Form 16B basically is an indicator of the amount of money that has been deducted as property Tax Deducted at Source (TDS). The buyer, in this case, is required to basically minus the TDS on property at the time of the property sale.

Form 16B which is a TDS certificate reflects the amount that has been deducted as TDS on property that has been deposited by the buyer with the Income Tax Department. Buyer is required to deduct TDS on property at the time of sale of the immovable property. The TDS is deducted at 1% from the amount that the buyer has to pay the seller. That amount is then to be deposited with the Income Tax Department.

After the amount has been deposited with the Income Tax Department the buyer will have to issue Form 16B to the seller. This is a proof of the TDS being deducted on the property and that it is deposited with the government. Form 16 is TDS certificate for the TDS deducted from salary, Form 16A is TDS certificate for the TDS deducted from all other types of payments, Form 16B is TDS certificate for the TDS being deducted on the sale of property.

Every person who has income chargeable to tax is required to file an income tax return to report their income and tax liabilities. However, income tax laws in India provide for the collection/deduction of tax at source (TDS/TCS). This, on the one hand, ensures, continuous revenue flow to Government and on the other hand, keeps a check on tax evasion.

It is the responsibility of the payer to deduct tax (TDS/TCS) and pay it to the credit of Government. For such tax deduction, obtaining a Tax deduction Account Number (TAN) is mandatory. Deductor also has the responsibility of filing Tax deduction at source (TDS) return providing particulars of deductees, nature of the payment made, tax deducted, rate at which it is deducted etc for every quarter of a financial year. The TDS returns filed facilitate the income tax department give credit of TDS to the right deductees.

Nature of Tax Deduction and Person Responsible to Deduct Tax

- here is a transfer (other than cases of compulsory acquisition) of immovable property

- Immovable property means land/building/part of building but excluding agricultural land*

- Buyer is responsible for paying consideration to resident seller in respect of such transfer

- Transfer is for a consideration of Rs 50 lakhs or more

- Buyer must deduct tax at the rate of 1% of consideration either at the time of credit or payment

- If seller does not provide for PAN, TDS at the rate of 20% as per Section 206AA

Contents of Form 16B

- Deductors and Deductee name and address

- Deductors and Deductee PAN number

- Assessment year

- Payment acknowledgement number

- Amount paid/credited

- Verification

Form 26QB and Form 16B

Form 26QB is a return cum challan for payment of TDS to the Government which shall be furnished electronically for tax deducted under Section 194-IA.

Due date

Form 26QB shall be furnished within 30 days from the end of the month in which deduction is made. For eg: if payment/credit is made on 16th April, Form 26QB shall be furnished by 30th May.

Installments

In case of payment/credit in installments, as TDS is required for each installment, Form 26QB shall also be furnished for each such deduction.

Multiple parties to transaction

Form 26QB shall be furnished for each buyer and seller combination.

Example 1: If there one buyer, B1 and 2 sellers, S1 and S2, Form 26QB shall be furnished separately for B1 and S1 combination and B1 and S2 combination, hence overall 2 26QB to be filed.

Due Date for Issuance of Form 16B

Deductor shall issue Form 16B to the payee within 15 days from the due date for furnishing Form 26QB and Form 16B can be generated and downloaded from TRACES – TDS Reconciliation and Analysis and Correction Enabling System. For eg: Using the same example as above w.r.t due date for Form 26QB, Form 16B shall be issued on 14th June.

Depositing TDS amount

Once the challan is printed, the tax amount is deposited as a cheque or demand draft. When the taxpayer opts to pay at a bank, he/she will be redirected to the bank’s official payment page. Once the amount is paid, a challan counterfoil with CIN, payment details, bank’s name, etc. is displayed. This counterfoil acts as proof of payment. After this, taxpayers can proceed to the TRACES portal after 5 days and download Form 16B.

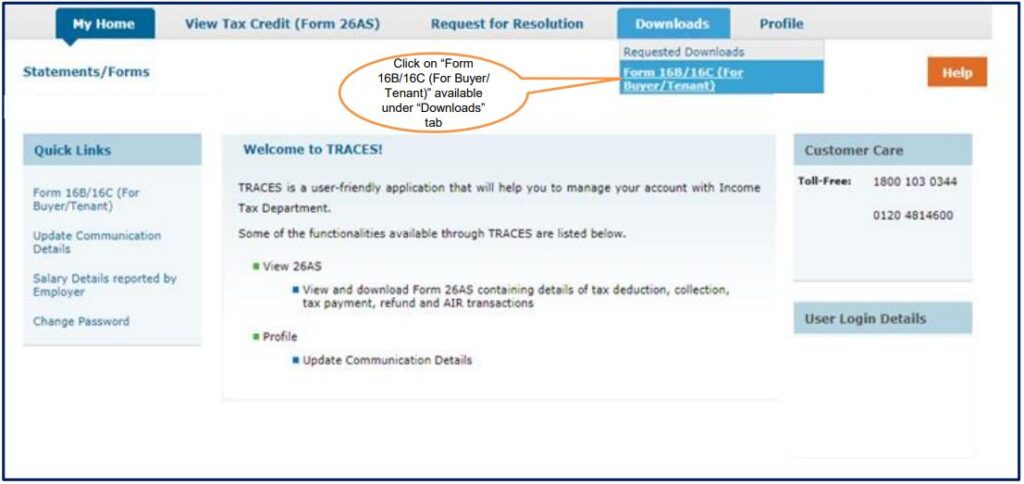

Procedure to Generate and Download Form16B from TRACES

- Register as taxpayer on TRACES with details of PAN and either detail of tax deducted or details of challan or details of Form 26QB. Also, enter the verification code and click on ‘Proceed’. Activation link will be sent to email id through which account can be successfully created

- If already registered login to TRACES with username as ‘PAN’ and password

- Under downloads tab Select ‘Form 16B (For Buyer)’

- Furnish details such as assessment year, acknowledgment no. of the Form 26QB and PAN of the seller

- Form 16B will now be available on requested downloads section under Downloads category

- Form 16B can now be printed/saved

Difference Between Form 16, Form 16A, and Form 16B

Particulars | Form 16 | Form 16A | Form 16B |

Who issues it? | Issued by the employer | Issued by financial institutions, tenants, etc. | Issued by property buyers to sellers. |

Who is it directed at? | Directed towards salaried employees. | Directed towards non-salaried employees. | Directed towards property sellers. |

Purpose | Form 16 is issued for TDS on salary. | Form 16A is issued on income generated through non-salary sources such as securities, returns on investment, rent, or interest on FD. | Form 16B is issued for TDS on earnings generated through the sale of immovable property. |

Components |

|

|

|

Section under IT Act | Section 203 of the Income Tax Act. | Section 203 of the Income Tax Act. | Section 194 of the Income Tax Act. |

FAQs

What is Form 16B?

Form 16B is a TDS (Tax Deducted at Source) certificate issued by the buyer of property to the seller. It is used to certify that TDS has been deducted on the sale of immovable property under Section 194-IA of the Income Tax Act. This form provides details of the transaction, including the amount of TDS deducted and deposited with the government.

When is Form 16B issued?

Form 16B is issued by the buyer of the property to the seller after the TDS on the property transaction has been deposited with the government. It must be issued within a specified time frame as per the Income Tax regulations.