Salary Hike Calculator

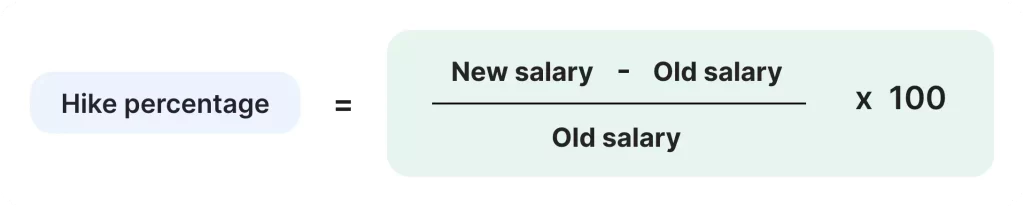

A salary hike, also known as an increment is an increase in the current wage by a fixed percentage. This is expressed as a percentage of the current salary and is known as the percentage hike. A salary hike refers to an increment in salary. It includes upward adjustment of a person’s compensation package. It is usually given by an employer based on important factors like an employee’s performance, his experience, inflation, or fluctuations in the job market. Salary hikes are important achievements in an employee’s career. It shows recognition for their contributions and provides them with opportunities for increased financial stability and professional growth.. What is a salary hike? A salary hike is an addition to an employee’s compensation besides the bonus. Employers use salary hikes to adjust base salaries and compensation regularly. This type of salary increase is distinct from bonuses and commissions, which are typically performance-based. A salary hike typically recognises an employee’s long service to a company and reflects changes in the employee’s responsibilities towards them. Salary Hike Calculator Work Input Current Salary Details: Users can start by entering their current salary data into the calculator. This includes their current salary amount, any extra benefits or allowances received, and other details like bonuses or commissions. Enter Proposed Salary Adjustments: After that, users input the proposed salary adjustments. This could include factors such as a percentage increase in salary, a fixed amount of raise, or any changes in benefits or allowances. Calculate Salary Hike Percentage: Once the current and proposed salary details are entered, the calculator applies a predefined formula to calculate the percentage increase in salary. This formula typically involves subtracting the current salary from the new salary, dividing it by the current salary, and then multiplying by 100 to obtain the percentage increase. Display Updated Salary Amount: After the calculation is complete, the calculator displays the updated salary amount post-hike. This provides users with a clear understanding of how their salary has changed and what their new income level will be. Optional Features: Some advanced Salary Hike Calculators may offer additional features such as comparison tools to analyze different salary hike scenarios, charts or graphs to visualize the impact of salary adjustments, and options to factor in tax implications or other financial considerations. How to Calculate Salary Hike Percentage? Determine Current Salary: Start by identifying the individual’s current salary. This could be their annual salary, monthly salary, or any other period-specific amount. Identify New Salary: Next, determine the new or proposed salary after the hike. This could be the result of a salary increase, promotion, or any other change in compensation. Calculate the Difference: Find the difference between the new salary and the current salary. This can be done by subtracting the current salary from the new salary. Calculate Percentage Increase: Divide the difference obtained in step 3 by the current salary. Then, multiply the result by 100 to express it as a percentage. Formula to calculate hike percentage (New salary – Old salary) * 100 / (Old salary) = Salary hike percentage Here is an example to help you understand:Suppose your monthly salary was ₹30,000 and your new salary is ₹36,000. The salary increase would be ₹35,000 – ₹30,000 = ₹6,000. Here, the hike percentage would become (₹6,000100) / ₹30,000 = 20%. Common reasons for salary hike Displaying a good work ethic and positive attitude: A positive attitude and a strong work ethic can help you influence and improve the performance of your colleagues. Managers reward employees who uphold ethical standards and are diligent, as this fosters productive engagement within the organisation. Inspiring and challenging your colleagues: Employees who exhibit leadership abilities and understand their teammates’ motivations are likely to be the next generation of managers and senior staff. A salary hike is one way to motivate them to stay with the company. Being proactive: Performing tasks without being asked and trying to boost your skills and knowledge can help you become a greater asset to the company. When you are proactive and can identify what the company has set as a criterion for a salary hike, you can fulfil them and increase your prospect of receiving an increment. FAQs When was the last time you received a salary hike? The date you started your job and the last time you received a raise can also affect your chances of receiving a successful salary increase. If you joined the business recently, or if you have received a raise within the last six months, your employer may not consider your request for a pay increase. It may be a good time to request a raise if you have not received one in years and have continued to take on more responsibility at work and perform well. If you believe you are due for a raise, consider the following to help you gauge your progress and quantify it in terms of the deserved salary hike: Collect all information about your work history and increasing responsibilities, including dates and amounts of previous hikes. Compile a list of your significant accomplishments and completed projects since your last salary hike. What makes me deserving of a hike? By asking yourself why you deserve a raise, you can determine your major objectives. Perhaps you deserve a raise because of the value you bring to the company, or you wish to earn additional money to increase your disposable income. When requesting a salary increase, it is crucial to exhibit your value to the organisation. If you believe that you deserve a salary hike, it can be easier to convince your employer for the same. With the following tips, you can request an adequate raise: Compare your compensation to the national average for the same role. This can help you establish a starting point for salary negotiations. Compile a list of initiatives you have taken, your skills and expertise that can benefit the company and use it to determine your eligibility for a raise.

Salary Hike Calculator Read More »