AGM full form, stands for Annual General Meeting and is a crucial company compliance event designed to facilitate communication between a company’s management and its shareholders. The Companies Act of 2013 mandates the convening of an AGM to deliberate on matters such as annual financial results, the appointment of auditors, and other relevant issues. In accordance with the Companies Act of 2013, a company must adhere to the prescribed procedures for conducting the AGM.

An Annual General Meeting (AGM) is a crucial requirement for certain companies under the Companies Act, 2013. It serves as a formal gathering where shareholders review the company’s financial performance, approve key decisions, and ensure corporate accountability. The AGM provides a platform for transparency and helps in fostering trust among shareholders, directors, and management.

The Companies Act, 2013 is a comprehensive legislation that regulates the functioning of companies in India. One of the significant requirements of the Act is conducting an Annual General Meeting (AGM) by companies. The Annual General Meeting (AGM) is an important event for every company as it provides an opportunity for the shareholders to interact with the management and get an update on the company’s performance. The Companies Act, 2013 (the Act) mandates every company to hold an AGM every year within six months from the end of the financial year.

Meaning of the Annual General Meeting (AGM)

n Annual General Meeting, in Company Law, is an interaction between a company’s shareholders and directors. During this meeting, shareholders with voting rights have the Authority to propose and vote on motions.

- Legal Requirement: The AGM is mandated by law, and all companies must hold it yearly.

- Shareholder Participation: It encourages shareholders to participate in the company’s affairs actively.

- Financial Check: Shareholders review and approve the company’s financial statements to ensure accuracy.

- Auditors and Directors: Decisions about auditors and directors are made during the AGM.

- Compensation and Dividends: Compensation for officers and dividend payments are discussed and approved.

- Open Discussion: Shareholders can also raise any other concerns or issues.

Importance of Annual General Meeting

The AGM is an essential corporate event as it provides an opportunity for shareholders to meet the company’s management, ask questions, and clarify doubts regarding the company’s performance and future plans. It also allows shareholders to vote on critical matters, such as the Appointment of Directors, approval of the company’s financial statements, and the declaration of dividends. The AGM ensures transparency and accountability in the functioning of a company, and it is an effective way to strengthen the relationship between the company and its shareholders.

The AGM is an important event in the life of a company for various reasons:

- Transparent communication: The AGM provides an opportunity for the management to transparently communicate with shareholders about the company’s financial performance, future plans, and any other pertinent information.

- Accountability: The AGM enables shareholders to hold the management accountable for its actions and decisions.

- Democracy: The AGM upholds the democratic principles of a company by giving shareholders the right to vote on key issues and resolutions.

- Compliance: Conducting an Annual General Meeting as per Companies Act is mandatory, and failure to do so can result in legal consequences.

Legal Requirement of AGM

As per Section 96 of the Companies Act, 2013, every company except a One Person Company (OPC) is required to conduct an AGM each year. The first AGM of a company must be held within nine months from the end of the first financial year, and in such a case, there is no need to conduct another AGM in that year. For subsequent years, the AGM must be held within six months from the end of the financial year, ensuring that the gap between two AGMs does not exceed fifteen months.

Mandatory provisions related to Annual General Meeting

- Notice of Meeting: The company must issue a notice of the AGM to all its members at least 21 days before the meeting. The notice must include the date, time, and venue of the meeting, along with the agenda.

- Quorum: The quorum for an AGM should be either five members or 1/3rd of the total members, whichever is lower. If the quorum is not present, the meeting will stand adjourned.

- Business to be Transacted: The business to be transacted at the AGM includes the approval of the annual financial statements, the appointment of auditors, and the declaration of dividends.

- Voting: Shareholders can vote either by show of hands or by a poll. In case of a poll, the voting can be done through electronic means also.

- Timing: An AGM must be held within six months from the end of the financial year. However, the Registrar of Companies (ROC) can grant an extension of up to three months.

- Agenda: The agenda of the AGM must include matters such as the approval of the annual report, declaration of dividends, appointment or reappointment of directors, and any other business that requires shareholder approval.

Companies Required to Hold an AGM

Except for One-Person Companies (OPCs), every company must have an AGM at the conclusion of each fiscal year. The AGM must be held within six months of the conclusion of the fiscal year.

In the event of the first general meeting of the year, however, the company may have an AGM within nine months after the conclusion of the first fiscal year. There is no requirement to convene an AGM in the year of establishment if the first AGM has already been held. It is critical to remember that the time interval between the two annual general meetings should not exceed 15 months.

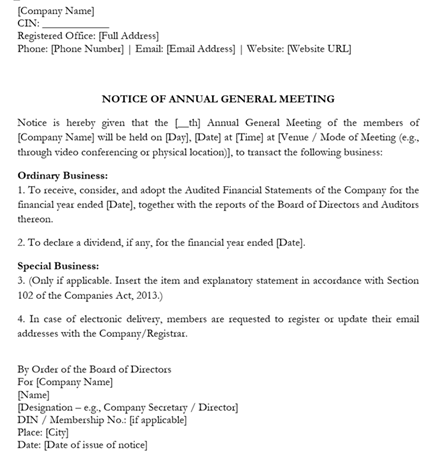

Notice of AGM

As per the Companies Act, every company is required to send a notice convening the AGM to its stakeholders at least 21 clear days prior to the date of the meeting. The notice must clearly state the date, time, venue, and agenda of the meeting.

The notice must be sent to the following persons:

- All shareholders, including legal representatives of deceased members and assignees of insolvent members;

- Statutory auditor(s) of the company; and

- All directors of the company.

The mode of delivery can include registered post, speed post, electronic communication, or hand delivery, and must be sent to the address or email as per the company’s official records.

In case of electronic communication, the notice should be sent to the member’s registered email address and may be included either as the body of the email or as an attachment. Furthermore, the company is required to publish the notice on its official website or any other platform prescribed by the government.

While a minimum of 21 days’ notice is generally mandatory, an AGM may be convened at shorter notice if 95% or more of the shareholders entitled to vote consent to it. Such consent may be given in writing or through electronic means.

The format of the notice is as shown:

Agenda of the AGM?

The primary objective of an AGM is to enable shareholders to participate in key decision-making processes. Some of the major business matters discussed in an AGM include:

- Approval of Financial Statements: The board presents the audited financial statements, including the balance sheet, profit and loss account, and cash flow statement, for approval. These statements must be prepared in accordance with Schedule III of the Companies Act, 2013 and relevant accounting standards.

- Declaration of Dividends: If the company generates sufficient profits, the shareholders decide on the distribution of dividends to reward investors. The final dividend is usually recommended by the Board of Directors and approved by shareholders in the AGM.

- Appointment or Reappointment of Directors: In companies where directors retire by rotation, the AGM provides an opportunity for their reappointment or replacement. As per Section 152(6) of the Act, one-third of the directors (except independent and nominee directors) must retire in rotation every year, and they can be re-elected by the shareholders.

- Appointment or Reappointment of Auditors: Under Section 139 of the Companies Act, 2013, auditors are appointed for a term of five years. However, their appointment must be ratified by shareholders in every AGM. If necessary, a new auditor can be appointed, provided they meet the eligibility criteria specified in the Act.

- Review of Company Performance: The board presents an annual report, highlighting financial performance, operational achievements, corporate governance initiatives, and future plans. This allows shareholders to evaluate the company’s progress and provide feedback.

The matters discussed or business transacted in an AGM consists of:

- Consideration and adoption of the audited financial statements.

- Consideration of the Director’s report and auditor’s report.

- Dividend declaration to shareholders.

- Appointment of directors to replace the retiring directors.

- Appointment of auditors and deciding the auditor’s remuneration.

- Apart from the above ordinary business, any other business may be conducted as a special business of the company.

The ordinary business of the company will be passed by an ordinary resolution where the votes cast in favour are more than the votes cast against the resolution.

However, in case of special business transactions, the resolution may be passed as an ordinary resolution or a special resolution, depending on the applicable legal provisions. A special resolution requires at least 75% votes in favour of the resolution.

An AGM should be conducted during the business hours between 9 a.m. and 6 p.m. only. The meeting can be conducted on any day, which is not a national holiday, including holidays declared by the Central Government. The meeting can be held at any place which is within the limits of the city or town or village in which the registered office is situated.

A government company can also hold its AGM at any other place as the Central Government may approve. An unlisted company can hold an AGM at any place in India after obtaining consent from its members in writing or in electronic mode. In the case of a Section 8 company, the Board decides the date, time and place of the AGM as per the directions given in a general meeting of the company.

Procedure of Conducting an AGM

The chairperson of the Board of Directors generally presides over the meeting. If the chairperson is absent, the directors present elect a chairperson for the meeting. The meeting proceeds as per the agenda mentioned in the notice. Shareholders are encouraged to ask questions and seek clarifications on financial matters and company policies.

For an AGM to be legally valid, a quorum must be present. As per Section 103 of the Companies Act, 2013, the quorum for a private company is two members personally present. In the case of a public company, the quorum varies based on the number of members:

- If the company has less than 1,000 members, at least 5 members must be present.

- If there are 1,000 to 5,000 members, at least 15 members are required.

- If the company has more than 5,000 members, at least 30 members must be present.

If the quorum is not met within half an hour of the scheduled time, the meeting is adjourned to the next scheduled date unless stated otherwise in the Articles of Association.

Extension of the AGM Deadline

The Registrar of Companies (RoC) has the authority to grant an extension of up to three months for holding an AGM, excluding the first AGM. To avail of this extension, a company must submit an application detailing the reasons for the delay and the period of extension required. The RoC will assess the application and, if satisfied with the justification, may approve the extension.

Common reasons for seeking an extension include mergers and acquisitions, delays in finalizing financial statements, unavailability of auditors due to unforeseen circumstances, loss of data due to technical issues, natural calamities, or other significant disruptions impacting the company’s operations.

During exceptional situations, such as the COVID-19 pandemic, the Ministry of Corporate Affairs (MCA) issued directives allowing for a general extension of the AGM deadline. For instance, for the financial year ending on March 31, 2020, the MCA directed the RoCs to extend the AGM deadline by three months without requiring individual applications from companies

Minutes of the Annual General Meeting

Every company is required to prepare the minutes of its AGM, which serve as a written record of the meeting’s proceedings, including resolutions passed and key decisions taken. These minutes must be recorded by the Company Secretary, or if unavailable, by a person authorised by the Board or Chairman.

The minutes must be signed and entered in the minutes book within 30 days of the AGM and kept at the company’s registered office or another approved location. Members can inspect the minutes upon request and payment of a prescribed fee. A copy of the minutes must be provided within seven days of a member’s request.

Failure to comply attracts penalties: ₹25,000 on the company and ₹5,000 on each defaulting officer. These minutes carry legal significance and ensure transparency and accountability in the company’s governance.

Minutes are an official written record, either physical or electronic, of a meeting’s proceedings. A Minutes Book is a book that is kept in either electronic or physical form to record Minutes.

Reporting of the AGM

After a company holds its AGM, it has to officially inform the RoC about the meeting and what was decided there.

This is done by filing Form MGT-15, which includes:

- Details of the AGM, such as the date, time, and venue.

- The resolutions passed (like approval of financial statements, appointment of auditors, etc.).

- An explanatory statement, which explains the reasons behind the resolutions.

This report must be submitted within 30 days from the date the AGM was held.

Filing this form ensures transparency and keeps the company compliant with the legal requirements under the Companies Act, 2013.

Consequences and Penalty for Default in Holding an AGM

Failure to hold an AGM within the prescribed period can result in serious consequences. Under Section 99 of the Companies Act, 2013, the company may be liable to a fine of up to ₹1,00,000, and every officer responsible for the default may be fined up to ₹5,000 for each day of non-compliance. The RoC has the authority to initiate legal proceedings against the defaulting company and its officers.

Moreover, shareholders can file a complaint before the National Company Law Tribunal (NCLT), seeking directions to compel the company to conduct the AGM. If a company persistently fails to hold AGMs, it may risk deregistration or further legal action from regulatory authorities.

Importance of AGMs in Corporate Governance

AGMs play a pivotal role in corporate governance, ensuring that management remains accountable to shareholders. They enhance transparency by providing investors with insights into the company’s financial health and strategic direction. Shareholders get an opportunity to voice their opinions, vote on crucial matters, and influence corporate decisions.

AGMs also help in building investor confidence, as companies that consistently hold these meetings demonstrate their commitment to legal and ethical business practices. Additionally, regulatory bodies such as the Securities and Exchange Board of India (SEBI) closely monitor AGM proceedings, especially in publicly listed companies, ensuring investor protection.

Recent Developments and Virtual AGMs

With the rise of digital transformation, the Ministry of Corporate Affairs (MCA) introduced provisions for virtual AGMs amid the COVID-19 pandemic. The MCA allowed companies to conduct electronic AGMs (E-AGMs) through video conferencing or other online platforms. These virtual meetings helped companies maintain compliance while ensuring shareholder participation.

In certain cases, hybrid models, where both physical and virtual participation are allowed, have been encouraged to improve accessibility. However, companies must comply with MCA guidelines, including maintaining proper records of virtual proceedings and ensuring data security.

Conclusion

The Annual General Meeting is a statutory obligation that companies must fulfill to maintain transparency, ensure shareholder participation, and uphold good governance. Under the Companies Act, 2013, AGMs provide a structured framework for reviewing financial performance, approving major decisions, and safeguarding investor interests.

Companies that adhere to AGM regulations benefit from enhanced investor trust, legal compliance, and better corporate reputation. As business environments evolve, AGMs continue to be a cornerstone of corporate democracy, bridging the gap between management and stakeholders. Proper planning, adherence to legal requirements, and effective communication during AGMs contribute to the overall success and sustainability of the company.

About the Author

This article is written by CA Bhuvnesh Kumar Goyal, a seasoned Chartered Accountant with over 15 years of experience in taxation, GST, MSME advisory, startups, and audits. He specializes in company registration, ESG, BRSR, and the Companies Act, helping businesses stay compliant while optimizing their financial efficiency with expert guidance.