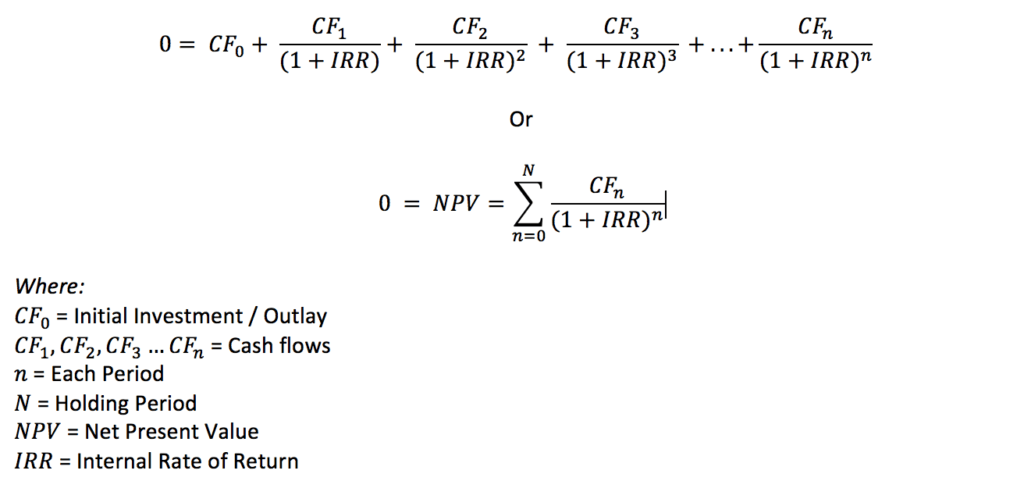

The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

What Is IRR?

IRR, or internal rate of return, is a metric used in financial analysis to estimate the profitability of potential investments. IRR is a discount rate that makes the net present value (NPV) of all cash flows equal to zero in a discounted cash flow analysis.

IRR calculations rely on the same formula as NPV does. Keep in mind that IRR is not the actual dollar value of the project. It is the annual return that makes the NPV equal to zero.Generally speaking, the higher an internal rate of return, the more desirable an investment is to undertake. IRR is uniform for investments of varying types and, as such, can be used to rank multiple prospective investments or projects on a relatively even basis. In general, when comparing investment options with other similar characteristics, the investment with the highest IRR probably would be considered the best.

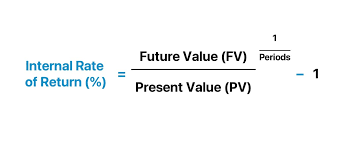

The Formula for IRR

The IRR formula is as follows:

Calculating the internal rate of return can be done in three ways:

- Using the IRR or XIRR function in Excel or other spreadsheet programs (see example below)

- Using a financial calculator

- Using an iterative process where the analyst tries different discount rates until the NPV equals zero (Goal Seek in Excel can be used to do this)

What Is IRR Used For?

In capital planning, one popular scenario for IRR is comparing the profitability of establishing new operations with that of expanding existing operations. For example, an energy company may use IRR in deciding whether to open a new power plant or to renovate and expand an existing power plant.

While both projects could add value to the company, one will likely be the more logical decision as prescribed by IRR. Note that because IRR does not account for changing discount rates, it’s often not adequate for longer-term projects with discount rates that are expected to vary.IRR is also useful for corporations in evaluating stock buyback programs. Clearly, if a company allocates substantial funding to repurchasing its shares, then the analysis must show that the company’s own stock is a better investment—that is, has a higher IRR—than any other use of the funds, such as creating new outlets or acquiring other companies.

Individuals can also use IRR when making financial decisions—for instance, when evaluating different insurance policies using their premiums and death benefits. The consensus is that policies that have the same premiums and a high IRR are much more desirable.

Note that life insurance has a very high IRR in the early years of the policy—often more than 1,000%. It then decreases over time. This IRR is very high during the early days of the policy because if you made only one monthly premium payment and then suddenly died, your beneficiaries would still get a lump sum benefit.

Another common use of IRR is in analyzing investment returns. In most cases, the advertised return will assume that any interest payments or cash dividends are reinvested back into the investment. What if you don’t want to reinvest dividends but need them as income when paid? And if dividends are not assumed to be reinvested, are they paid out, or are they left in cash? What is the assumed return on the cash? IRR and other assumptions are particularly important on instruments like annuities, where the cash flows can become complex.

Finally, IRR is a calculation used for an investment’s money-weighted rate of return (MWRR). The MWRR helps determine the rate of return needed to start with the initial investment amount factoring in all of the changes to cash flows during the investment period, including sales proceeds.

Using IRR With WACC

Most IRR analyses will be done in conjunction with a view of a company’s weighted average cost of capital (WACC) and NPV calculations. IRR is typically a relatively high value, which allows it to arrive at an NPV of zero.

Most companies will require an IRR calculation to be above the WACC. WACC is a measure of a firm’s cost of capital in which each category of capital is proportionately weighted. All sources of capital, including common stock, preferred stock, bonds, and any other long-term debt, are included in a WACC calculation.In theory, any project with an IRR greater than its cost of capital should be profitable. In planning investment projects, firms will often establish a required rate of return (RRR) to determine the minimum acceptable return percentage that the investment in question must earn to be worthwhile. The RRR will be higher than the WACC.Any project with an IRR that exceeds the RRR will likely be deemed profitable, although companies will not necessarily pursue a project on this basis alone. Rather, they will likely pursue projects with the highest difference between IRR and RRR, as these will likely be the most profitable.

Limitations of IRR

IRR is generally ideal for use in analyzing capital budgeting projects. It can be misconstrued or misinterpreted if used outside of appropriate scenarios. In the case of positive cash flows followed by negative ones and then by positive ones, the IRR may have multiple values. Moreover, if all cash flows have the same sign (i.e., the project never turns a profit), then no discount rate will produce a zero NPV.Within its realm of uses, IRR is a very popular metric for estimating a project’s annual return; however, it is not necessarily intended to be used alone. IRR is typically a relatively high value, which allows it to arrive at an NPV of zero. The IRR itself is only a single estimated figure that provides an annual return value based on estimates. Since estimates of IRR and NPV can differ drastically from actual results, most analysts will choose to combine IRR analysis with scenario analysis. Scenarios can show different possible NPVs based on varying assumptions.As mentioned, most companies do not rely on IRR and NPV analyses alone. These calculations are usually also studied in conjunction with a company’s WACC and an RRR, which provides for further consideration. Companies usually compare IRR analysis to other tradeoffs. If another project has a similar IRR with less up-front capital or simpler extraneous considerations, then a simpler investment may be chosen despite IRRs.

In some cases, issues can also arise when using IRR to compare projects of different lengths. For example, a project of a short duration may have a high IRR, making it appear to be an excellent investment. Conversely, a longer project may have a low IRR, earning returns slowly and steadily. The ROI metric can provide some more clarity in these cases, although some managers may not want to wait out the longer time frame.

Investing Based on IRR

The internal rate of return rule is a guideline for evaluating whether to proceed with a project or investment. The IRR rule states that if the IRR on a project or investment is greater than the minimum RRR—typically the cost of capital, then the project or investment can be pursued.

Conversely, if the IRR on a project or investment is lower than the cost of capital, then the best course of action may be to reject it. Overall, while there are some limitations to IRR, it is an industry standard for analyzing capital budgeting projects.

FAQs

What Does Internal Rate of Return Mean?

The internal rate of return (IRR) is a financial metric used to assess the attractiveness of a particular investment opportunity. When you calculate the IRR for an investment, you are effectively estimating the rate of return of that investment after accounting for all of its projected cash flows together with the time value of money. When selecting among several alternative investments, the investor would then select the investment with the highest IRR, provided it is above the investor’s minimum threshold. The main drawback of IRR is that it is heavily reliant on projections of future cash flows, which are notoriously difficult to predict.

What Is a Good Internal Rate of Return?

Whether an IRR is good or bad will depend on the cost of capital and the opportunity cost of the investor. For instance, a real estate investor might pursue a project with a 25% IRR if comparable alternative real estate investments offer a return of, say, 20% or lower. However, this comparison assumes that the riskiness and effort involved in making these difficult investments are roughly the same. If the investor can obtain a slightly lower IRR from a project that is considerably less risky or time-consuming, then they might happily accept that lower-IRR project. In general, though, a higher IRR is better than a lower one, all else being equal.

Is IRR the Same as ROI?

Although IRR is sometimes referred to informally as a project’s “return on investment,” it is different from the way most people use that phrase. Often, when people refer to ROI, they are simply referring to the percentage return generated from an investment in a given year or across a period. However, that type of ROI does not capture the same nuances as IRR, and for that reason, IRR is generally preferred by investment professionals.

Another advantage of IRR is that its definition is mathematically precise, whereas the term ROI can mean different things depending on the context or the speaker.

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Penalty Notice u/s 271(1)(c) | Income Tax Notice u/s 142(1) | Income Tax Notice u/s 144 |Income Tax Notice u/s 148 | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Complete CA Services

RERA Services

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | 115bac | section 41 of income tax act | GST Search Taxpayer | 194h | section 185 of companies act 2013 | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | 194r | ec tamilnadu | 194a of income tax act | 80ddb | aaple sarkar portal | epf activation | scrap business | brsr | section 135 of companies act 2013 | depreciation on computer | section 186 of companies act 2013 | 80ttb | section 115bab | section 115ba | section 148 of income tax act | 80dd | 44ae of Income tax act | west bengal land registration | 194o of income tax act | 270a of income tax act | 80ccc | traces portal | 92e of income tax act | 142(1) of Income Tax Act | 80c of Income Tax Act | Directorate general of GST Intelligence | form 16 | section 164 of companies act | section 194a | section 138 of companies act 2013 | section 133 of companies act 2013

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Penalty Notice u/s 271(1)(c) | Income Tax Notice u/s 142(1) | Income Tax Notice u/s 144 |Income Tax Notice u/s 148 | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Complete CA Services

RERA Services

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | 115bac | section 41 of income tax act | GST Search Taxpayer | 194h | section 185 of companies act 2013 | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | 194r | ec tamilnadu | 194a of income tax act | 80ddb | aaple sarkar portal | epf activation | scrap business | brsr | section 135 of companies act 2013 | depreciation on computer | section 186 of companies act 2013 | 80ttb | section 115bab | section 115ba | section 148 of income tax act | 80dd | 44ae of Income tax act | west bengal land registration | 194o of income tax act | 270a of income tax act | 80ccc | traces portal | 92e of income tax act | 142(1) of Income Tax Act | 80c of Income Tax Act | Directorate general of GST Intelligence | form 16 | section 164 of companies act | section 194a | section 138 of companies act 2013 | section 133 of companies act 2013