Reverse charge mechanism (RCM) under GST refers to the situation where the liability to pay tax for the supply of goods or services shifts from the supplier to the recipient, particularly in specific cases involving purchases from unregistered dealers.

This mechanism aims to broaden tax collection, especially in unorganised sectors, and covers certain services imports.

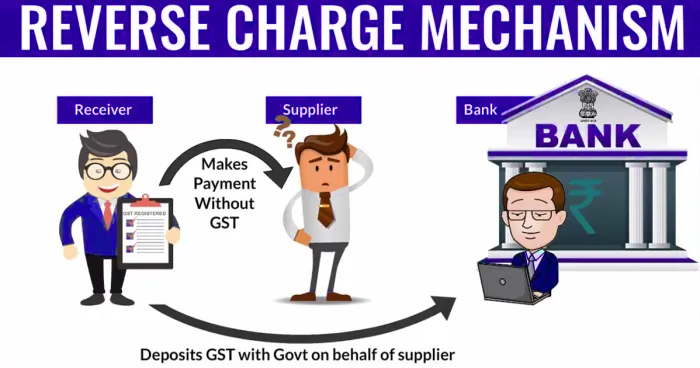

What is Reverse Charge Mechanism?

The supplier of goods or services pays the tax on supply. Under the reverse charge mechanism, the recipient of goods or services becomes liable to pay the tax, i.e., the chargeability gets reversed.

The objective of shifting the burden of GST payments to the recipient is to widen the scope of levy of tax on various unorganized sectors, to exempt specific classes of suppliers, and to tax the import of services (since the supplier is based outside India).

Reverse Charge Mechanism Example

Example 1

XYZ Pvt Ltd, a registered company, purchases raw cashews worth ₹50,000 from an unregistered farmer. Since the farmer doesn’t charge GST, XYZ Pvt Ltd is responsible for paying GST under RCM. The company calculates 5% GST, amounting to ₹2,500, and pays it directly to the government. It later includes this amount in its GST liability when filing tax returns.

Example 2

An SME registered under GST hires an unregistered freelancer for website design services worth ₹20,000. Since the freelancer doesn’t charge GST, the SME is responsible for paying it under RCM. The SME calculates 18% GST, amounting to ₹3,600, and pays it directly to the government. It later includes this amount in its GST liability when filing tax returns.

Different Types of Reverse Charges Under GST

1. Forward Charge

In a forward charge scenario, the supplier collects the tax from the customer and then pays it to the tax authorities.

For example, if a car manufacturing company sells auto parts worth ₹1,00,000 to a trader, it collects GST from the trader and later pays it to the government. This is the standard process for most transactions under GST.

2. Backward Charge

The reverse charge or backward charge method is less common but is used in specific situations to ensure tax compliance and increase tax revenues. Under the GST reverse charge, the recipient of the service becomes responsible for paying the tax directly to the government.

For example, if a chartered accountant provides professional services worth ₹50,000 to a client, it is the client who is liable to pay GST under this mechanism.

Several services fall under reverse charge on GST:

- Goods transport agency (GTA) services

- Legal services

- Rent-a-car services

- Manpower supply services

- Import of taxable services

- Security services

- Service portion in execution of works contract

- Sponsorship services

When is Reverse Charge under GST Applicable

| Supply from Unregistered or Registered Dealers – | Reverse Charge will occur if a seller who is not registered for GST supplied products to an individual who is registered for GST. This ensures that the GST would have to be billed directly to the government by the recipient rather than the seller. The licensed dealer who is required to pay GST under reverse charge must self-invoice for sales made. The customer would pay IGST on interstate sales. The customer must pay CGST and SGST on intra-state purchases under RCM. |

| Services through eCommerce Operators – | Where an e-commerce operator provides facilities, the e-commerce operator would be subject to a reverse charge. He would be required to pay GST. For eg, UrbanClap offers the services of plumbers, electricians, teachers, beauticians, and other professionals. Instead of licensed service providers, UrbanClap is required to pay GST and receive it from consumers. If the e-commerce operator does not have a physical presence in the taxable jurisdiction, a person representing such an e-commerce operator for any reason must pay tax. If there is no official, the operator will nominate one who will be responsible for GST. |

| CBEC-specified supply of such goods and services – | The CBEC has published a list of products and services that are subject to a reverse payment. |

This case is reversed when the individual purchasing the goods and services is required to pay taxes. If the recipient purchases products from an unregistered provider, GST must be charged on their behalf. The retailer must give a payment voucher to the receiver. According to Section 2(94) of the CGST Act, 2017, the recipient must be a registered individual.

According to Section 2(98) of the CGST Act of 2017, a “reverse charge” is the obligation to pay tax by the purchaser of delivery of products or services or both rather than the seller of those goods or services or both.

Who Needs to GST in Reverse Charge Mechanism

According to GST rules, the person supplying the goods must indicate on the tax invoice whether or not tax is payable under the RCM. When making GST payments under RCM, keep the following points in mind:

- The ITC on the tax amount paid under RCM can be claimed by the recipient of goods or services only if such goods or services are utilised for business or furthering of business.

- When discharging duty under RCM, a composition dealer shall pay tax at the regular rates, not the composition rates. They are also ineligible to claim any input tax credit for taxes paid.

- The GST compensation cess can be applied to the RCM tax payable or paid.

Current RCM under GST

In the current situation, the reverse charge process is used in service tax for utilities such as insurance agents, manpower supply, and goods transport agencies, among others. In contrast to the Service Tax, there is no definition of a partial reversal fee. The recipient would pay the full amount of tax on the supply.

Previously, it was difficult to raise service tax from the various unorganized markets, equivalent to goods transportation. The attempt has been made to position the facilities in accordance with the current system, and as a result, compliance and tax revenues can be improved by the reverse charge process.

The reverse fee is now available on all goods and services.

Goods supplied under the Reverse Charge Mechanism

| S.No. | Description of supply of goods | Supplier | Recipient |

| 1 | Bidi wrapper | Agriculturist | Any Registered Person |

| 2 | Cashew Nuts | Agriculturist | Any Registered Person |

| 3 | Tobacco Leaves | Agriculturist | Any Registered Person |

| 4 | Supply of Lottery | State Government, Union Territory or any local authority | Lottery distributor or selling agent |

| 5 | Silk Yarn | A person who manufactures silk yarn. | Any Registered Person |

| 6 | Priority Sector Lending Certificate | Any Registered Person | Any Registered Person |

| 7 | Raw Cotton | Agriculturist | Any Registered Person |

| 8 | Used vehicles, seized & Confiscated goods | Central Govt or State Govt. Union Territory or the local Authority | Any Registered Person |

RCM GST List For Services

| SL. NO | Provider | Recipient |

| 1 | Director of a company or a body corporate | Company or the body corporate |

| 2 | Recovery Agent | Banking Company, NBFC or financial institutions |

| 3 | Goods transport agency | Casual Taxable person, body corporate, partnership firm, any society, factory, and persons registered under CGST, SGST, IGST Act |

| 4 | An insurance agent | Persons carrying on insurance business |

| 5 | Individual advocate or firm of advocates | Any business entity |

FAQs

How is RCM calculated?

RCM is calculated based on the applicable GST rates using the formula: (Value of Goods/Services) x (Applicable GST Rate). You can also make use of the GST calculator online to get the GST rate of the product or services.

How do I claim reverse charge on GSTR 3b?

Recipients must report their GST liability under RCM in Table 3.1 D of GSTR-3B. They can later claim an Input Tax Credit (ITC) for these transactions in Table 4A of GSTR-3B for the same month.