Brief History of de-linking of Credit / Debit Notes with Tax Invoice

The flow of activity in the matter

- Originally, from 1st July 2017, the provisions of section 34 of the Central Goods and Services Tax mandates the registered person to issue two or more number of a credit note or debit note in respect of multiple tax invoice issued/ raised in a Financial Year.

- To overcome the hurdle, in 28th GST council meeting, held on 21st July 2018, it was proposed to permit the registered person to consolidate the credit note/ debit note in respect of multiple invoices issued in a Financial Year.

- Accordingly, provisions of section 34 sub-section (1) and sub-section (3) of the Central Goods and Services Tax Act, 2017 was amended (vide the Central Goods and Services Tax (Amendment) Act, 2018) and made effective from 1st February 2019.

- Interestingly, even though the amendment was made effective from 1st February 2019, the corresponding changes were not incorporated in GSTN portal. After a long break of more than one and a half year, finally, on 14th September 2020, the delinking facility is incorporated in the GSTN portal.

Prior and amended provisions of section 34 of the Central Goods and Services Tax Act

Provisions of section 34(1) deal with the credit notes, whereas, provisions of section 34(3) deals with the debit notes.

Prior provisions of section 34, mandates the registered person to provide one to one correlation between the credit or debit notes issued against the tax invoice. However, post amendment, the registered person was allowed to consolidate the credit or debit notes for supplies made in a financial year.

Analyzing delinking facility in GSTN portal

the delinking is made available in the GSTN portal only from 14th September 2020. The details of credit notes and debit notes as covered in Table-9B, of Form GSTR-1, before and after delinking facility is explained hereunder.

Details in Table-9B of Form GSTR-1 before delinking facility incorporated in GSTN portal-

- Receiver GSTIN/ UIN.

- Receiver Name.

- Debit/ Credit Note No.

- Debit/ Credit Note Date.

- Original Invoice Number.

- Original Invoice Date.

- Note Type.

- Note Value.

- Supply Type.

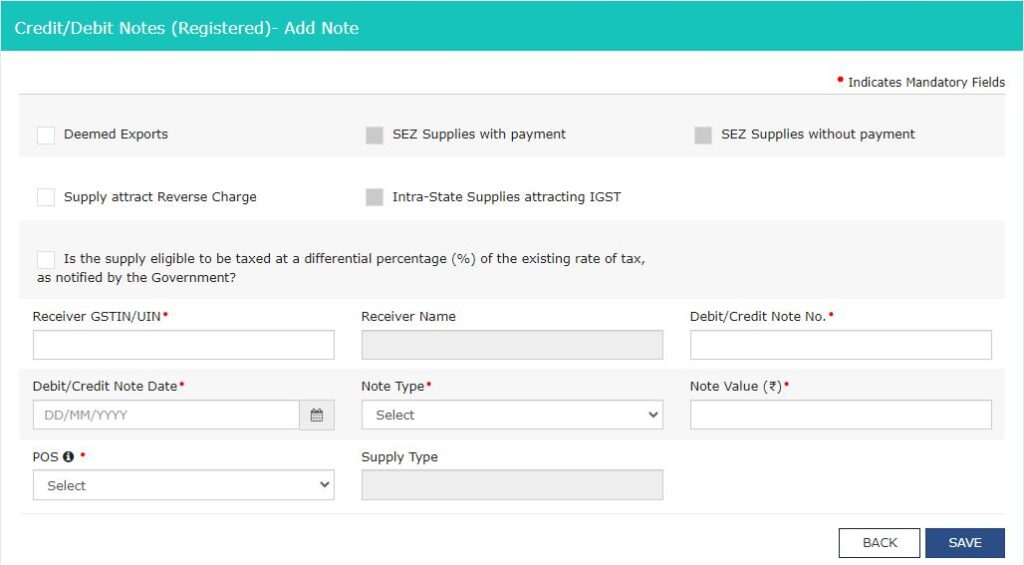

Details in Table-9B of Form GSTR-1 after delinking facility incorporated in GSTN portal-

- Select the appropriate option.

- Receiver GSTIN/ UIN.

- Receiver Name.

- Debit/ Credit Note No.

- Debit/ Credit Note Date.

- Note Type.

- Note Value.

- POS

- Supply Type.

In nut-shell, before incorporation of delinking facility in GSTN portal, the registered person was required to mention ‘Original Invoice Number and Original Invoice Date’. However, only after incorporation of the delinking facility (i.e. from 14th September 2020), the consolidation of credit note and debit note gets possible.

Critical Issues Involved related to Input tax Credit

FAQs

What does it mean to delink credit notes and debit notes from the original invoice?

Delinking credit notes and debit notes from the original invoice means that these documents can be issued independently without referring to the specific original invoice they relate to. This simplifies the process of issuing and managing these notes.

Why has the GST Council decided to delink credit and debit notes from the original invoice?

The GST Council decided to delink these notes to reduce compliance burdens on businesses. This change simplifies the process of adjusting tax liabilities and ensures smoother handling of returns.