The Risk Free Rate (rf) is the theoretical rate of return received on zero-risk assets, which serves as the minimum return required on riskier investments. The rate should reflect the yield to maturity (YTM) on default-free government bonds of equivalent maturity as the duration of the projected cash flows.

What Is the Risk-Free Rate of Return?

The risk-free rate of return is the theoretical rate of return of an investment with zero risk. The risk-free rate represents the interest an investor would expect from an absolutely risk-free investment over a specified period of time.The so-called “real” risk-free rate can be calculated by subtracting the current inflation rate from the yield of the Treasury bond matching your investment duration.

In theory, the risk-free rate is the minimum return an investor expects for any investment. Investors will not accept additional risk unless the potential rate of return is greater than the risk-free rate. If you are finding a proxy for the risk-free rate of return, you must consider the investor’s home market. Negative interest rates can complicate the issue.

How to Calculate Risk Free Rate (rf)?

For corporate valuations, the majority of risk/return models begin with the presumption that there is a so-called “risk free rate”.

Despite the fact that the return expected by investors is considered to be risk-free, it is important to remember that the risk-free rate is a mere simplification, as all investments carry some degree of risk.

However, government-issued bonds are logically about as close to being risk-free as an asset could get, as governments could simply print more money if necessary.As a result of being secured by a central government, the probability of default on such bond issuances is practically zero – and therefore, government bonds are viewed as the safest asset class that investors could place their capital in.

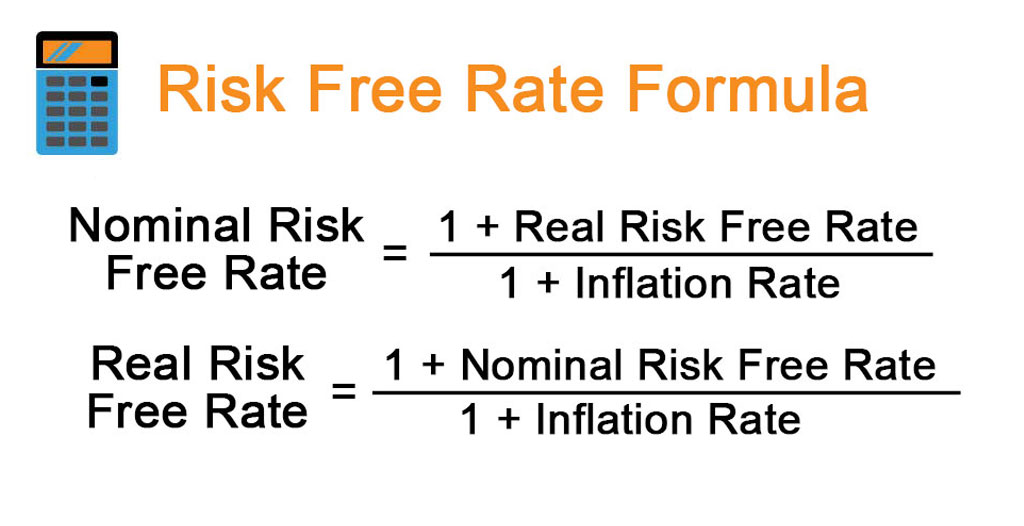

Risk Free Rate Formula (rf)

To expand further on the risk-free rate, there are two different types to consider:

- Real Risk-Free Rate

- Nominal Risk-Free Rate

The reasoning behind these two concepts is related to the inclusion (or exclusion) of the rate of inflation.

The real risk-free rate is the required return on zero-risk financial instruments with the rate of inflation taken into account.

The relationship between the real and the nominal risk-free rate is depicted by the following equation:

The nominal risk-free rate refers to the yield on a risk-free asset without the effect of inflation.

If the projected cash flows are discounted in nominal terms (i.e. reflects expected inflation), the discount rate used should also be nominal.

What is the Role of the Risk Free Rate in CAPM?

The risk-free rate has a significant role in the capital asset pricing model (CAPM), which is the most widely used model for estimating the cost of equity.Under the CAPM, the expected return on a risky asset is estimated as the risk-free rate plus an approximated equity risk premium. The minimum threshold for return factors in the beta of the specific asset (i.e. systematic, non-diversifiable risk) and the average return of the stock market.

The risk-free rate serves as the minimum rate of return, to which the excess return (i.e. the beta multiplied by the equity risk premium) is added.

The equity risk premium (ERP) is calculated as the average market return (S&P 500) minus the risk-free rate.

The equity risk premium helps investors evaluate potential investments based on the “extra” return that they are receiving for the incremental risk above the rf rate.

How Does the Risk-Free Rate Affect Discount Rate?

The risk-free rate assumption is also a key input in the estimation of the weighted average cost of capital (WACC) of a company.

The CAPM estimates the cost of equity based on the risk-free rate of return and the additional risk (and required return) associated with the investment. But the cost of debt can also be estimated by adding a certain spread based on the risk profile (i.e. default risk premium) of the company to the risk-free rate.

If the risk-free rate increases, there will be increased pressure on the equity risk premium to compensate investors more for the amount of risk undertaken (and vice versa).Since investors can receive higher returns from risk-free assets, riskier assets are expected to result in higher returns to meet the new standards set by the market for the returns of riskier assets.

FAQs

Why is the risk-free rate important?

The risk-free rate is important because it provides a baseline for comparing the returns of other investments. Investors use the risk-free rate as a reference point to assess the risk and potential reward of various investment opportunities.

What investment is considered risk-free?

Typically, short-term government securities issued by stable and creditworthy governments are considered risk-free investments.

How is the risk-free rate determined?

The risk-free rate is influenced by various factors, including monetary policy, inflation expectations, and market demand for safe assets. Central banks, such as the Federal Reserve in the United States, play a significant role in setting short-term interest rates, which in turn affect the risk-free rate.

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Penalty Notice u/s 271(1)(c) | Income Tax Notice u/s 142(1) | Income Tax Notice u/s 144 |Income Tax Notice u/s 148 | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Complete CA Services

RERA Services

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | 115bac | section 41 of income tax act | GST Search Taxpayer | 194h | section 185 of companies act 2013 | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | 194r | ec tamilnadu | 194a of income tax act | 80ddb | aaple sarkar portal | epf activation | scrap business | brsr | section 135 of companies act 2013 | depreciation on computer | section 186 of companies act 2013 | 80ttb | section 115bab | section 115ba | section 148 of income tax act | 80dd | 44ae of Income tax act | west bengal land registration | 194o of income tax act | 270a of income tax act | 80ccc | traces portal | 92e of income tax act | 142(1) of Income Tax Act | 80c of Income Tax Act | Directorate general of GST Intelligence | form 16 | section 164 of companies act | section 194a | section 138 of companies act 2013 | section 133 of companies act 2013

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Penalty Notice u/s 271(1)(c) | Income Tax Notice u/s 142(1) | Income Tax Notice u/s 144 |Income Tax Notice u/s 148 | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Complete CA Services

RERA Services

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | 115bac | section 41 of income tax act | GST Search Taxpayer | 194h | section 185 of companies act 2013 | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | 194r | ec tamilnadu | 194a of income tax act | 80ddb | aaple sarkar portal | epf activation | scrap business | brsr | section 135 of companies act 2013 | depreciation on computer | section 186 of companies act 2013 | 80ttb | section 115bab | section 115ba | section 148 of income tax act | 80dd | 44ae of Income tax act | west bengal land registration | 194o of income tax act | 270a of income tax act | 80ccc | traces portal | 92e of income tax act | 142(1) of Income Tax Act | 80c of Income Tax Act | Directorate general of GST Intelligence | form 16 | section 164 of companies act | section 194a | section 138 of companies act 2013 | section 133 of companies act 2013