Appreciation is an increase in the value of an asset over time. The term is widely used in several disciplines, including economics, finance, and accounting.

In accounting, appreciation refers to the positive adjustment made to the initially booked value of an asset. Moreover, accountants determined additional criteria to define the concept:

- The new value of an asset is higher than its depreciable cost.

- The value of an asset increases due to some market or economic conditions.

- The increase in the value of an asset does not result from improving or adding to the asset.

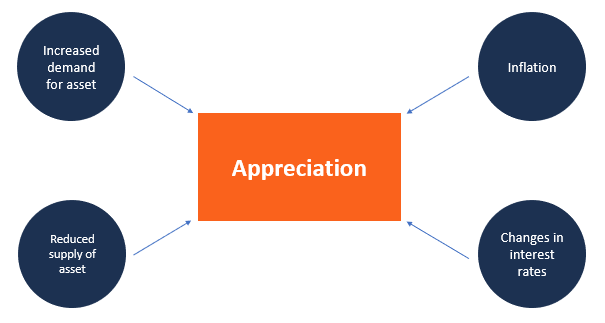

What Is Appreciation?

Appreciation, in general terms, is an increase in the value of an asset over time. The increase can occur for a number of reasons, including increased demand or weakening supply, or as a result of changes in inflation or interest rates. This is the opposite of depreciation, which is a decrease in value over time.

Appreciation can be used to refer to an increase in any type of asset, such as a stock, bond, currency, or real estate. For example, the term capital appreciation refers to an increase in the value of financial assets such as stocks, which can occur for reasons such as improved financial performance of the company.

Just because the value of an asset appreciates does not necessarily mean its owner realizes the increase. If the owner revalues the asset at its higher price on their financial statements, this represents a realization of the increase.

Another type of appreciation is currency appreciation. The value of a country’s currency can appreciate or depreciate over time in relation to other currencies.

How to Calculate the Appreciation Rate

The appreciation rate is virtually the same as the compound annual growth rate (CAGR). Thus, you take the ending value, divide by the beginning value, then take that result to 1 dividend by the number of holding periods (e.g. years). Finally, you subtract one from the result. However, in order to calculate the appreciation rate that means you need to know the initial value of the investment and the future value. You also need to know how long the asset will appreciate.

Appreciation vs. Depreciation

Appreciation is also used in accounting when referring to an upward adjustment of the value of an asset held on a company’s accounting books. The most common adjustment on the value of an asset in accounting is usually a downward one, known as depreciation.

Certain assets are given to appreciation, while other assets tend to depreciate over time. As a general rule, assets that have a finite useful life depreciate rather than appreciate.

Depreciation is typically done as the asset loses economic value through use, such as a piece of machinery being used over its useful life. While appreciation of assets in accounting is less frequent, assets such as trademarks may see an upward value revision due to increased brand recognition.

Real estate, stocks, and precious metals represent assets purchased with the expectation that they will be worth more in the future than at the time of purchase. By contrast, automobiles, computers, and physical equipment gradually decline in value as they progress through their useful lives.

FAQs

What Is an Appreciating Asset?

An appreciating asset is any asset which value is increasing. For example, appreciating assets can be real estate, stocks, bonds, and currency.

What Is Appreciation Rate?

Appreciation rate is another word for growth rate. The appreciation rate is the rate at which an asset’s value grows.

What Is a Good Home Appreciation Rate?

A good appreciation rate is relative to the asset and risk involved. What might be a good appreciation rate for real estate is different than what is a good appreciation rate for a certain currency given the risk involved.

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Penalty Notice u/s 271(1)(c) | Income Tax Notice u/s 142(1) | Income Tax Notice u/s 144 |Income Tax Notice u/s 148 | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Complete CA Services

RERA Services

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | 115bac | section 41 of income tax act | GST Search Taxpayer | 194h | section 185 of companies act 2013 | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | 194r | ec tamilnadu | 194a of income tax act | 80ddb | aaple sarkar portal | epf activation | scrap business | brsr | section 135 of companies act 2013 | depreciation on computer | section 186 of companies act 2013 | 80ttb | section 115bab | section 115ba | section 148 of income tax act | 80dd | 44ae of Income tax act | west bengal land registration | 194o of income tax act | 270a of income tax act | 80ccc | traces portal | 92e of income tax act | 142(1) of Income Tax Act | 80c of Income Tax Act | Directorate general of GST Intelligence | form 16 | section 164 of companies act | section 194a | section 138 of companies act 2013 | section 133 of companies act 2013 | rtps | patta chitta