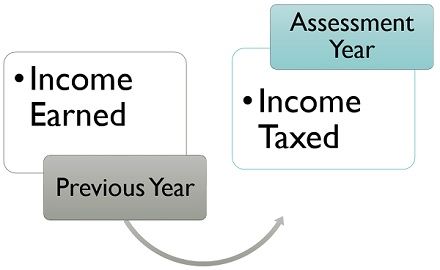

Difference between financial year and assessment year

Assessment Year (AY) and Financial Year (FY) are two important terms in income tax and financial planning. They are used to determine the taxation of an individual or entity’s income. While both terms are fundamental to understanding tax obligations and planning, their definitions, functions, and implications are markedly different. In this guide, we will delve into the nuances of AY and FY, shedding light on their significance in taxation, financial reporting, and planning. What is Financial Year? The financial year is the year in which you have earned the income. It starts on the 1st of April of the calendar year & ends on the 31st of March of the next calendar year. The term “Financial Year” is also commonly referred to as F.Y. For example, the financial year 2024-25 started on April 1st, 2024, and will end on March 31, 2025. What is Assessment Year? Assessment year means the year (from 1st April to 31st March) in which income you earn in a particular financial year is taxed. You are required to file your income tax return in the relevant assessment year. The assessment year is the year just succeeding the Financial Year. E.g., Income earned in the current Financial Year 2023-24 (i.e., from 1st April 2023 to 31st March 2024) will become taxable in Assessment Year 2024-25 (i.e., from 1st April 2024 to 31st March 2025 ). AY and FY for Recent Years Period Financial Year Assessment Year 1 April 2024 to 31 March 2025 2024-25 2025-26 1 April 2023 to 31 March 2024 2023-24 2024-25 1 April 2022 to 31 March 2023 2022-23 2023-24 1 April 2021 to 31 March 2022 2021-22 2022-23 1 April 2020 to 31 March 2021 2020-21 2021-22 1 April 2019 to 31 March 2020 2019-20 2020-21 1 April 2018 to 31 March 2019 2018-19 2019-20 What is the difference between Assessment Year and Financial Year? From the tax perspective, a Financial year is a year in which a person earns an income. On the other hand, The assessment year is the year followed by the financial year in which the previous year’s income is evaluated, tax is paid on the same, and an Income tax Return (ITR) is filed. For instance, if we consider the financial year from 1 April 2022 to 31 March 2023, it is known to be the Financial year 2022-23. The assessment year begins after the financial year ends, so the assessment year of FY 2022-23 would be AY 2023-24. Why Does an ITR Form have AY? Since income for any particular financial year is evaluated and taxed in the assessment year, income tax return forms have an assessment year (AY). As the income earned in a financial year cannot be taxed before it is earned, so it is taxed in the following year. Scenarios like loss of job, job change, new investments etc., can come up in the middle or end of the FY. Also, the income earned in a financial year cannot be exactly known before the end of the financial year. This is why the assessment can start only after the financial year ends. Hence, taxpayers have to select AY while filing their income tax returns. FAQs Are the Financial Year and Previous Year the same? Yes, for ITR filing, the financial year and previous year mean the same. E.g., the Financial Year 2022-23 also means the Previous Year 2022-23. How do I calculate my income and tax liability for the purpose of filing an income tax return? You should calculate your income for the full financial year and calculate the tax thereon. You need to file an income tax return when your income exceeds the basic exemption limit of Rs. 2.5 lakhs for individuals under the age of 60 years, Rs.3 lakh for individuals of the age 60-80 years, Rs. 5 lakh for individuals who are above the age of 80 years. However Rs. 3 lakhs under the new tax regime for all the individuals.

Difference between financial year and assessment year Read More »