This Accounting Standard is not mandatory for Small and Medium Sized Companies, and Micro, Small and Medium sized enterprises (Level IV, Level III and Level II non-company entities), as defined in Appendix 1 to this Compendium ‘Applicability of Accounting Standards to Various Entities’. Such Companies are however encouraged to comply with the Standard.

Objective

The objective of this Standard is to establish principles for reporting financial information, about the different types of products and services an enterprise produces and the different geographical areas in which it operates. Such information helps users of financial statements:

- (a) better understand the performance of the enterprise;

- (b) better assess the risks and returns of the enterprise; and

- (c) make more informed judgements about the enterprise as a whole.

Many enterprises provide groups of products and services or operate in geographical areas that are subject to differing rates of profitability, opportunities for growth, future prospects, and risks. Information about different types of products and services of an enterprise and its operations in different geographical areas – often called segment information – is relevant to assessing the risks and returns of a diversified or multi-locational enterprise but may not be determinable from the aggregated data. Therefore, reporting of segment information is widely regarded as necessary for meeting the needs of users of financial statements.

Scope

1 This Standard should be applied in presenting general purpose financial statements.

2 The requirements of this Standard are also applicable in case of consolidated financial statements.

3 An enterprise should comply with the requirements of this Standard fully and not selectively.

4 If a single financial report contains both consolidated financial statements and the separate financial statements of the parent, segment information need be presented only on the basis of the consolidated financial statements. In the context of reporting of segment information in consolidated financial statements, the references in this Standard to any financial statement items should construed to be the relevant item as appearing in the consolidated financial statements.

Definitions

5 The following terms are used in this Standard with the meanings specified:

5.1 A business segment is a distinguishable component of an enterprise that is engaged in providing an individual product or service or a group of related products or services and that is subject to risks and returns that are different from those of other business segments. Factors that should be considered in determining whether products or services are related include:

- (a) the nature of the products or services;

- (b) the nature of the production processes;

- (c) the type or class of customers for the products or services;

- (d) the methods used to distribute the products or provide the services; and

- (e) if applicable, the nature of the regulatory environment, for example, banking, insurance, or public utilities.

5.2 A geographical segment is a distinguishable component of an enterprise that is engaged in providing products or services within a particular economic environment and that is subject to risks and returns that are different from those of components operating in other economic environments. Factors that should be considered in identifying geographical segments include:

- (a) similarity of economic and political conditions;

- (b) relationships between operations in different geographical areas;

- (c) proximity of operations;

- (d) special risks associated with operations in a particular area;

- (e) exchange control regulations; and

- (f) the underlying currency risks.

5.3 A reportable segment is a business segment or a geographical segment identified on the basis of foregoing definitions for which segment information is required to be disclosed by this Standard.

5.4 Enterprise revenue is revenue from sales to external customers as reported in the statement of profit and loss.

5.5 Segment revenue is the aggregate of

- (i) the portion of enterprise revenue that is directly attributable to a segment,

- (ii) the relevant portion of enterprise revenue that can be allocated on a reasonable basis to a segment, and

- (iii) revenue from transactions with other segments of the enterprise.

- Segment revenue does not include:

- (a) extraordinary items as defined in AS 5, Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies;

- (b) interest or dividend income, including interest earned on advances or loans to other segments unless the operations of the segment are primarily of a financial nature; and

- (c) gains on sales of investments or on extinguishment of debt unless the operations of the segment are primarily of a financial nature.

5.6 Segment expense is the aggregate of

- (i) the expense resulting from the operating activities of a segment that is directly attributable to the segment, and

- (ii) the relevant portion of enterprise expense that can be allocated on a reasonable basis to the segment, including expense relating to transactions with other segments of the enterprise.

Segment expense does not include:

- (a) extraordinary items as defined in AS 5, Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies;

- (b) interest expense, including interest incurred on advances or loans from other segments, unless the operations of the segment are primarily of a financial nature;

Explanation:

The interest expense relating to overdrafts and other operating liabilities identified to a particular segment are not included as a part of the segment expense unless the operations of the segment are primarily of a financial nature or unless the interest is included as a part of the cost of inventories. In case interest is included as a part of the cost of inventories where it is so required as per AS 16, Borrowing Costs, read with AS 2, Valuation of Inventories, and those inventories are part of segment assets of a particular segment, such interest is considered as a segment expense. In this case, the amount of such interest and the fact that the segment result has been arrived at after considering such interest is disclosed by way of a note to the segment result.

(c) losses on sales of investments or losses on extinguishment of debt unless the operations of the segment are primarily of a financial nature;

(d) income tax expense; and

(e) general administrative expenses, head-office expenses, and other expenses that arise at the enterprise level and relate to the enterprise as a whole. However, costs are sometimes incurred at the enterprise level on behalf of a segment. Such costs are part of segment expense if they relate to the operating activities of the segment and if they can be directly attributed or allocated to the segment on a reasonable basis.

5.7 Segment result is segment revenue less segment expense.

5.8 Segment assets are those operating assets that are employed by a segment in its operating activities and that either are directly attributable to the segment or can be allocated to the segment on a reasonable basis.

If the segment result of a segment includes interest or dividend income, its segment assets include the related receivables, loans, investments, or other interest or dividend generating assets.

Segment assets do not include income tax assets.

Segment assets are determined after deducting related allowances/ provisions that are reported as direct offsets in the balance sheet of the enterprise.

5.9 Segment liabilities are those operating liabilities that result from the operating activities of a segment and that either are directly attributable to the segment or can be allocated to the segment on a reasonable basis.

If the segment result of a segment includes interest expense, its segment liabilities include the related interest-bearing liabilities.

Segment liabilities do not include income tax liabilities.

5.10 Segment accounting policies are the accounting policies adopted for preparing and presenting the financial statements of the enterprise as well as those accounting policies that relate specifically to segment reporting.

6 The factors in paragraph 5 for identifying business segments and geographical segments are not listed in any particular order.

7 A single business segment does not include products and services with significantly differing risks and returns. While there may be dissimilarities with respect to one or several of the factors listed in the definition of business segment, the products and services included in a single business segment are expected to be similar with respect to a majority of the factors.

8 Similarly, a single geographical segment does not include operations in economic environments with significantly differing risks and returns. A geographical segment may be a single country, a group of two or more countries, or a region within a country.

9 The risks and returns of an enterprise are influenced both by the geographical location of its operations (where its products are produced or where its service rendering activities are based) and also by the location of its customers (where its products are sold or services are rendered). The definition allows geographical segments to be based on either:

- (a) the location of production or service facilities and other assets of an enterprise; or

- (b) the location of its customers.

10 The organisational and internal reporting structure of an enterprise will normally provide evidence of whether its dominant source of geographical risks results from the location of its assets (the origin of its sales) or the location of its customers (the destination of its sales). Accordingly, an enterprise looks to this structure to determine whether its geographical segments should be based on the location of its assets or on the location of its customers.

11 Determining the composition of a business or geographical segment involves a certain amount of judgement. In making that judgement, enterprise management takes into account the objective of reporting financial information by segment as set forth in this Standard and the qualitative characteristics of financial statements as identified in the Framework for the Preparation and Presentation of Financial Statements issued by the Institute of Chartered Accountants of India. The qualitative characteristics include the relevance, reliability, and comparability over time of financial information that is reported about the different groups of products and services of an enterprise and about its operations in particular geographical areas, and the usefulness of that information for assessing the risks and returns of the enterprise as a whole.

12 The predominant sources of risks affect how most enterprises are organised and managed. Therefore, the organisational structure of an enterprise and its internal financial reporting system are normally the basis for identifying its segments.

13 The definitions of segment revenue, segment expense, segment assets and segment liabilities include amounts of such items that are directly attributable to a segment and amounts of such items that can be allocated to a segment on a reasonable basis. An enterprise looks to its internal financial reporting system as the starting point for identifying those items that can be directly attributed, or reasonably allocated, to segments. There is thus a presumption that amounts that have been identified with segments for internal financial reporting purposes are directly attributable or reasonably allocable to segments for the purpose of measuring the segment revenue, segment expense, segment assets, and segment liabilities of reportable segments.

14 In some cases, however, a revenue, expense, asset or liability may have been allocated to segments for internal financial reporting purposes on a basis that is understood by enterprise management but that could be deemed arbitrary in the perception of external users of financial statements. Such an allocation would not constitute a reasonable basis under the definitions of segment revenue, segment expense, segment assets, and segment liabilities in this Standard. Conversely, an enterprise may choose not to allocate some item of revenue, expense, asset or liability for internal financial reporting purposes, even though a reasonable basis for doing so exists. Such an item is allocated pursuant to the definitions of segment revenue, segment expense, segment assets, and segment liabilities in this Standard.

15 Examples of segment assets include current assets that are used in the operating activities of the segment and tangible and intangible fixed assets. If a particular item of depreciation or amortisation is included in segment expense, the related asset is also included in segment assets. Segment assets do not include assets used for general enterprise or head-office purposes. Segment assets include operating assets shared by two or more segments if a reasonable basis for allocation exists. Segment assets include goodwill that is directly attributable to a segment or that can be allocated to a segment on a reasonable basis, and segment expense includes related amortisation of goodwill. If segment assets have been revalued subsequent to acquisition, then the measurement of segment assets reflects those revaluations.

16 Examples of segment liabilities include trade and other payables, accrued liabilities, customer advances, product warranty provisions, and other claims relating to the provision of goods and services. Segment liabilities do not include borrowings and other liabilities that are incurred for financing rather than operating purposes. The liabilities of segments whose operations are not primarily of a financial nature do not include borrowings and similar liabilities because segment result represents an operating, rather than a net-of-financing, profit or loss. Further, because debt is often issued at the head-office level on an enterprise-wide basis, it is often not possible to directly attribute, or reasonably allocate, the interest- bearing liabilities to segments.

17 Segment revenue, segment expense, segment assets and segment liabilities are determined before intra-enterprise balances and intra-enterprise transactions are eliminated as part of the process of preparation of enterprise financial statements, except to the extent that such intra-enterprise balances and transactions are within a single segment.

18 While the accounting policies used in preparing and presenting the financial statements of the enterprise as a whole are also the fundamental segment accounting policies, segment accounting policies include, in addition, policies that relate specifically to segment reporting, such as identification of segments, method of pricing inter-segment transfers, and basis for allocating revenues and expenses to segments.

Identifying Reportable Segments

Primary and Secondary Segment Reporting Formats

19 The dominant source and nature of risks and returns of an enterprise should govern whether its primary segment reporting format will be business segments or geographical segments. If the risks and returns of an enterprise are affected predominantly by differences in the products and services it produces, its primary format for reporting segment information should be business segments, with secondary information reported geographically. Similarly, if the risks and returns of the enterprise are affected predominantly by the fact that it operates in different countries or other geographical areas, its primary format for reporting segment information should be geographical segments, with secondary information reported for groups of related products and services.

20 Internal organisation and management structure of an enterprise and its system of internal financial reporting to the board of directors and the chief executive officer should normally be the basis for identifying the predominant source and nature of risks and differing rates of return facing the enterprise and, therefore, for determining which reporting format is primary and which is secondary, except as provided in sub-paragraphs (a) and (b) below:

- (a) if risks and returns of an enterprise are strongly affected both by differences in the products and services it produces and by differences in the geographical areas in which it operates, as evidenced by a ‘matrix approach’ to managing the company and to reporting internally to the board of directors and the chief executive officer, then the enterprise should use business segments as its primary segment reporting format and geographical segments as its secondary reporting format; and

- (b) if internal organisational and management structure of an enterprise and its system of internal financial reporting to the board of directors and the chief executive officer are based neither on individual products or services or groups of related products/services nor on geographical areas, the directors and management of the enterprise should determine whether the risks and returns of the enterprise are related more to the products and services it produces or to the geographical areas in which it operates and should, accordingly, choose business segments or geographical segments as the primary segment reporting format of the enterprise, with the other as its secondary reporting format.

21 For most enterprises, the predominant source of risks and returns determines how the enterprise is organised and managed. Organisational and management structure of an enterprise and its internal financial reporting system normally provide the best evidence of the predominant source of risks and returns of the enterprise for the purpose of its segment reporting. Therefore, except in rare circumstances, an enterprise will report segment information in its financial statements on the same basis as it reports internally to top management. Its predominant source of risks and returns becomes its primary segment reporting format. Its secondary source of risks and returns becomes its secondary segment reporting format.

22 A ‘matrix presentation’ — both business segments and geographical segments as primary segment reporting formats with full segment disclosures on each basis — will often provide useful information if risks and returns of an enterprise are strongly affected both by differences in the products and services it produces and by differences in the geographical areas in which it operates. This Standard does not require, but does not prohibit, a ‘matrix presentation’.

23 In some cases, organisation and internal reporting of an enterprise may have developed along lines unrelated to both the types of products and services it produces, and the geographical areas in which it operates. In such cases, the internally reported segment data will not meet the objective of this Standard. Accordingly, paragraph 20(b) requires the directors and management of the enterprise to determine whether the risks and returns of the enterprise are more product/service driven or geographically driven and to accordingly choose business segments or geographical segments as the primary basis of segment reporting. The objective is to achieve a reasonable degree of comparability with other enterprises, enhance understandability of the resulting information, and meet the needs of investors, creditors, and others for information about product/service-related and geographically- related risks and returns.

Business and Geographical Segments

24 Business and geographical segments of an enterprise for external reporting purposes should be those organisational units for which information is reported to the board of directors and to the chief executive officer for the purpose of evaluating the unit’s performance and for making decisions about future allocations of resources, except as provided in paragraph 25.

25 If internal organisational and management structure of an enterprise and its system of internal financial reporting to the board of directors and the chief executive officer are based neither on individual products or services or groups of related products/services nor on geographical areas, paragraph 20(b) requires that the directors and management of the enterprise should choose either business segments or geographical segments as the primary segment reporting format of the enterprise based on their assessment of which reflects the primary source of the risks and returns of the enterprise, with the other as its secondary reporting format. In that case, the directors and management of the enterprise should determine its business segments and geographical segments for external reporting purposes based on the factors in the definitions in paragraph 5 of this Standard, rather than on the basis of its system of internal financial reporting to the board of directors and chief executive officer, consistent with the following:

- (a) if one or more of the segments reported internally to the directors and management is a business segment or a geographical segment based on the factors in the definitions in paragraph 5 but others are not, sub-paragraph (b) below should be applied only to those internal segments that do not meet the definitions in paragraph 5 (that is, an internally reported segment that meets the definition should not be further segmented);

- (b) for those segments reported internally to the directors and management that do not satisfy the definitions in paragraph 5, management of the enterprise should look to the next lower level of internal segmentation that reports information along product and service lines or geographical lines, as appropriate under the definitions in paragraph 5; and

- (c) if such an internally reported lower-level segment meets the definition of business segment or geographical segment based on the factors in paragraph 5, the criteria in paragraph 27 for identifying reportable segments should be applied to that segment.

26. Under this Standard, most enterprises will identify their business and geographical segments as the organisational units for which information is reported to the board of the directors (particularly the non-executive directors, if any) and to the chief executive officer (the senior operating decision maker, which in some cases may be a group of several people) for the purpose of evaluating each unit’s performance and for making decisions about future allocations of resources. Even if an enterprise must apply paragraph 25 because its internal segments are not along product/service or geographical lines, it will consider the next lower level of internal segmentation that reports information along product and service lines or geographical lines rather than construct segments solely for external reporting purposes. This approach of looking to organisational and management structure of an enterprise and its internal financial reporting system to identify the business and geographical segments of the enterprise for external reporting purposes is sometimes called the ‘management approach’, and the organisational components for which information is reported internally are sometimes called ‘operating segments’.

Reportable Segments

27 A business segment or geographical segment should be identified as a reportable segment if:

- (a) its revenue from sales to external customers and from transactions with other segments is 10 per cent or more of the total revenue, external and internal, of all segments; or

- (b) its segment result, whether profit or loss, is 10 per cent or more of –

- (i) the combined result of all segments in profit, or

- (ii) the combined result of all segments in loss, or

- whichever is greater in absolute amount;

- (c) its segment assets are 10 per cent or more of the total assets of all segments.

28 A business segment or a geographical segment which is not a reportable segment as per paragraph 27, may be designated as a reportable segment despite its size at the discretion of the management of, the enterprise. If that segment is not designated as a reportable segment, it should be included as an unallocated reconciling item.

29 If total external revenue attributable to reportable segments constitutes less than 75 per cent of the total enterprise revenue, additional segments should be identified as reportable segments, even if they do not meet the 10 per cent thresholds in paragraph 27, until at least 75 per cent of total enterprise revenue is included in reportable segments.

30 The 10 per cent thresholds in this Standard are not intended to be a guide for determining materiality for any aspect of financial reporting other than identifying reportable business and geographical segments.

Illustration II attached to this Standard presents an illustration of the determination of reportable segments as per paragraphs 27-29.

31 A segment identified as a reportable segment in the immediately preceding period because it satisfied the relevant 10 per cent thresholds should continue to be a reportable segment for the current period notwithstanding that its revenue, result, and assets all no longer meet the 10 per cent thresholds.

32 If a segment is identified as a reportable segment in the current period because it satisfies the relevant 10 per cent thresholds, preceding-period segment data that is presented for comparative purposes should, unless it is impracticable to do so, be restated to reflect the newly reportable segment as a separate segment, even if that segment did not satisfy the 10 per cent thresholds in the preceding period.

Segment Accounting Policies

33 Segment information should be prepared in conformity with the accounting policies adopted for preparing and presenting the financial statements of the enterprise as a whole.

34 There is a presumption that the accounting policies that the directors and management of an enterprise have chosen to use in preparing the financial statements of the enterprise as a whole are those that the directors and management believe are the most appropriate for external reporting purposes. Since the purpose of segment information is to help users of financial statements better understand and make more informed judgements about the enterprise as a whole, this Standard requires the use, in preparing segment information, of the accounting policies adopted for preparing and presenting the financial statements of the enterprise as a whole. That does not mean, however, that the enterprise accounting policies are to be applied to reportable segments as if the segments were separate stand-alone reporting entities. A detailed calculation done in applying a particular accounting policy at the enterprise-wide level may be allocated to segments if there is a reasonable basis for doing so. Pension calculations, for example, often are done for an enterprise as a whole, but the enterprise-wide figures may be allocated to segments based on salary and demographic data for the segments.

35 This Standard does not prohibit the disclosure of additional segment information that is prepared on a basis other than the accounting policies adopted for the enterprise financial statements provided that (a) the information is reported internally to the board of directors and the chief executive officer for purposes of making decisions about allocating resources to the segment and assessing its performance and (b) the basis of measurement for this additional information is clearly described.

36 Assets and liabilities that relate jointly to two or more segments should be allocated to segments if, and only if, their related revenues and expenses also are allocated to those segments.

37 The way in which asset, liability, revenue, and expense items are allocated to segments depends on such factors as the nature of those items, the activities conducted by the segment, and the relative autonomy of that segment. It is not possible or appropriate to specify a single basis of allocation that should be adopted by all enterprises; nor is it appropriate to force allocation of enterprise asset, liability, revenue and expense items that relate jointly to two or more segments, if the only basis for making those allocations is arbitrary. At the same time, the definitions of segment revenue, segment expense, segment assets and segment liabilities are interrelated, and the resulting allocations should be consistent. Therefore, jointly used assets and liabilities are allocated to segments if, and only if, their related revenues and expenses also are allocated to those segments. For example, an asset is included in segment assets if, and only if, the related depreciation or amortisation is included in segment expense.

Disclosure

38 Paragraphs 39-46 specify the disclosures required for reportable segments for primary segment reporting format of an enterprise. Paragraphs 47-51 identify the disclosures required for secondary reporting format of an enterprise. Enterprises are encouraged to make all of the primary -segment disclosures identified in paragraphs 39-46 for each reportable secondary segment although paragraphs 47-51 require considerably less disclosure on the secondary basis. Paragraphs 53-59 address several other segment disclosure matters. Illustration III attached to this Standard illustrates the application of these disclosure standards.

Explanation:

In case, by applying the definitions of ‘business segment’ and ‘geographical segment’, it is concluded that there is neither more than one business segment nor more than one geographical segment, segment information as per this Standard is not required to be disclosed. However, the fact that there is only one ‘business segment’ and ‘geographical segment’ is disclosed by way of a note.

Primary Reporting Format

39 The disclosure requirements in paragraphs 40-46 should be applied to each reportable segment based on primary reporting format of an enterprise.

40 An enterprise should disclose the following for each reportable segment:

- (a) segment revenue, classified into segment revenue from sales to external customers and segment revenue from transactions with other segments;

- (b) segment result;

- (c) total carrying amount of segment assets;

- (d) total amount of segment liabilities;

- (e) total cost incurred during the period to acquire segment assets that are expected to be used during more than one period (tangible and intangible fixed assets);

- (f) total amount of expense included in the segment result for depreciation and amortisation in respect of segment assets for the period; and

- (g) total amount of significant non-cash expenses, other than depreciation and amortisation in respect of segment assets, that were included in segment expense and, therefore, deducted in measuring segment result.

41 Paragraph 40 (b) requires an enterprise to report segment result. If an enterprise can compute segment net profit or loss or some other measure of segment profitability other than segment result, without arbitrary allocations, reporting of such amount(s) in addition to segment result is encouraged. If that measure is prepared on a basis other than the accounting policies adopted for the financial statements of the enterprise, the enterprise will include in its financial statements a clear description of the basis of measurement.

42 An example of a measure of segment performance above segment result in the statement of profit and loss is gross margin on sales. Examples of measures of segment performance below segment result in the statement of profit and loss are profit or loss from ordinary activities (either before or after income taxes) and net profit or loss.

43 Accounting Standard 5, Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies requires that “when items of income and expense within profit or loss from ordinary activities are of such size, nature or incidence that their disclosure is relevant to explain the performance of the enterprise for the period, the nature and amount of such items should be disclosed separately”. Examples of such items include write- downs of inventories, provisions for restructuring, disposals of fixed assets and long-term investments, legislative changes having retrospective application, litigation settlements, and reversal of provisions. An enterprise is encouraged, but not required, to disclose the nature and amount of any items of segment revenue and segment expense that are of such size, nature, or incidence that their disclosure is relevant to explain the performance of the segment for the period. Such disclosure is not intended to change the classification of any such items of revenue or expense from ordinary to extraordinary or to change the measurement of such items. The disclosure, however, does change the level at which the significance of such items is evaluated for disclosure purposes from the enterprise level to the segment level.

44. An enterprise that reports the amount of cash flows arising from operating, investing and financing activities of a segment need not disclose depreciation and amortisation expense and non-cash expenses of such segment pursuant to sub-paragraphs (f) and (g) of paragraph 40.

45 AS 3 Cash Flow Statements recommends that an enterprise present a cash flow statement that separately reports cash flows from operating, investing and financing activities. Disclosure of information regarding operating, investing and financing cash flows of each reportable segment is relevant to understanding the enterprise’s overall financial position, liquidity, and cash flows. Disclosure of segment cash flow is, therefore, encouraged, though not required. An enterprise that provides segment cash flow disclosures need not disclose depreciation and amortisation expense and non-cash expenses pursuant to sub- paragraphs (f) and (g) of paragraph 40.

46 An enterprise should present a reconciliation between the information disclosed for reportable segments and the aggregated information in the enterprise financial statements. In presenting the reconciliation, segment revenue should be reconciled to enterprise revenue; segment result should be reconciled to enterprise net profit or loss; segment assets should be reconciled to enterprise assets; and segment liabilities should be reconciled to enterprise liabilities.

Secondary Segment Information

47 Paragraphs 39-46 identify the disclosure requirements to be applied to each reportable segment based on primary reporting format of an enterprise. Paragraphs 48-51 identify the disclosure requirements to be applied to each reportable segment based on secondary reporting format of an enterprise, as follows:

- (a) if primary format of an enterprise is business segments, the required secondary-format disclosures are identified in paragraph 48;

- (b) if primary format of an enterprise is geographical segments based on location of assets (where the products of the enterprise are produced or where its service rendering operations are based), the required secondary-format disclosures are identified in paragraphs 49 and 50;

- (c) if primary format of an enterprise is geographical segments based on the location of its customers (where its products are sold or services are rendered), the required secondary-format disclosures are identified in paragraphs 49 and 51.

48 If primary format of an enterprise for reporting segment information is business segments, it should also report the following information:

- (a) segment revenue from external customers by geographical area based on the geographical location of its customers, for each geographical segment whose revenue from sales to external customers is 10 per cent or more of enterprise revenue;

- (b) the total carrying amount of segment assets by geographical location of assets, for each geographical segment whose segment assets are 10 per cent or more of the total assets of all geographical segments; and

- (c) the total cost incurred during the period to acquire segment assets that are expected to be used during more than one period (tangible and intangible fixed assets) by geographical location of assets, for each geographical segment whose segment assets are 10 per cent or more of the total assets of all geographical segments.

49 If primary format of an enterprise for reporting segment information is geographical segments (whether based on location of assets or location of customers), it should also report the following segment information for each business segment whose revenue from sales to external customers is 10 per cent or more of enterprise revenue or whose segment assets are 10 per cent or more of the total assets of all business segments:

- (a) segment revenue from external customers;

- (b) the total carrying amount of segment assets; and

- (c) the total cost incurred during the period to acquire segment assets that are expected to be used during more than one period (tangible and intangible fixed assets).

50 If primary format of an enterprise for reporting segment information is geographical segments that are based on location of assets, and if the location of its customers is different from the location of its assets, then the enterprise should also report revenue from sales to external customers for each customer-based geographical segment whose revenue from sales to external customers is 10 per cent or more of enterprise revenue.

51 If primary format of an enterprise for reporting segment information is geographical segments that are based on location of customers, and if the assets of the enterprise are located in different geographical areas from its customers, then the enterprise should also report the following segment information for each asset-based geographical segment whose revenue from sales to external customers or segment assets are 10 per cent or more of total enterprise amounts:

- (a) the total carrying amount of segment assets by geographical location of the assets; and

- (b) the total cost incurred during the period to acquire segment assets that are expected to be used during more than one period (tangible and intangible fixed assets) by location of the assets.

Illustrative Segment Disclosures

52 Illustration III attached to this Standard Illustrates the disclosures for primary and secondary formats that are required by this Standard.

Other Disclosures

53 In measuring and reporting segment revenue from transactions with other segments, inter-segment transfers should be measured on the basis that the enterprise actually used to price those transfers. The basis of pricing inter-segment transfers and any change therein should be disclosed in the financial statements.

54 Changes in accounting policies adopted for segment reporting that have a material effect on segment information should be disclosed. Such disclosure should include a description of the nature of the change, and the financial effect of the change if it is reasonably determinable.

55 AS 5 requires that changes in accounting policies adopted by the enterprise should be made only if required by statute, or for compliance with an accounting standard, or if it is considered that the change would result in a more appropriate presentation of events or transactions in the financial statements of the enterprise.

56 Changes in accounting policies adopted at the enterprise level that affect segment information are dealt with in accordance with AS 5. AS 5 requires that any change in an accounting policy which has a material effect should be disclosed. The impact of, and the adjustments resulting from, such change, if material, should be shown in the financial statements of the period in which such change is made, to reflect the effect of such change. Where the effect of such change is not ascertainable, wholly or in part, the fact should be indicated. If a change is made in the accounting policies which has no material effect on the financial statements for the current period but which is reasonably expected to have a material effect in later periods, the fact of such change should be appropriately disclosed in the period in which the change is adopted.

57 Some changes in accounting policies relate specifically to segment reporting. Examples include changes in identification of segments and changes in the basis for allocating revenues and expenses to segments. Such changes can have a significant impact on the segment information reported but will not change aggregate financial information reported for the enterprise. To enable users to understand the impact of such changes, this Standard requires the disclosure of the nature of the change and the financial effect of the change, if reasonably determinable.

58 An enterprise should indicate the types of products and services included in each reported business segment and indicate the composition of each reported geographical segment, both primary and secondary, if not otherwise disclosed in the financial statements.

59 To assess the impact of such matters as shifts in demand, changes in the prices of inputs or other factors of production, and the development of alternative products and processes on a business segment, it is necessary to know the activities encompassed by that segment. Similarly, to assess the impact of changes in the economic and political environment on the risks and returns of a geographical segment, it is important to know the composition of that geographical segment.

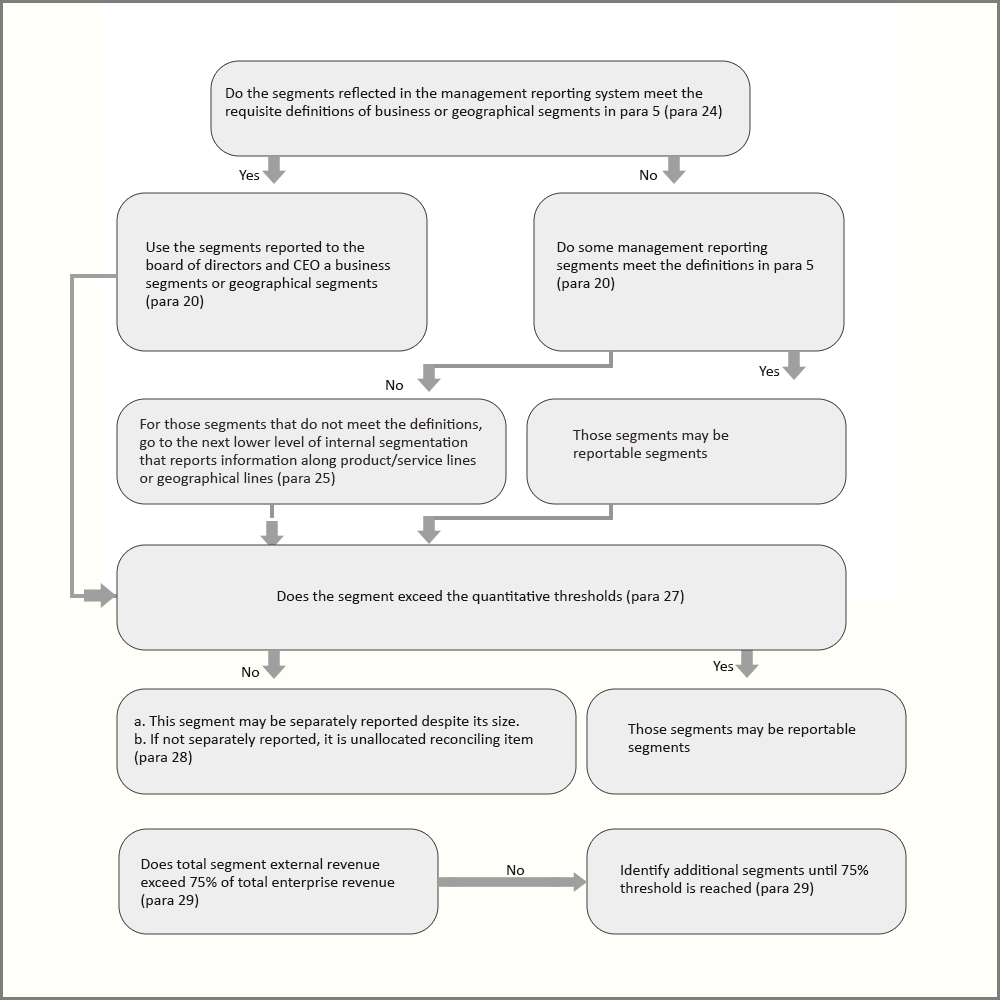

Illustration I

Segment Definition Decision Tree

The purpose of this illustration is illustrate the application of paragraphs (24-32) of the Accounting Standard

Illustration II

Illustration on Determination of ReportableSegments (Paragraphs 27-29)

This illustration does not form part of the Accounting Standard. Its purpose is to illustrate the application of paragraphs 27-29 of the Accounting Standard.

An enterprise operates through eight segments, namely, A, B, C, D, E, F, G and H. The relevant information about these segments is given in the following table (amounts in Rs.’000):

| A | B | C | D | E | F | G | H | Total(Segments) | Total (Enterprise) | |

| 1. SEGMENT REVENUE (a) External Sales | – | 255 | 15 | 10 | 15 | 50 | 20 | 35 | 400 | |

| (b) lnter-segment Sales | 100 | 60 | 30 | 5 | – | – | 5 | – | 200 | |

| (c) Total Revenue | 100 | 315 | 45 | 15 | 15 | 50 | 25 | 35 | 600 | 400 |

| 2. Total Revenue of each segment as a percentage of total revenue of all segments | 16.7 | 52.5 | 7.5 | 2.5 | 2.5 | 8.3 | 4.2 | 5.8 | ||

| 3. SEGMENT RESULT (Profile/Loss) | 5 | (90) | 15 | (5) | 8 | (5) | 5 | 7 | ||

| 4. Combined Result of all Segments in profits | 5 | 15 | 8 | 5 | 7 | 40 | ||||

| 5. Combined Result of an Segments in loss | (90) | (5) | (5) | (100) | ||||||

| 6. Segment Result as a percentage of the greater of the totals arrived at 4 and 5 above in absolute amount(i.e., 100) | 5 | 90 | 15 | 5 | 8 | 5 | 5 | 7 | ||

| 7. SEGMENT ASSETS | 15 | 47 | 5 | 11 | 3 | 5 | 5 | 9 | 100 | |

| 8. Segment assets as a percentage of total assets of all segments | 15 | 47 | 5 | 11 | 3 | 5 | 5 | 9 |

The reportable segments of the enterprise will be identified as below:

(a) In accordance with paragraph 27(a), segments whose total revenue from external sales and inter-segment sales is 10% or more of the total revenue of all segments, external and internal, should be identified as reportable segments. Therefore, Segments A and B are reportable segments.

(b) As per the requirements of paragraph 27(b), it is to be first identified Whether the combined result of all segments in profit or the comb ned result of all segments in loss is greater in absolute amount From the table, it is evident that combined result in loss (i.e. Rs.1,00,000) is greater. Therefore, the individual segment result as a percentage of Rs.1,00,000 needs to be examined. In accordance with paragraph 27(b), Segments B and C are reportable segments as their segment result is more than the threshold limit of 10%.

(c) Segments A,B and D are reportable segments as per paragraph 27(c),as their segment assets are more than 10% of the total segment assets.

Thus,Segments A, B, C, and D are reportable segments in terms of the criteria laid down in paragraph 27.

Paragraph 28 of the Standard gives an option to the management of the enterprise to designate any segment as a reportable segment In the given case, it is presumed that the management decides to designate SegmentE as a reportable segment

Paragraph 29 requires that if total external revenue attributable to reportable segments identified as aforesaid constitutes less than 75% of the total enterprise revenue, additional segments should be identified as reportable segments even if they do not meet the 10% thresholds in paragraph 27, until at least 75% of total enterprise revenue is included in reportable segments.

The total external revenue of Segments A, B, C, D and E-identified above as reportable segments, is Rs.2,95,000. This is less than 75% of total enterprise revenue of Rs.4,00,000. The management of the enterprise is required to designate any one or more of the remaining segments as reportable segment(s) so that the external revenue of reportable segments is at least 75% of the total enterprise revenue Suppose, the management designates Segment H for this purpose. Now the external revenue of reportable segments is more than 75% of the total enterprise revenue.

Segments A, B, C, D, E and H are reportable segments. Segments F and G will be shown as reconciling items.

Illustration III

Illustrative Segment Disclosures

This illustration does not form part of the Accounting Standard- Its purpose is to illustrate the application of paragraphs 38-59 of the Accounting Standard.

This illustration illustrates the segment disclosures that this Standard would require for a diversified multi-locational business enterprise. This example is intentionally complex to illustrate most of the provisions of this Standard.

INFORMATION ABOUT BUSINESS SEGMENTS (NOTE xx)

(All amounts in Rs. Lakhs)

| Paper Product | Office Product | Publishing | Other Operations | Eliminations | Consolidated Total | |||||||

| Current Year | Previous Year | Current Year | Previous Year | Current Year | Previous Year | Current Year | Previous Year | Current Year | Previous Year | Current Year | Previous Year | |

| REVENUE | ||||||||||||

| External Sales | 55 | 50 | 20 | 17 | 19 | 16 | 7 | 7 | ||||

| Inter- segment sales | 15 | 10 | 10 | 14 | 2 | 4 | 2 | 2 | (29) | (30) | ||

| Total Revenue | 70 | 60 | 30 | 31 | 21 | 20 | 9 | 9 | (29) | (30) | 101 | 90 |

| RESULT | ||||||||||||

| Segment result | 20 | 17 | 9 | 7 | 2 | 1 | 0 | 0 | (1) | (1) | 30 | 24 |

| Unallocated corporate expenses | (7) | (9) | ||||||||||

| Operating profit | 23 | 15 | ||||||||||

| Interest expense | (4) | (4) | ||||||||||

| Interest income | 2 | 3 | ||||||||||

| Income taxes | (7) | (4) | ||||||||||

| Profit from ordinary activities | 14 | 10 | ||||||||||

| Extraordinary loss uninsured earthquake damage to factory | (3) | (3) | ||||||||||

| Net profit | 14 | 7 | ||||||||||

| OTHER INFORMATION | ||||||||||||

| Segment assets | 54 | 50 | 34 | 30 | 10 | 10 | 10 | 9 | 108 | 99 | ||

| Unallocated corporate assets | 67 | 56 | ||||||||||

| Total assets | 175 | 155 | ||||||||||

| Segment liabilities | 25 | 15 | 8 | 11 | 8 | 8 | 1 | 1 | 42 | 35 | ||

| Unallocated corporate liabilities | 40 | 55 | ||||||||||

| Total liabilities | 82 | 90 | ||||||||||

| Capital expenditure | 12 | 10 | 3 | 5 | 5 | 4 | 3 | |||||

| Depreciation | 9 | 7 | 9 | 7 | 5 | 3 | 3 | 4 | ||||

| Non-cash expenses other than depreciation | 8 | 2 | 7 | 3 | 2 | 2 | 2 | 1 | ||||

Note xx-Business and Geographical Segments (amounts in Rs-lakhs)

Business segments: For management purposes, the Company is organised on a worldwide basis into three major operating divisionÂpaper products, office products and publishing – each headed by a senior vice president. The divisions are the basis on which the company reports its primary segment information The paper products segment produces a broad range of writing and publishing papers and newsprint The office products segment manufactures labels, binders, pens, and markers and also distributes office products made by others- The publishing segment develops and sells books in the fields of taxation, law and accounting Other operations include development of computer software for standard and specialised business applications. Financial information about business segments is presented in the above table.

Geographical segments: Although the Company’s major operating divisions are managed on a worldwide basis, they operate in four principal geographical areas of the world. In India, its home country, the Company produces and sells a broad range of papers and office products. Additionally, all of the Company’s publishing and computer software development operations are conducted in India. In the European Union, the Company operates paper and office products manufacturing facilities and sales offices in the following countries: France, Belgium, Germany and the UK Operations in Canada and the United States are essentially similar and consist of manufacturing papers and news print that are sold entirely within those two countries. Operations in Indonesia include the production of paper pulp and the manufacture of writing and publishing papers and office products, almost all of which is sold outside Indonesia, both to other segments of the company and to external customers.

Sales by market: The following table shows the distribution of the Company’s consolidated sales by geographical market regardless of where the goods were produced:

| Sales Revenue by Geographical Market | ||

| Current Year | Previous Year | |

| India | 19 | 22 |

| European Union | 30 | 31 |

| Canada and the United States | 28 | 21 |

| Mexico and South America | 6 | 2 |

| Southeast Asia (principally Japan and Taiwan) | 18 | 14 |

| 90 | ||

Assets and additions to tangible and intangible fixed assets by geographical area: The following table shows the carrying amount of segment assets and additions to tangible and intangible fixed assets by geographical area in which the assets are located:

| Carrying Amount of Segment Assets | Additions of Fixed Assets and Intangible Assets | |||

| Current Year | Previous Year | Current Year | Previous Year | |

| India | 72 | 78 | 8 | 5 |

| European Union | 47 | 37 | 5 | 4 |

| Canada and the United States | 34 | 20 | 4 | 3 |

| Indonesia | 22 | 20 | 7 | 6 |

| 175 | 155 | 24 | 18 | |

Segment revenue and expense: In India, paper and office products are manufactured in combined facilities and are sold by a combined sales force. Joint revenues and expenses are allocated to the two business segments on a reasonable basis. All other segment revenue and expense are directly attributable to the segments.

Segment assets and liabilities: Segment assets include all operating assets used by a segment and consist principally of operating cash, debtors, inventories and fixed assets, net of allowances and provisions which are reported as direct offsets in the balance sheet. While most such assets can be directly attributed to individual segments, the carrying amount of certain assets used jointly by two or more segments is allocated to the segments on a reasonable basis. Segment liabilities include all operating liabilities and consist principally of creditors and accrued liabilities. Segment assets and liabilities do not include deferred income taxes.

Inter-segment transfers: Segment revenue, segment expenses and segment result include transfers between business segments and between geographical segments. Such transfers are accounted for at competitive market prices charged to unaffiliated customers for similar goods. Those transfers are eliminated in consolidation.

Unusual item: Sales of office products to external customers in the current year were adversely affected by a lengthy strike of transportation workers in India, which interrupted product shipments for approximately four months. The Company estimates that sales of office products during the four-month period were approximately half of what they would otherwise have been.

Extraordinary loss: As more fully discussed in Note x, the Company incurred an uninsured loss of Rs.3,00,000 caused by earthquake damage to a paper mill in India during the previous year.

Illustration IV

Summary of Required Disclosure

This illustration does not form part of the Accounting Standard. Its purpose is to summarise the disclosures required by paragraphs 38-59 for each of the three possible primary segment reporting formats.

Figures in parentheses refer to paragraph numbers of the relevant paragraphs in the text.

PRIMARY FORMAT IS BUSINESS SEGMENTS | PRIMARY FORMAT IS GEOGRAPHICAL SEGMENTS BY LOCATION OF ASSETS | PRIMARY FORMAT IS GEOGRAPHICAL SEGMENTS BY LOCATION OF CUSTOMERS |

Required Primary Disclosures | Required Primary Disclosures | Required Primary Disclosures |

Revenue from external customers by business segment [40(a)] | Revenue from external customers by location of assets [40(a)] | Revenue from external customers by location of customers [40(a)] |

Revenue from transactions with other segments by business segment [40(a)] | Revenue from transactions with other segments by location of assets [40(a)] | Revenue from transactions with other segments by location of customers [40(a)] |

Segment result by business segment [40(b)] | Segment result by location of assets [40(b)] | Segment result by location of customers [40(b)] |

Carrying amount of segment assets by business segment [40(c)] | Carrying amount of segment assets by location of assets [40(c)] | Carrying amount of segment assets by location of customers [40(c)] |

Segment liabilities by business segment [40(d)] | Segment liabilities by location of assets [40(d)] | Segment liabilities by location of customers [40(d)] |

Cost to acquire tangible and intangible fixed assets by business segment [40(e)] | Cost to acquire tangible and intangible fixed assets by location of assets [40(e)] | Cost to acquire tangible and intangible fixed assets by location of customers [40(e)] |

Depreciation and amortisation expense by business segment [40(f)] | Depreciation and amortisation expense by location of assets[40(f)] | Depreciation and amortisation expense by location of customers[40(f)] |

Non-cash expenses other than depreciation and amortisation by business segment [40(g)] | Non-cash expenses other than depreciation and amortisation by location of assets [40(g)] | Non-cash expenses other than depreciation and amortisation by location of customers [40(g)] |

Reconciliation of revenue, result, assets, and liabilities by business segment [46] | Reconciliation of revenue, result, assets, and liabilities [46] | Reconciliation of revenue, result, assets, and liabilities [46] |

Revenue from external customers by location of customers [48] | Revenue from external customers by business segment [49] | Revenue from external customers by business segment [49] |

Carrying amount of segment assets by location of assets [48] | Carrying amount of segment assets by business segment [49] | Carrying amount of segment assets by business segment [49] |

Cost to acquire tangible and intangible fixed assets by location of assets [48] | Cost to acquire tangible and intangible fixed assets by business segment [49] | Cost to acquire tangible and intangible fixed assets by business segment [49] |

Revenue from external customers by geographical customers if different from location of assets [50] | ||

Carrying amount of segment assets by location of assets if different from location of customers [51] | ||

Cost to acquire tangible and intangible fixed assets by location of assets if different from location of customers [51] | ||

Other Required Disclosures | Other Required Disclosures | Other Required Disclosures |

Basis of pricing inter- segment transfers and any change therein [53] | Basis of pricing inter- segment transfers and any change therein [53] | Basis of pricing inter- segment transfers and any change therein [53] |

Changes in segment accounting policies [54] | Changes in segment accounting policies [54] | Changes in segment accounting policies [54] |

Types of products and services in each business segment [58] | Types of products and services in each business segment [58] | Types of products and services in each business segment [58] |

Composition of each geographical segment [58] | Composition of each geographical segment [58] | Composition of each geographical segment [58] |