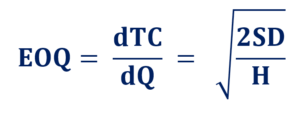

The Economic Order Quantity formula is calculated by minimizing the total cost per order by setting the first-order derivative to zero. The components of the formula that make up the total cost per order are the cost of holding inventory and the cost of ordering that inventory. The key notations in understanding the EOQ formula are as follows:

Components of the EOQ Formula:

D: Annual Quantity Demanded

Q: Volume per Order

S: Ordering Cost (Fixed Cost)

C: Unit Cost (Variable Cost)

H: Holding Cost (Variable Cost)

i: Carrying Cost (Interest Rate)

Ordering Cost

The number of orders that occur annually can be found by dividing the annual demand by the volume per order. The formula can be expressed as:

For each order with a fixed cost that is independent of the number of units, S, the annual ordering cost is found by multiplying the number of orders by this fixed cost. It is expressed as:

Holding Cost

Holding inventory often comes with its own costs. This cost can be in the form of direct costs incurred by financing the storage of said inventory or the opportunity cost of holding inventory instead of investing the money elsewhere. As such, the holding cost per unit is often expressed as the cost per unit multiplied by the interest rate, expressed as follows:

H = iC

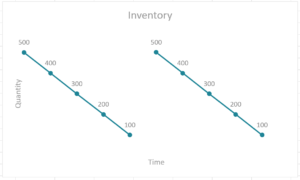

With the assumption that demand is constant, the quantity of stock can be seen to be depleting at a constant rate over time. When inventory reaches zero, an order is placed and replenishes inventory as shown:

As such, the holding cost of the inventory is calculated by finding the sum product of the inventory at any instant and the holding cost per unit. It is expressed as follows:

Total Cost and the Economic Order Quantity

Summing the two costs together gives the annual total cost of orders. To find the optimal quantity that minimizes this cost, the annual total cost is differentiated with respect to Q. It is shown as follows: