GST invoice is a bill or receipt of items sent or services that a seller or service provider offers to a customer. It specifically lists out the services/products, along with the total amount due. One can check a GST invoice to determine said product or service prices before CGST and SGST are levied on them.

A GST invoice bill also displays the amount of taxes charged on each product or service, that an individual purchases from the seller or provider

Invoicing is a crucial activity for any business, irrespective of type and size. Businesses should be careful while generating invoices as every transaction enters into books of accounts through this activity. Further, after introducing the Goods and Services Tax (GST), registered businesses must issue GST invoices, also known as GST bills.

What is a GST invoice?

An invoice or a GST bill is a list of goods sent or services provided, along with the amount due for payment.

Prescribed GST Bill Formats

As per Section 2(66) of the Central Goods and Services Tax Act of 2017, to understand the exact format of a tax invoice, one must refer to Section 31. Even though Section 31 outlines a general guideline for GST invoice formats, it does not go into specifics.

However, Section 31 does state the requirements or entries that such an invoice must carry to qualify as an official GST document. Moreover, such an invoice can be electronic, as well as manual.

Who should issue GST Invoice?

If you are a GST registered business, you need to provide GST compliant invoices for sale of good and/or services.

Also, you should receive GST invoices from your vendors to claim the Input Tax credit (ITC).

What should a GST Invoice Bill Include?

The following pointers are mandatory inclusions in such a bill –

- This invoice should be issued by an input distributor.

- All supplementary bills/invoices.

- Any revisions to the invoice generated by the supplier in the past.

Apart from these sections, a GST tax invoice must include the following particulars as well –

- GSTIN, name, and address of the supplier issuing a GST invoice.

- Date of issuance.

- A unique serial number not exceeding 16 digits.

- In the case of registered recipients, this bill should also include the name, GSTIN, and address of the receiving party as well.

- A complete description of all services or goods provided, complete with HSN code.

- Amount of discount applicable on these taxes, if any.

- Tax amount.

- Invoice valuation.

- The rate at which CGST, SGST, and IGST are charged should be mentioned on this bill.

- The billing address and information.

- Shipping address and information.

- Reverse charge or forward charge.

- Signature of the tax invoice issuer or authorized representative.

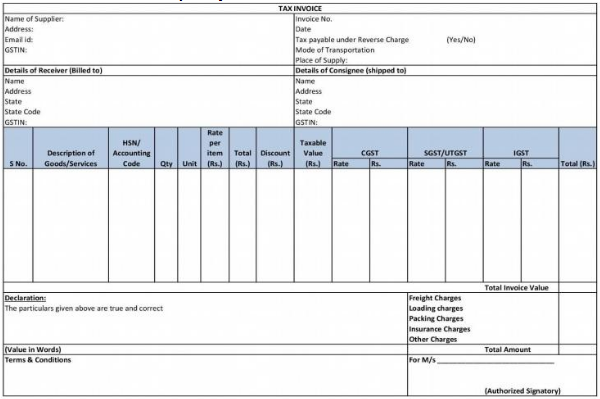

The table below is indicative of how a GST invoice bill generally looks. One should understand that the layout of such receipts differs from one supplier or seller to the next. Nevertheless, the information and details should match the one presented in the following table –

| Tax Invoice | Date: | ||||||||

| Company Name: GSTIN: | Address: | ||||||||

| Billing Address: | Shipping Address: | ||||||||

| Serial No. | Item Desc. | HSN | Qty. | Per Item Rate | Total | Discount | Taxable Amt | CGST(9%) | SGST (9%) |

| 1. | X | 5 | Rs.40 | Rs.200 | – | Rs.200 | Rs.18 | Rs.18 | |

| 2. | Y | 7 | Rs.25 | Rs.175 | – | Rs.175 | Rs.15.75 | Rs.15.75 | |

| Total | Rs.375 | Rs.375 | Rs.33.75 | Rs.33.75 | |||||

| Tax Invoice Value (In figures) | Rs.442.50 | ||||||||

| Tax Amount Subject to Reverse Charges | |||||||||

Issuing a GST Invoice: When should it be done?

Generating a GST invoice as soon as items are shipped or services rendered can be difficult in certain cases. Thus, to ease matters, the Indian Government has outlined a general time limit for suppliers to follow.

- On Goods (Normal)

Goods suppliers need to draw up such an invoice on or before the date of removal of said products. Under Section 2 (96) of CGST Act, 2017 removal of goods can mean one of two things –

- Goods dispatched for delivery to the recipient.

- Goods collected from the supplier by the recipient or an authorised person acting on behalf of the recipient.

- On Goods (Continuous Supply)

If the invoice concerns a recipient with whom the supplier maintains a constant order of business, then the latter can issue an invoice under GST on or before the account statement is generated or payment received.

- On Services

In the case of a GST invoice bill on services rendered, one needs to issue the same within 30 days of providing the services in question.

- On Bank and NBFC Services

In the event of financial services provided by banks and other financial institutions, the deadline for issuing a GST receipt is not within 30 days unlike all other services, but 45 days from the date of service supply.

FAQs

How many copies of invoices should be issued?

- For goods – 3 copies

- For services – 2 copies

Copies of Invoices for Goods Supply

In the event of raising a GST invoice for goods supply, the issuer would need to arrange three copies for the following members involved in such transactions –

- The original copy is for the recipient.

- The duplicate copy is for the use of individuals responsible for transporting said goods from supplier to recipient.

- The triplicate copy is useful to the supplier.

Copies of Invoices for Services Supply

Since there are no transporters involved in a supply of service, issuers need to only draw two copies of the GST invoice bill.

- The original document belongs to the service recipient.

- The duplicate is kept by the supplier for internal use.

What are the mandatory fields a GST Invoice should have?

A tax invoice is generally issued to charge the tax and pass on the ITC. A GST Invoice must have the following mandatory fields-

- Invoice number

- Invoice date

- Customer name

- Shipping and billing address

- Customer and taxpayer’s GSTIN (if registered)**

- Place of supply

- HSN code/ SAC code

- Item details i.e. description, quantity (number), unit (meter, kg etc.)

- Total value

- Taxable value and discounts

- GST rate and amount of taxes i.e. CGST/ SGST/ IGST

- Whether GST is payable on reverse charge basis

- Signature of the supplier

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | GST Search Taxpayer | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | aaple sarkar portal | epf activation | scrap business | brsr | depreciation on computer | west bengal land registration | traces portal | Directorate general of GST Intelligence | form 16 | rtps | patta chitta