Reporting and analyzing financial metrics is necessary to understand your business’s financial health. Gross revenue represents the total amount of revenue earned from all your income sources and is a useful tool for calculating sales, predicting business growth and attracting lenders or investors.Gross revenue, also known as gross income, is the sum of all money generated by a business, without taking into account any part of that total that has been or will be used for expenses. As such, gross revenue includes not just money made from the sale of goods and services but also from interest, sale of shares, exchange rates and sales of property and equipment.

What is gross revenue?

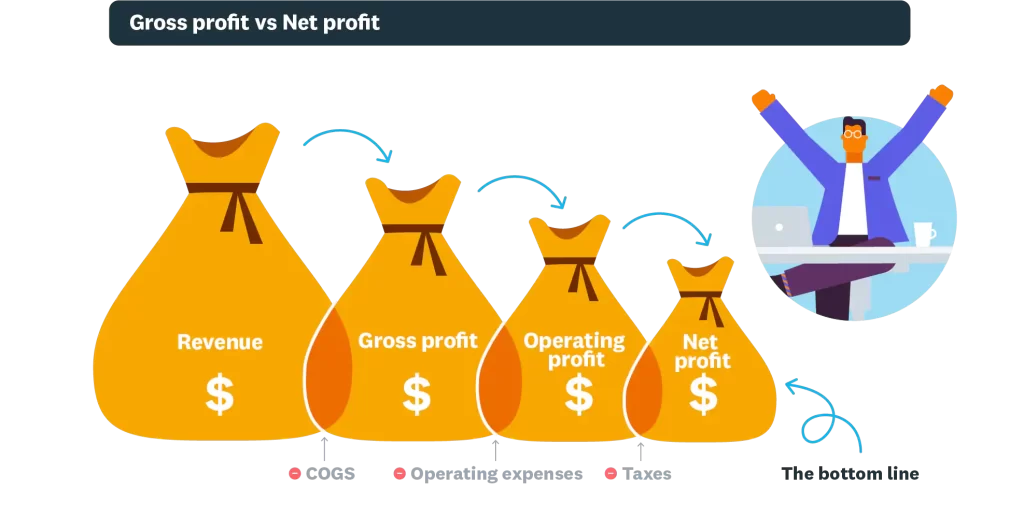

Gross revenue refers to the total amount of revenue earned in a given reporting period. Found on the first line of your income statement, gross revenue is also called the top line. Gross revenue factors into business profits, but relates only to money earned from sales and doesn’t account for any other expenses, such as cost of goods sold (COGS) or overhead.

Gross revenue is often used interchangeably with other similar terms, such as gross profit, cash flow or total sales. The key difference between gross revenue and these terms is that revenue represents the total amount your business receives without accounting for any expenses, and other terms relate to subsets of income.

Gross revenue vs. Net revenue

Gross revenue and net revenue are often considered together, but they describe different aspects of an organization’s financial health.

Where gross revenue is the top line of the income statement, net revenue is the bottom line. It subtracts all expenses incurred during operation and production, such as COGS, taxes or loan interest, from gross revenue to determine net income or profit. When gross and net revenue are understood together, they can illustrate an organization’s profitability and financial performance.

The general formula for net revenue is: Gross revenue ($100,000) – total expenses ($40,000) = net revenue ($60,000)

Why is gross revenue important?

Although it doesn’t account for operating costs or COGS, gross revenue is an important metric that assesses your organization’s profitability and financial performance. Even before businesses turn a profit, changes in gross revenue can indicate and predict business growth and can be considered against other profitability metrics, including gross profit and net income.

Gross revenue also demonstrates your company’s potential to external stakeholders. Investors and financial partners consider revenue in relation to other metrics to determine if the company is a secure investment.

Likewise, banks, lenders and credit card companies factor your business’s growth revenue into your credit applications. Consistent or growing revenue shows lenders that your business can reliably repay loans. Stagnant or declining revenue may cause difficulties in acquiring credit as lenders may see your loan as high-risk.

How to calculate gross revenue

1. Determine the reporting period- Begin by setting a period of time for your gross revenue reporting. Businesses typically calculate gross revenue yearly, quarterly or monthly as part of required income statements, but you can calculate it as often as your business strategy requires.

2. Identify all income sources- Identify all the income sources your business had over the established time period. Include product sales, services sold, shares and any other income streams your business might have.

For example, if a customer pays for $1,200 of services over one year and your business calculates gross revenue quarterly, this income stream is calculated at $300 per quarter.

3. Add income together- Add all of your income streams together. This total is your gross revenue.

Example: Your business earns $20,000 from in-store sales, $30,000 from online sales and $5,000 from investment dividends. The gross revenue is $55,000.

Evaluating gross revenue

- Know your audience: When determining what fiscal information to present along with gross revenue, consider who the information is for. Income statements for stakeholders better describe your business’s financial health when they include gross revenue in conjunction with net revenue, operating costs or other information.

- Internal use: You should evaluate gross revenue periodically to set targets and to better inform your business growth and sales strategies.

- Include all income: Remember to include all forms of income, such as in-store sales, online sales, investment income, royalties and other revenue sources.

- Track gross revenue: Track your gross revenue at consistent intervals to see if your business is growing or struggling in certain financial aspects.

How an obligor changes revenue reporting

a primary obligor is an organization that provides a product or service to another business. Understanding this relationship is an important part of revenue reporting.

For example, Business A manufactures computers and is responsible for production costs, inventory and credit risk. Business A sets its own prices, negotiates with suppliers and fulfills orders independently.

To sell its computers, Business A enters an agreement with Business B, which agrees to sell Business A’s computers alongside products made by other manufacturers. Business B’s website includes a disclaimer that the company bears no responsibility for the shipping or quality of products. Business B notifies Business A of any sales, and Business A ships products to buyers.

In this example, Business A is the primary obligor and reports gross revenue on its income statements. Business B isn’t the primary obligor and reports sales as net revenue.

FAQs

What’s the difference between gross revenue vs. gross profit?

Gross revenue is the company’s total revenue without any losses or costs deducted. Typically only accounting for variable costs instead of fixed costs, gross profit is a metric describing gross revenue minus COGS. Gross profit is likewise different from net profit, which considers all organizational expenses. It’s used to assess a company’s labor and resource efficiency in manufacturing goods or providing services.

What’s the difference between gross revenue and cash flow?

Gross revenue represents all income streams that your business receives, including sales, royalties and interests. Cash flow refers to money going in and out of businesses. Gross revenue is included in cash flow calculations, and investors, lenders and stakeholders often consider this calculation when assessing your organization’s financial health.

Are net revenue and net income the same thing?

No, net revenue refers to gross revenue minus expenses related to the sale. Your net income is the amount of money left over after all of your expenses are subtracted from your net revenue. On an income statement, the net income will usually be the bottom line.

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Penalty Notice u/s 271(1)(c) | Income Tax Notice u/s 142(1) | Income Tax Notice u/s 144 |Income Tax Notice u/s 148 | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida

Complete CA Services

RERA Services

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | 115bac | section 41 of income tax act | GST Search Taxpayer | 194h | section 185 of companies act 2013 | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | 194r | ec tamilnadu | 194a of income tax act | 80ddb | aaple sarkar portal | epf activation | scrap business | brsr | section 135 of companies act 2013 | depreciation on computer | section 186 of companies act 2013 | 80ttb | section 115bab | section 115ba | section 148 of income tax act | 80dd | 44ae of Income tax act | west bengal land registration | 194o of income tax act | 270a of income tax act | 80ccc | traces portal | 92e of income tax act | 142(1) of Income Tax Act | 80c of Income Tax Act | Directorate general of GST Intelligence | form 16 | section 164 of companies act | section 194a | section 138 of companies act 2013 | section 133 of companies act 2013