The Goods and Services Tax has eased the process of indirect taxation considerably since its introduction in India in 2017. However, despite the relative simplification in regards to the previous tax regime, it’s still in the nascent stages. Hence, there is still some degree of blurriness concerning its functioning among the business community in India.

GSTR-2A is a purchase-related tax return automatically generated for every business registered under the Goods and Services Tax (GST). It is a statement that captures details of all your purchases for a particular month. GSTR-2A is an automatic return generated for a taxpayer from the seller’s/counterparty’s GSTR-1, GSTR-5, GSTR-6, GSTR-7, and GSTR-8.

What is GSTR 2A?

GSTR 2A means a purchase-related document that the GST portal provides to each business registered with it. The GSTR 2A has generated automatically when a business’s seller or counterparty uploads the GSTR 1 and 5 Forms. It details the purchases a company makes in a particular month, thereby noting all invoice details.

However, it is a read-only document, serving only to inform a business of its sellers’ invoice details. The concerned enterprise should verify this GST form 2A and rectify any discrepancy in it before filing their returns on the GST portal as GSTR 2.

How is GSTR 2A generated?

The GST portal auto-populates GSTR 2A standing on information available from a business’s sellers or counterparties’ returns per the following forms –

- GSTR 1

- GSTR 5

- GSTR 6

- GSTR 7

- GSTR 8

It’s generated in these cases mentioned below –

- When a seller (registered resident) uploads transaction details in the GSTR 1 Form.

- When a seller (non-resident) uploads transaction details in the GSTR 5 Form.

- When the Input Service Distributor submits the GSTR 6 Form.

- When a counterparty files the GSTR 7 & 8 Forms, noting the TDS and TCS details

Verification of GSTR 2A is necessary to file the GSTR 2 Form. However, in some cases, the seller might defer their filing of GSTR 1. In that case, the concerned business will need to populate the necessary details when filing their GST returns manually.

And to ensure consistency in information recording, the details submitted by a seller in GSTR 1 will reflect in such business’s GSTR 2A in the next month.

For instance, suppose one is filing their GST returns in August, and their seller uploads GSTR 1 of August in September. Thence, such businesses will need to fill in relevant information manually in GSTR 2 of August. And, such details as submitted by the seller will show in the GSTR 2A of September.

Difference between GSTR-2A and GSTR-2B

Parameters for Comparison | GSTR-2A | GSTR-2B |

| Purpose of Statement | An auto-drafted statement that provides Input Tax Credit (ITC) details to every recipient of supplies, based on the suppliers’ data including changes done later on. | A constant auto-drafted statement that provides ITC details to every recipient of supplies, based on the suppliers’ data for every tax period. |

| Nature of the statement | Dynamic, as it changes from day to day, as and when a supplier reports the documents. | Static, as the GSTR-2B for one month, cannot change based on actions of the supplier taken later on. |

| Frequency of availability | Monthly | Monthly |

| Source of information | GSTR-1 or IFF*, GSTR-5, GSTR-6, GSTR-7, GSTR-8, ICES | GSTR-1 or IFF*, GSTR-5, GSTR-6, ICES |

| Advisory on ITC claims | Does not consist of information/advisory on the action a registered buyer needs to take | Consist of an advisory against each section on whether the ITC is eligible, ineligible or reversal, for the taxpayer to take action accordingly in his GSTR-3B |

| When will ITC entries get transferred from sources? | GSTR-1: Saved, filed, or submitted GSTR-6: Submitted GSTR-7 and GSTR-8: Filed | GSTR-1, GSTR-5, or GSTR-6: Filed |

| Cut-off date for entries, to view the statement for a tax period | Not applicable, as it’s a dynamic statement | 11th or 13th of the next month (depending on the return filing frequency) The statement will be generated on the 14th of the succeeding month |

| Maximum ITC entries that can be viewed on GST portal without excel download | Total of 500 rows | Total of 1,000 rows |

What happens if the seller delays GSTR-1 or fails to upload invoices?

The ITC pertaining to those invoices not uploaded or delayed will not appear in GSTR-2A of the relevant tax period. The buyer may have to bring this to the notice of his defaulting suppliers or vendors to upload the missing invoices on time. From August 2020, every buyer must refer to GSTR-2B instead of GSTR-2A to know the ITC available to him for a tax period.

Nonetheless, until 31st December 2021, the buyer could have claimed an input tax credit on a provisional basis in his GSTR-3B to the extent of 5% of eligible tax credit appearing in GSTR-2B towards the invoices not found in GSTR-3B under the CGST Rule 36(4).

However, from 1st January 2022 onwards, it is not possible to claim such 5% provisional or additional ITC due to the amendment made to CGST rule 36(4). A buyer can only claim ITC appearing in GSTR-2B by virtue of Section 16(2)(aa) of the CGST Act.

How to File GSTR 2A?

Since it is a read-only document that’s auto-populated based on other forms, a business does not need to file it. However, businesses need to accept it, reject it, modify it, or defer its acceptance if such an organisation finds any discrepancy in the invoice details that its seller submitted in GSTR 1.

Also, since it’s generated automatically, there’s no GSTR 2A due date in question. Nevertheless, if any information in that form requires modification, businesses shall do so in GSTR 2. And the due date for that is between the 11th and 15th of a month immediately following the month for which such GST return is filed.

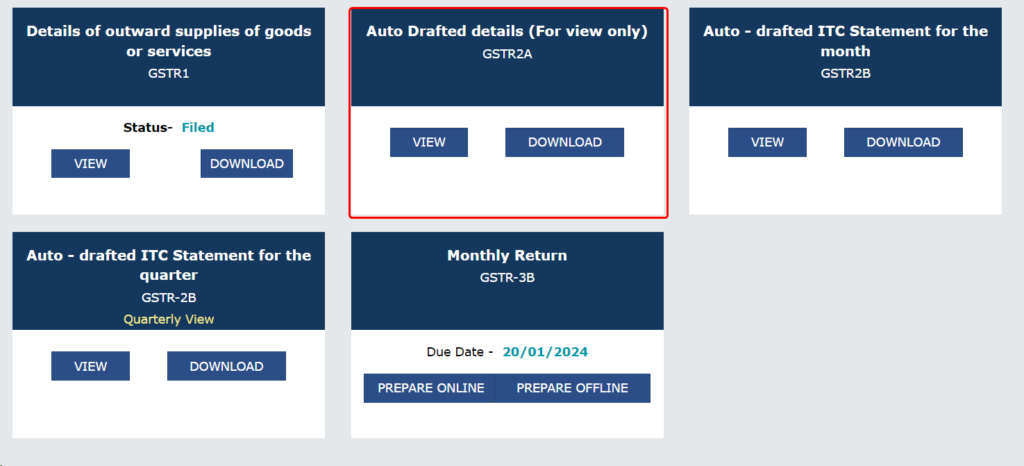

How to View GSTR 2A?

Step 1: Visit the official GST portal.

Step 2: Log in with the necessary credentials.

Step 3: Click on “Services” on the dashboard.

Step 4: Click on “Returns” and then “Returns Dashboard”.

Step 5: It will show the “File Returns” page, where one needs to fill the “Financial Year” and “Return Filing Period” and then click on Search.

Step 6: Following that, one needs to click on the “View” option under GSTR 2A.

Step 7: It will then show the GSTR 2A – Auto-drafted details page.

What are the Details Featured in GSTR 2A?

GSTR 2A format seven headings, as per the government’s mandate. These are –

- GSTIN – The 15-digit GSTIN of such business

- Name of the Taxpayer – The registered person’s legal name and trade name (if any)

PART A

- Invoice details of inward supplies that a business received from a registered person, except supplies that attract a reverse charge. It is presented in the following format.

| GSTIN of Supplier | Invoice details | Rate | Taxable Value | Amount of Tax | Place of Supply (Name of State/UT) | |||||

| Number | Date | Value | Integrated tax | Central tax | State/UT tax | Cess | ||||

- Inward supplies on which the reverse charge attracts tax. It’s presented in a similar format as 3.

- All Debit/Credit notes and any modification received thereof in the current period. It’s illustrated in the following format.

| Details of original document | Revised details of document or details of original Debit/Credit note | Rate | Taxable Value | Amount of tax | Place of Supply (Name of State/UT) | ||||||||

| GSTIN | No. | Date | GSTIN | No. | Date | Value | Integrated tax | Central tax | State/UT tax | Cess | |||

Part B

- IDS credit received (including amendments thereof) – It is applicable for Input Service Distributors and their branches. This title shows the credit of ISD and any modification in the current tax period.

Part C

- TDS and TCS credit received (including amendments thereof) – it is applicable for businesses involved in TDS transactions or selling online via an e-commerce platform.

How to Download the Form?

A taxpayer needs to download the GSTR – 2A if the number of invoices is more than 500. You must have the GST offline tool installed in the system in order to use this file. Here are the steps to do so:

Step 1: Click on download on the GSTR – 2A block.

Step 2: Click on the ‘Generate JSON file to download’ button in order to generate data in the JSON or excel format. The generated JSON file needs to be opened in Returns Offline Tool, available on the GST portal.

Step 3: Click on the link that says – “Click here to download JSON-File1” once it appears

FAQs

Matching GSTR-3B and GSTR-2A or GSTR-2B?

When the supplier files GSTR-1 in any particular month disclosing his sales, the corresponding details are captured in GSTR-2A and GSTR-2B of the recipient. GSTR-3B is a summary return. Hence, the amount of ITC available as disclosed in Table 4(a) must match with tax details disclosed in GSTR-2A or GSTR-2B. It is important to reconcile GSTR-3B and GSTR-2A or GSTR-2B on account of the following reasons:

- GST authorities have issued notices to a large number of taxpayers asking them to reconcile the ITC claimed in a self-declared summary return Form GSTR-3B and auto-generated Form GSTR-2A or GSTR-2B. Such notices are issued in GST ASMT-10. The taxpayer would be required to reply to such notices or pay the differential amount.

- Action has also been taken against evaders claiming ITC on the basis of fake invoices.

- Reconciliation ensures that credit is being claimed only in respect of the tax which has been actually paid to the supplier.

- Ensures that no invoices have been missed/ recorded more than once etc.

- In case the supplier has not recorded the outward supplies in GSTR-1, communication can be sent out to the supplier to ensure that the discrepancies are corrected.

- Errors committed while reporting details in GSTR-1 by suppliers or GSTR-3B by recipients can be rectified.

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | GST Search Taxpayer | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | aaple sarkar portal | epf activation | scrap business | brsr | depreciation on computer | west bengal land registration | traces portal | Directorate general of GST Intelligence | form 16 | rtps | patta chitta