Section 74 – Code of Criminal Procedure, 1973

Warrant directed to police officer A warrant directed to any police officer may also be executed by any other police officer whose name is endorsed upon the warrant by the officer to whom it is directed or endorsed.

Transfer Pricing

Transfer pricing can be defined as the value which is attached to the goods or services transferred between related parties. In other words, transfer pricing is the price that is paid for goods or services transferred from one unit of an organization to its other units situated in different countries (with exceptions). Transfer price, also […]

Scheme for Promoting Interests, Creativity and Ethics among Students (SPICES)

The scheme “AICTE – Scheme for Promoting Interests, Creativity and Ethics among Students (SPICES)” is a scheme for the institutions by the All India Council for Technical Education (AICTE), Department of Higher Education (DoHE). This scheme provides financial support to institutions for developing students’ clubs for the well-rounded development of students by promoting their interests, […]

SBI SME eBiz Loan

State Bank of India (SBI) offers a vast array of loans to cater to the financial needs of the Small and Micro Enterprises (SME) sector. Individuals who are engaged in income-generating activities in the manufacturing, trading, and services sectors can avail loans ranging between Rs.5 lakh and Rs.500 crore. The interest rates charged on these loans range […]

Integrated Child Development Services Rajasthan

Integrated Child Development Services (ICDS) is an Indian government welfare programme that provides food, preschool education, and primary healthcare to children under 6 years of age and their mothers. ICDS Scheme The scheme was started in 1975 and aims at the holistic development of children and empowerment of mother. It is a Centrally-Sponsored scheme. The […]

Employment Contracts in India

The Indian Contract Act, of 1872 primarily governed the employment contract in India. An employment agreement is a mutual contract between the Employee and the employer that rules the terms of employment. Like any other agreement under the standard law system, the vital requirements of the employment contract letter include an offer, consideration, acceptance, lawful […]

Interim Dividend

The Indian Contract Act, of 1872 primarily governed the employment contract in India. An employment agreement is a mutual contract between the Employee and the employer that rules the terms of employment. Like any other agreement under the standard law system, the vital requirements of the employment contract letter include an offer, consideration, acceptance, lawful […]

Mahila Samman Saving Certificate

In a significant move from the government, Smt. Nirmala Sitharaman announced the introduction of the Mahila Samman Savings Certificate in the Budget 2023-24. This scheme has been launched to encourage savings and investment by the women of India. The scheme “Mahila Samman Savings Certificate” was launched by the Department of Economic Affairs, Ministry of Finance […]

Preference Shares in Private Limited Company

Preference shares or preferred stocks are company stocks which extend dividends to its shareholders. Though such shares extend a fixed dividend, they do not come with any voting rights. Notably, a company often issues different types of preference shares which are distinct in their features and associated benefits. What are Preference Shares? Preference shares or preferred stocks come […]

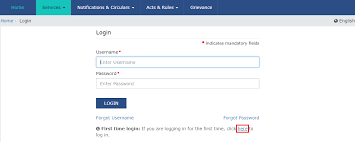

Gst Login Portal

The official GST website of the government is www.gst.gov.in, also known as the GST Portal. It helps taxpayers with a variety of programs, including getting GST registration, filing GST returns, applying for refunds, and cancelling their GST registration. The fact that the tax administration must rely heavily on technologies is an essential part of the […]