Make in India initiative celebrates 10 Years of its launch

Name of the scheme Make in India Date of launching 25th September 2014 Launched by PM Narendra Modi Government Ministry Ministry of Commerce and Industry Make in India website http://www.makeinindia.com/home/ 10 years of ‘Make in India’ Launched in 2014 to transform India into a global manufacturing hub.About Make in IndiaObjective: To facilitate investment, foster innovation, […]

Dormant Account

A dormant account is a customer’s account at a bank or other financial institution that has seen no activity, with the possible exception of interest deposits, for a long period of time. The owner may have forgotten about the account, moved out of town without leaving a forwarding address, or died. A dormant account with […]

Directorate of Women Empowerment

Women Empowerment is the progression of women and, accepting and including them in the decision-making process. It also means providing them with equal opportunities for growth and development in society, and disapproving gender bias. Article 15(3) mentions the welfare of women and children and can be stated as “Nothing in this article shall prevent the […]

TCS Rate Chart as applicable for the Financial Year 2023-2024 (Assessment Year 2024-2025)

Indian Income Tax Act has provisions for tax collection at source or TCS. In these provisions, certain persons are required to collect a specified percentage of tax from their buyers on exceptional transactions. Most of these transactions are trading or business in nature. It does not affect the common man. What is Tax Collected at Source (TCS)? […]

GSTR 9 and 9C

Digital is one word that would be synonymous with the current year in India. From GSTN to the e-Way Bill, the finance sector, by far more than any other Industry, went through the most aggressive digital; makeover in recent years. For better or worse, we must now accept the fact that 2022 was the year […]

ITR-1: Key Differences between the Old and New Tax Regime

The Budget 2023 caused a lot of confusion among taxpayers regarding the choice between the old and new tax regimes. The government introduced various incentives in the 2023 Budget and 2024 Budget to encourage the adoption of the new regime. These changes show that the government intends to have taxpayers transition to the new regime and eventually phase out […]

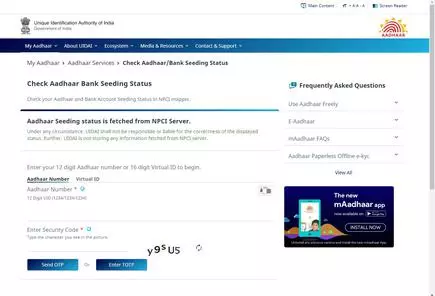

Aadhaar Bank Link Status Check

You can link your Aadhar card to a bank account offline using SMS, mobile banking, ATMs, and other methods. In the event that you do not connect your Aadhar card to your bank account, you will forfeit the funds and advantages of the scheme. By utilising your cell phone number, the mAadhaar app, or the […]

LLP Form 11 Annual Return

Form 11 comprises an annual return i.e to be furnished by all LLPs no matter what the turnover is in that year. Also, Limited Liability Partnership (LLP) does not have any operations or business in the fiscal year, Form 11 is required to be furnished. Apart from the basic details about the Name, and Address of LLP, […]

EPF Interest Rate

EPF is a retirement benefits scheme under the Employees Provident Fund and Miscellaneous Act, 1952, where an employee has to pay a certain contribution towards the scheme and an equal contribution is paid by the employer as well on a month on month basis. The Scheme is managed by Employee Provident Fund Organization (EPFO). The […]

What is CST Registration

The Central Sales Tax Act, 1956 defines the guidelines which determine if a trade can be categorised as a sale or purchase of goods by way of inter-state commerce in order to outline the conditions and restrictions regarding the tax that is imposed. Introduction: The structure and sections of the Indian tax system is fairly […]