Section 105-I – Code of Criminal Procedure, 1973

Fine in lieu of forfeiture (1) Where the Court makes a declaration that any property stands forfeited to the Central Government under section 105H and it is a case where the source of only a part of such property has not been proved to the satisfaction of the Court, it shall make an order giving […]

Haryana Road Tax

Haryana is one of the leading Indian states in terms of rapid infrastructure development. The North Indian state has a vast network of at least30 National Highways,11 Expressways and several State Highways, keeping it well connected to its neighbouring states. The people of Haryana immensely benefit from the wide connectivity of roads to commute within […]

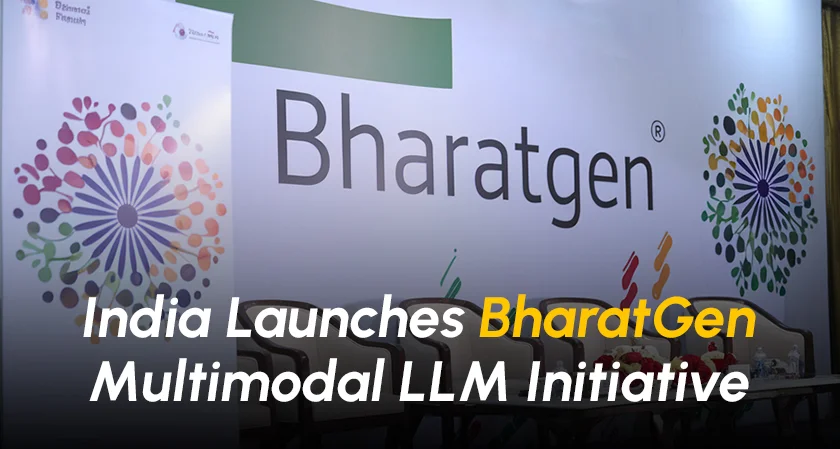

India launches BharatGen

BharatGen, a pioneering initiative in generative AI, was launched in India on September 30, 2024, in Delhi. The initiative is designed to revolutionize public service delivery and boost citizen engagement by developing a suite of foundational models in language, speech, and computer vision. The event convened in the virtual presence of Dr Jitendra Singh, Union […]

Covid 19 Ex Gratia Details

The mismanagement of the COVID-19 pandemic has been independent India’s gravest governance failure. The Union government under Prime Minister Narendra Modi did not take adequate measures to prevent and contain the pandemic. Therefore, there is a Need for a White Paper (Chapter-1) that examines the government’s acts of omission and commission, its impact on India […]

SEBI KYC Registration Agency

Operating a mutual fund house is subject to stringent regulations. Activities must be conducted within the structure already in place and governed by the Securities and Exchange Board of India (SEBI). This involves adhering to the SEBI KYC guidelines. Identifying a customer before enrolling them as an investor under a particular fund is known as “Know Your […]

Excise Duty in India

Taxation plays a vital role in the economy and makes a significant contribution to it. In India, the tax structure encompasses different types of taxes and duties like excise duty. To streamline the process of paying taxes and claiming returns, it is essential for individuals whose income comes under a taxable bracket to become familiar with […]

GST Composition Scheme

Composition Scheme acts as an alternative method for levying a tax under GST. Small businesses registered under the GST composition scheme can pay GST at a fixed rate of turnover every quarter and file quarterly GST returns. Composition levy would be generally related to small taxpayers who are supplying goods and services or both to […]

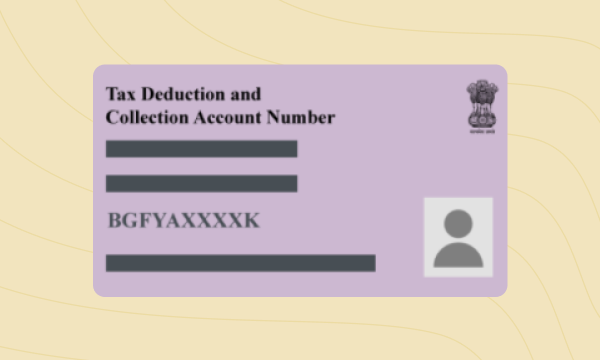

TAN Number: A Comprehensive Guide for Taxpayers

The full form of TAN is Tax Deduction or Collection Account Number. Every person liable to deduct TDS or TCS must apply for TAN. As per section 203A, this 10-digit alphanumeric number must be quoted when you become liable to either Deduct or Collect tax (i.e., liable to deduct TDS or collect TCS), make payment […]

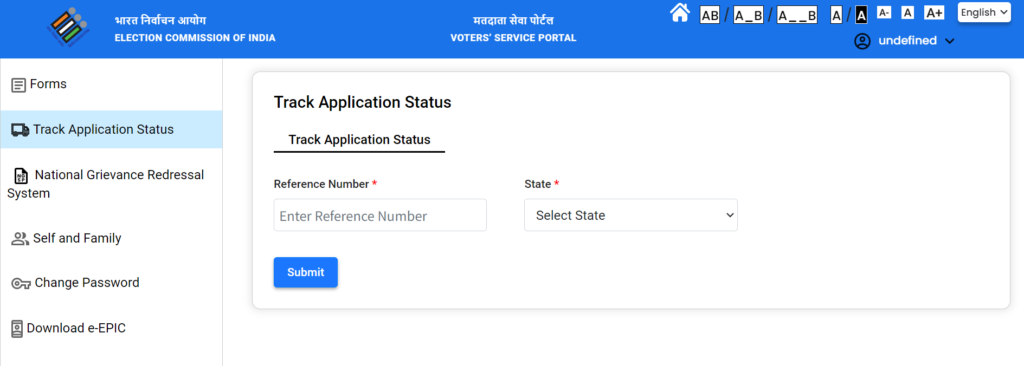

Voter ID Status

The Voter ID, or Voter Card or Electors Photo Identity Card (EPIC) is a very important document to have in the largest democracy of the world. One of the fundamental rights guaranteed by democracy is the right to vote. This right can be exercised through the Voter ID. The inception of Voter ID goes right […]

Lost Aadhar Card

Aadhaar Card acts as proof of identity and proof of address. It is also important to avail various government-aided subsidies, opening a bank account, investing in fixed deposit, mutual funds, etc. However, it is imperative that you must not lose your Aadhaar card, but in case of loss or misplacement of Aadhaar card, you can get […]