A delivery challan is a significant document that is useful when a business transports its goods from one place to another. It keeps a detailed record of the items delivered, ensuring that both the sender and receiver have a clear understanding of the transaction.

Meaning of delivery challan

A delivery challan is a document that contains details of the products in that particular shipment. It is issued at the time of delivery of goods that may or may not result in a sale.

When Delivery Challan is Issued?

A GST tax invoice is issued usually when the supply of goods or services is made or when payment has been made by the recipient. For services, the tax invoice must normally be issued within 30 days of delivery of service mandatorily. In some cases, instead of a tax invoice, a delivery challan is issued for transportation of goods. The following are instances when delivery challan can be issued for the transportation of goods without an invoice:

- Supply of liquid gas where the quantity at the time of removal from the place of business of the supplier is not known.

- Transportation of goods for job work.

- Transportation of goods for reasons other than by way of supply.

- Other supplies as notified by the Board.

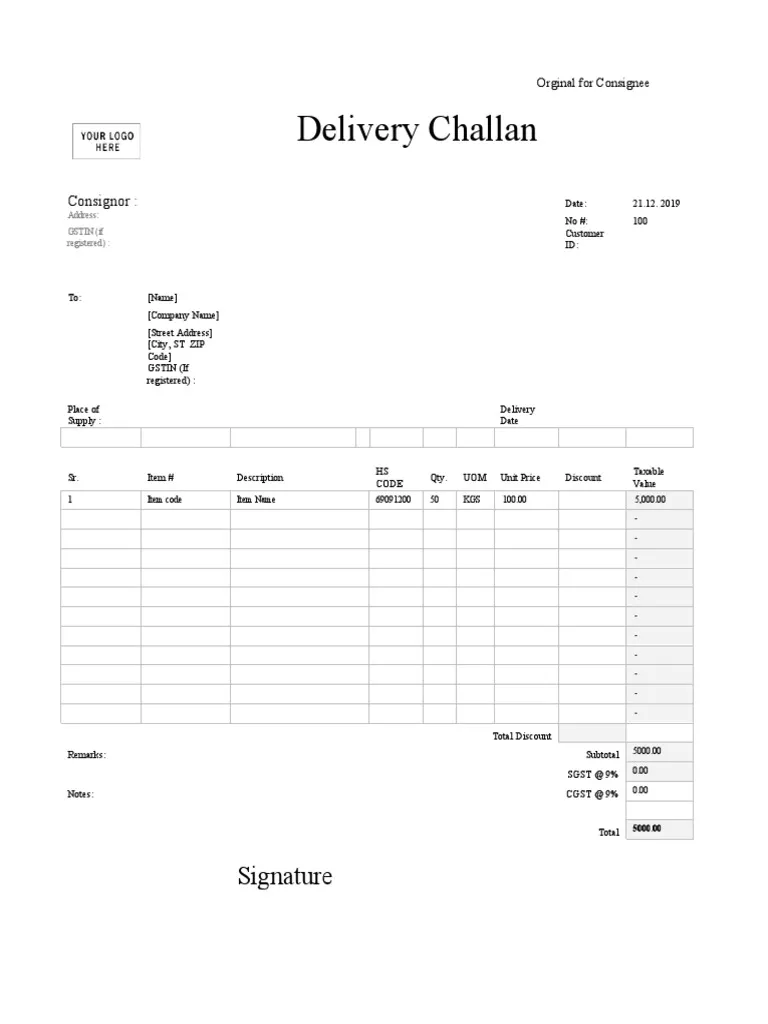

Delivery Challan Format

Delivery challans must be serially numbered not exceeding sixteen characters, in one or multiple series. The format of the delivery challan should contain the following information:

- Date and number.

- Name, address and GSTIN of the consigner, if registered.

- Name, address and GSTIN or Unique Identity Number of the consignee, if registered. If unregistered, name, address and place of supply.

- HSN code for the goods.

- Description of goods.

- Quantity of goods supplied (provisional, if unable to determine the supply of the exact quantity).

- Taxable value of supply.

- GST tax rate and tax amount broken down as CGST, SGST, IGST and GST Cess – where the transportation is for supply to the consignee.

- Place of supply, in case of inter-state movement of goods.

- Signature.

Important GST rules on delivery challan

A tax invoice must be issued in a case where a registered taxpayer intends to transport goods from one place of supply to another as per the provisions of Section 31 of the CGST Act. Particulars regarding the invoice value, description of the goods supplied, their quantities, rates and amount and the GST applicable on them will form part of the tax invoice.

Certain cases arise where the transportation does not result in a sale, and hence there is no tax invoice issued. In these cases, instead of a tax invoice, a delivery challan is issued. Therefore, a delivery challan is a document that permits the transportation of goods from one place to another. It also goes by the name dispatch slip or delivery slip.

Rule 55 (2) of the CGST Rules, delivery challans must be issued in three copies as follows-

- For the buyer to be marked as “Original”

- For the transporter to be marked as “Duplicate”

- For the seller to be marked as “Triplicate”

FAQs

Differences between tax invoice and delivery challan?

| Tax Invoice | Delivery Challan |

|---|---|

| Contains ownership proof and legal responsibilities. | Does not contain proof of ownership or legal responsibilities. |

| Shows the actual value of goods. | Shows that the customer has acknowledged receipt of the goods. |

| It is proof that a sale transaction has taken place. | May or may not result in a sale. |

| Depicts the actual value of the goods, including the applicable taxes. | Displays the rate of a particular product but not the full value of the sale. |

What is the difference between a delivery note and a delivery challan?

A delivery note is a mere document that accompanies a shipment of goods. Delivery challans, on the other hand, are issued while making a delivery of goods to the buyer and have an impact on the inventory levels since it decreases the inventory stock.