What is Form 16

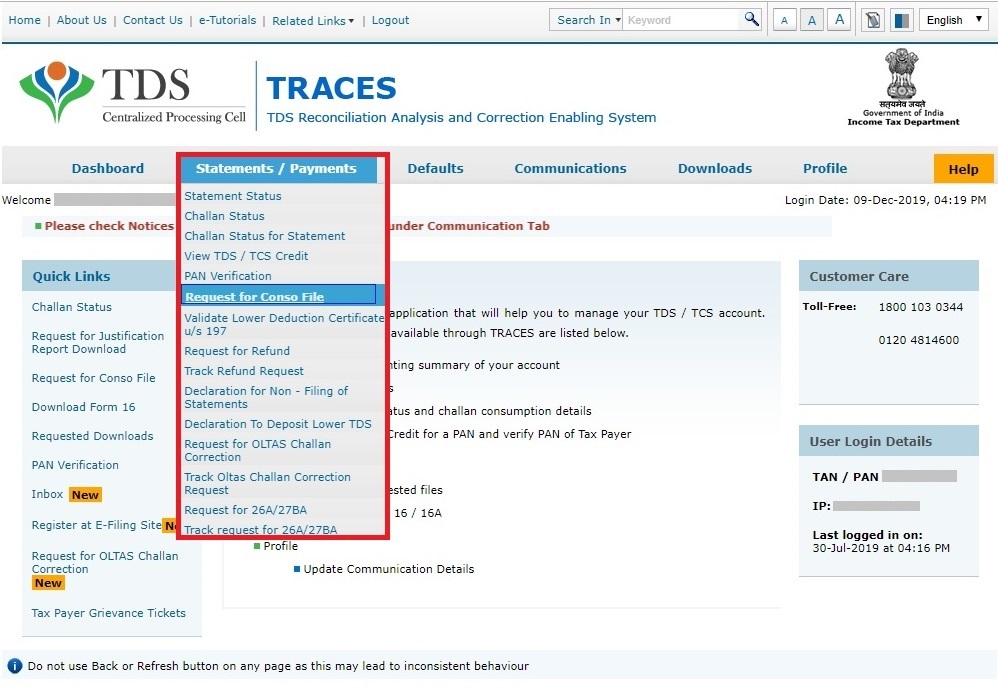

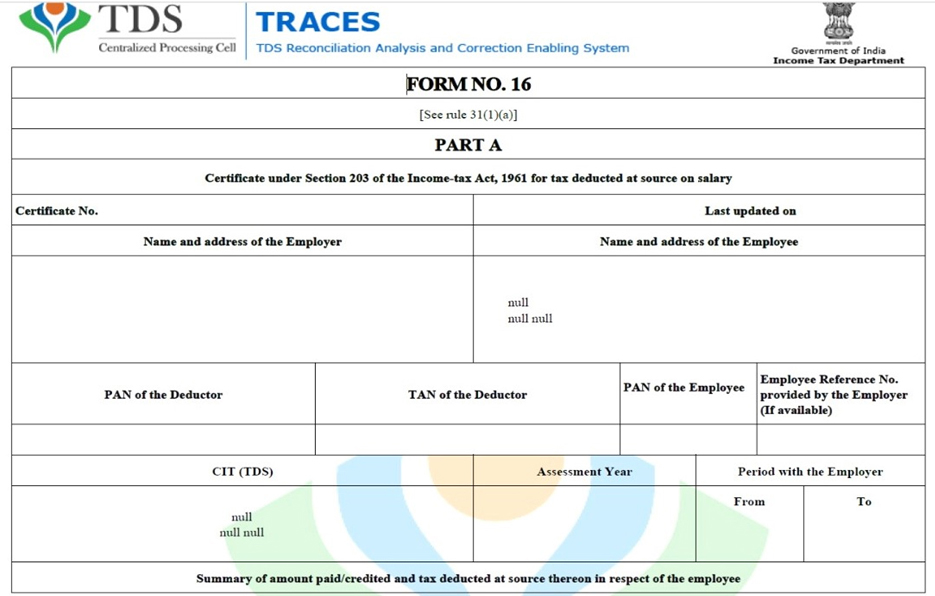

Form 16 is a document issued under Section 203 of the Income Tax Act 1961. It is issued by an employer to their employee and serves as a certificate of Tax Deducted at Source (TDS) on salary income. It ensures that the employer successfully submits the TDS to the Income Tax Department. Simply put, Form 16 is a certificate that provides a detailed summary of the following heads in a particular financial year (April to March): Salary earned by an employee Allowances Deductions Taxes paid on the employee’s behalf Form 16 is a certificate that denotes the fine breakup of salary income and the Tax Deducted at Source amount deducted by the employer. It is associated with Income tax and is used by companies to provide their salaried individuals’ information on the tax deducted. In simple words, Form 16 means a document provided by your employer that certifies the salary details earned during a particular year and how much TDS has been deducted. Form 16 is among the necessary forms for salaried individuals when it comes to taxation. It comprises all crucial information related to one’s salary and accumulated tax amount deducted by the issuer. What makes the said form so important is its role in filing ITR, among others. What is Form 16 in Income Tax Form 16 is a certificate that contains vital information required to file income tax returns. An employer issues it every year on or before 15 June of the next year, immediately after the financial year in which the tax is getting deducted. This certificate is issued according to Section 203 of the Income Tax Act 1961. Form 16 is also known as a salary TDS certificate and comprises details related to the salary paid by an employer to an employee in a given fiscal year. It also has the details of the income tax that has been deducted from the salary of the individual in question. Suppose the income from your salary for a financial year is more than the basic exemption limit of Rs. 2,50 000; then your employer is required to deduct TDS from your salary and deposit it with the government. Those who have worked with more than one employer at the same time or have changed jobs in a financial year will receive Form 16 from all the employers. It must be noted that it is not issued to an employee whose income for a particular year is below the threshold of tax exemption with no provision for TDS. Significance of Form 16 The information contained in this form comes in handy for filing ITR. It helps taxpayers to prepare their ITR easily without seeking the help of any financial planner or CA. The said certificate helps to verify the deposited tax amount by comparing the same with Form 26AS. It serves as proof of TDS. Form 16 also serves as proof of income. It is an important document that is used in the verification process while availing of a loan. Several organisations require individuals to submit Form 16 issued by their previous employers as a part of the onboarding process. It also serves as a visa checklist and comes in handy while planning a foreign trip. How to Download Form 16 From TRACES Firstly, go to the TRACES portal. Log in to the portal with your login ID and password. Hover over to the downloads tab, where you can find Form 16A. Once you have opened the Form, fill in all the required details. FAQs What is the use of Form 16? Form 16 is a certificate denoting salary income and the TDS amount breakup. It is useful for verifying the TDS that was deducted by the employer from the employee’s salary and finally submitted to the income tax department. Form 16 is a certificate that is issued by an employer. It consists of a salary breakup, which is required to file the ITR. What is the difference between Form 16 and ITR?