GST brings transparency and develops mutual trust between the Revenue and the taxpayers. Most of the compliance process- return filing, registration, and sometimes even proceedings intend to happen without meeting a tax officer in person! Let us now focus on one of GST’s new tools to achieve its objective-an Invoice Reference Number(IRN).

Form INV-01 holds a place of significance in the Indian GST regime, thanks to the provision of Invoice Reference Number (IRN). Invoice Reference Number (IRN) is an alternative to the conventional system of invoicing wherein an original invoice is maintained by the buyer, a duplicate is issued to the transporter, and triplicate to the seller. The option digitizes the revenue process at the check posts, reduces the waiting time for the transporter at revenue check posts and enables tax authorities to track the goods being transported without referring to the duplicate copy. As the nature of the invoice isn’t physical, it takes away the risk of loss. IRN could be generated from the eway bill portal by uploading an invoice (Form GST INV-01). The number so generated would be valid for a period of 30 days, within which it can be used in place of a physical tax invoice. This article particularly centres around Form GST INV-01 and its particulars.

How does IRN help?

Under normal circumstances, three sets of invoices are issued as follows:

- Original for the buyer

- Duplicate for the transporter

- Triplicate for the seller

Instead of the above paperwork, a transporter may opt for IRN as it digitizes the revenue process at the check posts. It reduces the waiting time for the transporter at the revenue check post and helps taxing authorities keep track of the goods being transported. There is no risk of losing an invoice if an IRN is generated.

Format Explained

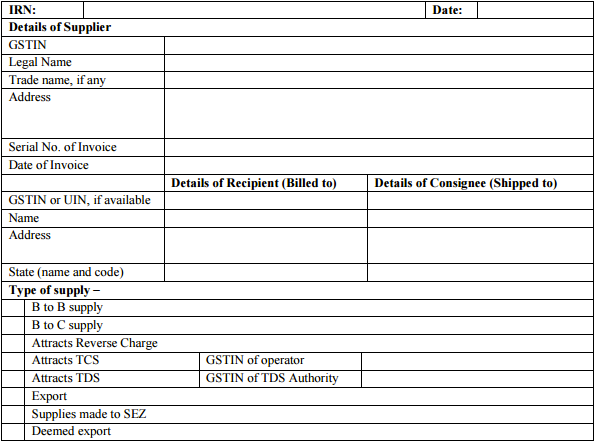

As already observed, GST INV-01 must be uploaded into the portal so as to generate the IRN. The form comprises of four parts with different particulars to be filed in each of them. Such particulars are covered here for the awareness of the readers:

Part A

The form begins by asking taxpayers/suppliers to fill in their basic details, which includes:

- GSTIN and the name of the supplier (auto-populated).

- The address of the registered/principal place of business.

- Serial number and the date of invoice.

Form GST INV 1 – Part A

Part B

This part of the form pertains to the details of the recipient, which includes:

- GSTIN (for registered taxpayers).

- UIN (if the recipient is an embassy or UN organization).

- The name of the recipient and consignee.

- The address and state code (first two digits of the GSTIN) of the consignee.

For the awareness of the taxpayers, the details of the consignee and recipient could be similar if the parties being billed to and the parties to whom the goods are being delivered are identical. In certain cases, though, the GSTIN of both the recipient and consignee can be the same but with different addresses. And in other instances, the GSTIN of the party to whom the bill is addressed to would differ from the one to whom it is shipped.

Form GST INV Part B

Part C

Part C of the Form deals with particulars concerning the type of supply made by the taxpayer, including the type of transaction and applicability for tax provisions.

Form GST INV 1 – Part 3

Part D

The final part of the form prompts for information pertaining to the consignment of goods billed, which includes:

- The description of goods.

- The HSN code.

- The quantity and unit price, which helps in determining the taxable GST amount.

- The applicable tax rate and amount, which will be calculated based on the type of transaction (inter-state or intra-state).

- The declaration of freight, invoice and packaging and forwarding charges as stated in the tax invoice.

FAQ

Items on which ITC is not allowed?

The input tax credit is not available for claims in the following cases-

- Motor vehicles, with a seating capacity of less than or equal to 13 persons (including the driver), goods transport agencies, vessels and aircraft, except for a few cases. So as an exception, ITC is allowed in the below cases:

- Such motor vehicles and conveyances are further supplied i.e. sold.

- Transport of passengers and goods.

- Conveyance is used for imparting training on driving, flying, and navigating such vehicles or conveyances.

- Services of general insurance, servicing, repair and maintenance relating to motor vehicles, vessels or aircraft in Sl. no.1.

- Food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery.

But if the goods and/or services are taken to deliver the same category of services or as a part of a composite supply, the input tax credit will be available

Example: Mr Dev purchases cosmetic creams to supply it to a customer, then ITC on purchases will be allowed. - Membership in a club, health, and fitness centre.

- Rent-a-cab, health insurance and life insurance except in the following cases where it is allowed:

- Government makes it obligatory for employers to provide it to their employees by law.

For example, the mandatory cab services for female staff in night shifts. - Goods and/or services are taken to deliver the same category of services or as a part of a composite supply, input tax credit will be available.

For example, if Mr Dev takes the service of rent-a-cab to supply to Mr Manoj, a customer, then the ITC on purchases will be allowed. - Leasing, renting or hiring motor vehicles, vessels or aircraft, except cases in Sl.no. 1.

- Government makes it obligatory for employers to provide it to their employees by law.

- Travel benefits are extended to employees on vacation such as leave or home travel concessions.

- Works contract service for construction of an immovable property (except plant & machinery or for providing a further supply of works contract service).

- Goods and/or services for the construction of an immovable property whether to be used for personal or business use.

- Goods and/or services where tax has been paid under the composition scheme.

- Goods and/or services used for personal use.

- Goods or services or both are received by a non-resident taxable person except for any of the goods imported by him.

- Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples.

- ITC will not be available in the case of any tax paid due to non-payment or short tax payment, excessive refund or ITC utilised or availed by the reason of fraud or willful misstatements or suppression of facts or confiscation and seizure of goods.

- Special cases: Standalone restaurants will charge only 5% GST but cannot enjoy any ITC on the inputs.

- The expenditure spent on Corporate Social Responsibility (CSR) initiatives by corporates

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | GST Search Taxpayer | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | aaple sarkar portal | epf activation | scrap business | brsr | depreciation on computer | west bengal land registration | traces portal | Directorate general of GST Intelligence | form 16 | rtps | patta chitta