Letter of Credit (LC)

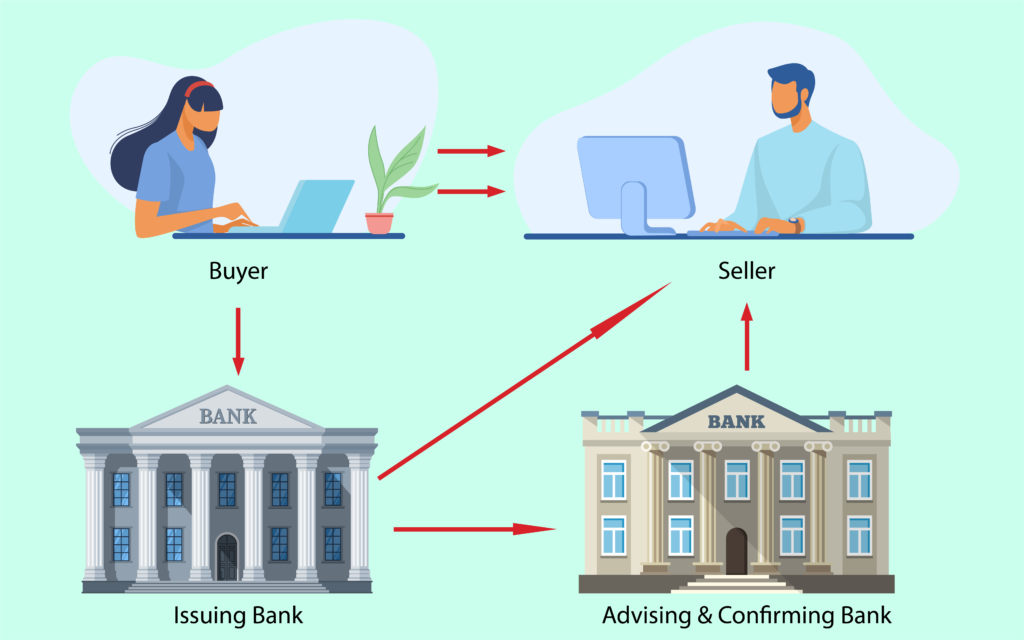

A letter of credit, or a credit letter, is a letter from a bank guaranteeing that a buyer’s payment to a seller will be received on time and for the correct amount. If the buyer is unable to make a payment on the purchase, the bank will be required to cover the full or remaining amount of the purchase. It may be offered as a facility (financial assistance that is essentially a loan). Due to the nature of international dealings, including factors such as distance, differing laws in each country, and difficulty in knowing each party personally, the use of letters of credit has become a very important aspect of international trade to protect buyers and sellers. A Letter of Credit (LC) is a document that guarantees the buyer’s payment to the sellers. It is issued by a bank and ensures timely and full payment to the seller. If the buyer is unable to make such a payment, the bank covers the full or the remaining amount on behalf of the buyer. Letter of Credit Letter of Credit (LC) is a credit limit that is used majorly by businesses engaged in international trade. It acts as a payment guarantee offered by Bank/NBFCs to exporters. Letter of Credit is a payment instrument in which Banks/NBFCs offer monetary guarantee to enterprises that are engaged in the import and export businesses, in case of payment delays or any default. Enterprises operating businesses overseas often deal with unknown suppliers so they require assurance of payment before performing any business transaction. Therefore, Letter of Credit acts as a financial instrument that offers payment assurance to the suppliers or exporters dealing in sales and purchase of goods and services. How Letter of Credit Works Letter of Credit is issued by the Bank to the Buyer in order to secure the timely payment by the buyer to the seller. It acts as a guarantee on behalf of the buyer that he/she pays the full amount to the seller, as per the defined timeline or on time. If in case the buyer is unable to repay the amount to the seller on time, then the bank will pay on the buyer’s behalf to the seller. Features LC is issued against Collateral/Security that may include buyer’s Fixed Deposits and Bank Deposit, etc. Certain fees is charged by the Bank depending on the type of Letter of Credit Guidelines are issued by the International Chambers of Commerce (ICC) for any form of Letter of Credit Correctness of Letter of Credit: Only documents are exchanged and no goods and services are involved in this process. Therefore, mentioned details in the letter should be correct that including the name of the seller, date, amount, product name and quantity, etc. Banks will deny the payment, if they find any slightest mistake in the buyer’s name, product name, shipping date, etc. As all parties deal in documents only and not goods and services, so the payment will not depend on the defects in goods and services, if any Types of Letter of Credit in India 1. Credit on Sight In this type of credit, an entrepreneur can present a bill of exchange to the lender with a sight letter and can take the funds instantly on the basis of a letter of sight. A sight letter of credit is considered to be the most instant letter of credit that can be availed immediately. 2. Time Credit Bill of exchange that is paid after an agreed time period between the lender and the borrower is known to be time credit. A certain time period is involved in this type of credit. Letter of Credit defining time credit allows a borrower with some days to repay the amount, only after receiving the goods. 3. Standby Letter of Credit (SBLC) Standby Letter of Credit (SBLC) is a credit mechanism in which an importer can get foreign currency funds internationally by providing the issuance of SBLC from the domestic bank that guarantees payment to the international bank if the borrower fails to repay the amount before the due date. 4. Revocable Credit Revocable credit is a type of letter of credit in which the terms and conditions of this type of LC can be amended or canceled by the issuing bank. It is not important for the issuing bank to tell beneficiaries about any change in the letter of credit. 5. Irrevocable Credit Irrevocable Credit is a type of LC in which the terms and conditions cannot be amended or canceled by the issuing bank. The bank has to obey the directions or commitments mentioned in the letter of credit. 6. Transferable Credit Transferable credit, as the name suggests is a type of LC in which the beneficiary can transfer his/her rights to third parties. The terms and conditions may differ as per the trade and industry. Process of Letter of Credit Step 1: The applicant or the buyer approaches the desired bank for the issuance of a letter of credit. This bank is known as an opening or issuing bank. Step 2: There will be an advising bank (mostly an international bank) for the beneficiary or seller that will receive the Letter of Credit issued by the issuing bank of the buyer. Further, the advising bank will check the authenticity of the letter of credit by checking the name, product details, etc. Step 3: Advising bank will share the letter of credit with the seller by keeping him/her rest assured that the money shall be received, as banks are now involved in this process. Step 4: Post seller assurance, the goods will be shipped as per the details mentioned by the buyer or applicant. The seller will now receive the bill of lading as the seller has already exported the goods. Step 5: The buyer shall now present the Bill of Lading to the Nominated or the Negotiating bank (International bank) where the bank will check all the shipping documents, and whether all goods were shipped as per the instructions. Finally, the nominating bank will do the payment to the seller or exporter. Step 6: Further

Letter of Credit (LC) Read More »