such form along with fees. According to Rule 11 (f) of Companies (Appointment and Qualification of Directors) Rules, 2014 application made in Form DIR-5 by the DIN holder to surrender his or her DIN along with the declaration that he has never been appointed as a director in any company and the said DIN has never been used for filing any document with any authority, the Central Government may deactivate such DIN. Latest Update in Form DIR-3 KYC Under MCA Important Update by MCA – “DIN holders of DINs marked as ‘Deactivated’ due to non-filing of DIR-3KYC/DIR-3 KYC-Web and those Companies whose compliance status has been marked as “ACTIVE non-compliant” due to non-filing of Active Company Tagging Identities and Verification (ACTIVE) e-form are encouraged to become compliant once again in pursuance of the General Circular No. 11 dated 24th March 2020 & General Circular No.12 dated 30th March 2020 and file DIR-3KYC/DIR-3KYC-Web/ACTIVE as the case may be between 1st April 2020 to 30th September 2020 without any filing fee of INR 5000/INR 10000 respectively.” Who Needs to File e-Form DIR 3 KYC? As per MCA recent announcement, any director who was allotted a DIN by or on 31st March 2018 and whose DIN is in approved status, will have to submit his/her KYC details to the MCA. Further, this procedure is mandatory for the disqualified directors too. From the Financial Year 2019-20 onwards, it is mandatory for every director who has been allotted a DIN on or before the end of the financial year and whose DIN is in approved status, will have to file form DIR-3 KYC before 30th September of the immediately next financial year. For example– For the Financial Year 2022-23, the directors having DIN or Director Partner Identification Number (DPIN) and the directors allotted with a DIN/DPIN by 31st March 2023, need to file the e-Form DIR-3 KYC before 30th September 2023. There are two types of e-Form DIR-3 KYC, which are as follows: DIR-3 KYC – Any director who is filing e-Form DIR-3 KYC for the first time after allotment of DIN or whose details are required to be updated/changed must file this form. DIR-3 KYC (Web) – Any director who has already filed the e-Form DIR-3 KYC/DIR-3 KYC (Web) in the previous year can file this form when there is no change in his/her KYC details. In this e-Form, the basic details of the director will be pre-filled from the MCA data and, thus, cannot be changed. What is the due date for Filing DIR-3 KYC? The last date for filing of Director KYC for the Financial Year 2023-24 (ending on 31st March 2024) is 30th September 2024. However, the Director KYC can be filed on or after 1st April 2024 and until 30th September 2024. If the Annual Filing of the DIN KYC is not completed within the due date, then the status of the DIN is changed to Deactivated. A deactivated DIN primarily restricts the director’s ability to act as a director.Every DIN holder whose DIN has been deactivated due to non-filing of DIR-3 KYC must file an eform known as DIR-3 KYC or perform KYC through the web service along with the applicable fee. Once the form (DIR-3 KYC) is filed, it is approved on an STP basis, and the system will automatically reactivate the DIN. Non-compliant DINs’ status would remain ‘Deactivated due to Non-filing of DIR-3 KYC.’ However, please note that filing of DIN KYC after its due date attracts an additional government fee of Rs. 5000/-. Documents required for filing e-Form DIR-3 KYC Permanent address proof, such as Voter’s ID, driving license or PAN card. Present address proof, such as utility bills not older than 2 months, rental agreement, etc. Aadhaar card. Passport. Other optional documents. Apart from the above documents mentioned above, please keep the following things ready: Digital Signature Certificate (DSC) of the director filing the form (applicant). DSC, membership number, certificate of practise number from a practising professional, such as CA, CS, or Cost Accountant. Step-by-step guide to file e-Form DIR-3 KYC Step 1: Login to MCA website Login to the MCA website by clicking ‘Sign In/Sign Up’ button on the homepage. If you have not registered on the MCA website, you can register by clicking the ‘Register’ button, entering the required details and logging in by entering the User ID and password. Step 2: Enter the mobile number and email After logging into the MCA website, go to ‘MCA Services’ tab, then ‘Company e-Filing’, ‘DIN Related Filings’ and click ‘Form DIR-3 KYC’ or ‘Form DIR-3 KYC Web’. On the form, the director must enter the DIN number, mobile number and email. OTP will be sent to mobile number and email. Enter the OTP and click on ‘Next’. Step 3: Enter the details in the DIR-3 KYC Form The director has to enter the below details on the next page: Name Father’s name Nationality Date of birth Gender PAN number Mobile number OTP sent to mobile number Email ID OTP sent to email ID Aadhaar number Permanent residential address Present residential address If the director is filling e-Form DIR-3 KYC (Web), the above details will be pre-filled. The details which are not pre-filled will have to be filled by the director. Note: It is mandatory to declare Permanent Account Number (PAN). After entering PAN details, director will have to click on the ‘Verify income-tax PAN’ button. The system will verify the