West Bengal Professional Tax

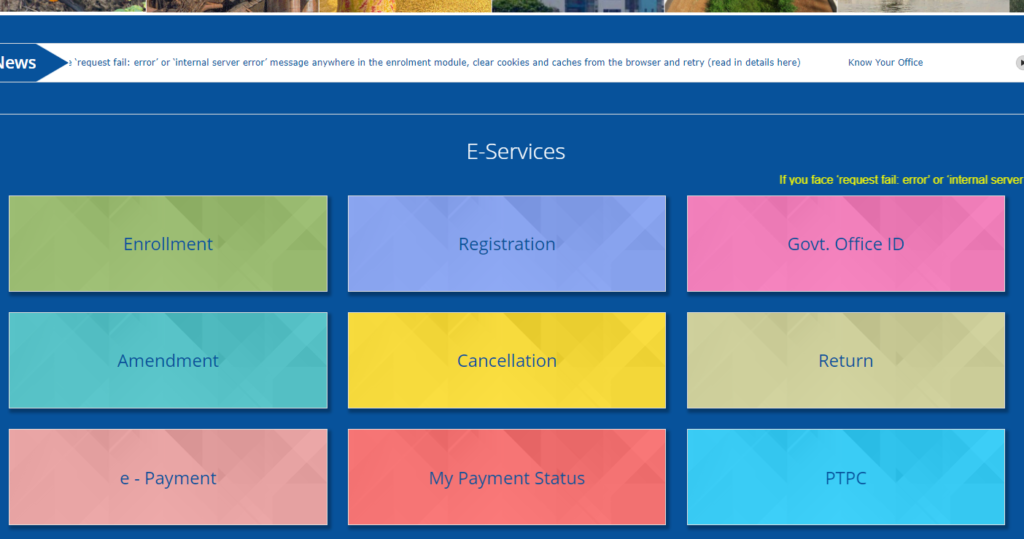

Article 276, Clause 2 of the Indian Constitution, the State Government of West Bengal can charge professional tax on income earned various sources. Professional tax in West Bengal is managed by West Bengal Tax on Profession, Trade, Callings and Employment Act, 1979. Professional Tax In West Bengal As per the West Bengal State Tax on Profession, Trades, Callings and Employment Act, 1979, salaried individuals or professionals with a gross monthly salary of more than Rs 10,000 are liable to pay professional tax. This signifies that you must pay this tax if your gross monthly salary is Rs 10,001. West Bengal Professional Tax Slab Rate in 2024 Each state government revises its professional slab tax rates at regular intervals, usually on yearly basis. Mentioned below is the revised rates of West Bengal Professional Tax: Monthly Gross Salary Amount Payable Up to Rs. 10,000 Nil Rs. 10,001-Rs. 15,000 Rs.110 Rs. 15,001 – Rs. 25,000 Rs. 130 Rs. 25,001 – Rs. 40,000 Rs. 150 Above Rs. 40,001 Rs. 200 West Bengal Professional Tax Rule As per Clause 2 of Article 276 of the Indian Constitution, professional tax in West Bengal is levied as per the provisions under the West Bengal Tax on Profession, Trade, Callings and Employment Act, 1979. Professional Tax is broadly classified into two types: Professional Tax Registration (PTRC): If you are a salaried employee, your establishment will have to obtain PTRC, this tax is automatically deducted by your employer and deposited to the state government. Professional Tax Enrollment (PTEC): If you are self-employed, you must pay it on your own by visiting any of the WB professional tax offices. The maximum amount you must pay as professional tax in West Bengal is Rs 2,500 per month. Eligibility The West Bengal State Legislature passed the “West Bengal State Tax on Professions, Trades, Callings and Employments Act, 1979” for its citizens. The persons liable to pay Profession Tax under the Act are divided into two categories. In the case of salaried persons and wage earners, the employer (Public and Private Sectors, Government who distribute salary or wages to the employees) deducts the Profession Tax from the salary or wages and is liable to deposit the same with the State Government. For other categories of individuals, the person who has engaged in employment, profession, calling, and trade is responsible for paying the tax. Professional Tax Applicability In West Bengal Self-employed individuals earning a specific amount are required to pay such tax. Professionals involved in government and private organisations are eligible to pay this tax. Other categories of taxpayers include- licensed boat suppliers, occupiers for factories, tax consultants, management consultants, architects, etc. West Bengal Professional Tax Online Payment Navigate to the website of the Profession Tax Directorate of Commercial Taxes, Government of West Bengal. Click on ‘e-payment’ under ‘E-services’. This will lead you to ‘GRIPS’ through which you can complete your transaction. To complete the payment, you can opt for four options. Check them out below: With Enrolment Number Select the ‘Enrolment Number’ option and provide the 12-digit PT Enrolment number. Click on ‘submit’ to get payment details. Select the mode of payment, year and payment. Follow the instructions and click on the ‘Pay’ option. With Registration Number Select ‘Registration Number’ and provide your 12-digit registration number. Select the submit option to get payment details. After following the instructions on the screen, click on the ‘Pay’ option. With Application Number for New Profession Tax Enrolment On the website, enter the 11-digit application number. Select on ‘submit’ option, and you will get payment details. Select ‘payment mode’. After entering the required details, click on the ‘Pay’ option. With Government ID On the website, select the ‘Government ID’ option and enter 12 12-digit government ID number. Click on ‘Submit’, and you will get details of payment. Finally, select ‘payment mode’, ‘month of payment’, and ‘year of payment’ and click the ‘Pay’ option to complete payment. FAQs How much is the professional tax in West Bengal? The tax rate may vary based on your income. Individuals earning up to Rs 10,000 per month don’t have to pay any professional tax. Moreover, the maximum amount that anyone has to pay is Rs 2500. Who is exempt from professional tax in West Bengal? Members of the Indian Navy, Air Force and Army serving in any part of West Bengal do not have to pay any professional tax to the state government.

West Bengal Professional Tax Read More »