GSTR-3B is the summary return that taxpayers must file regularly to show details of sales, ITC claims, tax liability, refunds, etc recorded on their GSTIN. The implementation of the GST regime has successfully eliminated the cascading taxation effect and has simplified the overall process. Since its introduction, several GST returns forms have been introduced catering to specific purposes. GSTR-3B is one of such vital return form.

What is GSTR 3B?

GSTR-3B is fundamentally a monthly self-declaration filed by a registered dealer in addition to GSTR 1 and GSTR 2 forms. It is a collected summary of inward and outward supplies that was introduced by the Government of India to provide relaxation to businesses that transitioned to the GST regime.

In other words, it is a simplified method that helps to declare the summary of GST liabilities for a given tax period. It must be noted that one cannot amend GSTR-3B and dealers must file separate GSTR-3B for each of their GSTIN. They must make it a point to pay the GSTR-3B’s tax liability by the last date of filing GSTR-3B for the same month.

All GST registrants must file GST return 3B including ‘NIL’ returns. Nonetheless, a few registrants do not need to file this self-declaration. They are –

- Suppliers of OIDAR

- Non-resident taxable individuals

- Input service distributors and composition dealers

- Small taxpayers

- Non-resident taxable individuals

Who should file GSTR 3B?

Every person who is registered under GST must file GSTR-3B.

- Taxpayers registered under the Composition Scheme

- Input service distributors

- Non-resident suppliers of OIDAR service

- Non-resident taxable persons

Late Fee & Penalty for GSTR-3B

A late fee is charged for filing GSTR-3B of a tax period after the due date. It is levied as follows:

- Rs. 50 per day of delay

- Rs. 20 per day of delay for taxpayers having nil tax liability for the month

In case the GST dues are not paid within the due date, interest at 18% per annum is payable on the amount of outstanding tax to be paid.

Due Dates for GSTR-3B Filing

GSTR-3B return is due on the 20th of each month.

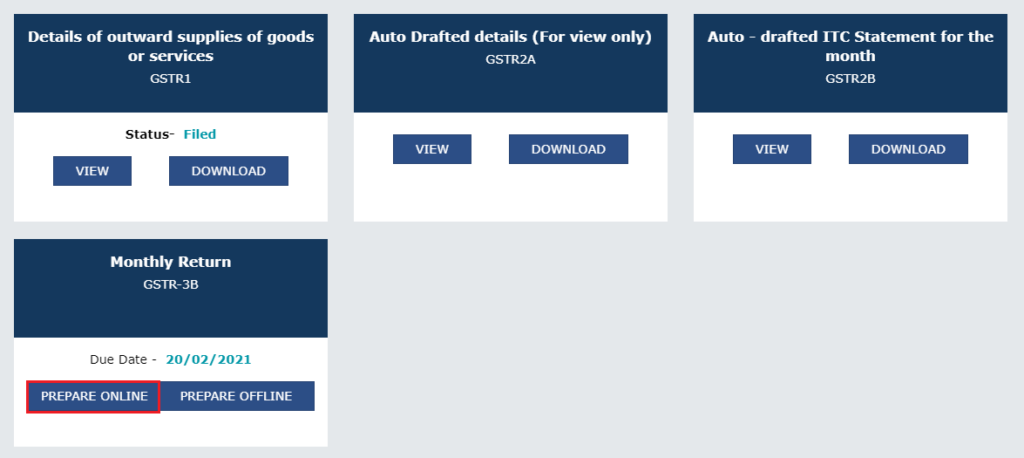

How to File Form GSTR-3B?

Step 1 – Login to GST’s official portal.

Step 2 – Navigate to the ‘Services’ tab.

Step 3 – Click on ‘Returns’.

Step 4 – Click on ‘Returns Dashboard’.

Step 5 – On being directed to the ‘File Returns’ page, select the ‘Financial year’ from the drop-down menu.

Step 6 – Select the applicable ‘Return Filing Period’ and click the ‘Search’ button.

Step 8 – Navigate to option marked GSTR 3B monthly returns.

Step 9 – Click on the button – ‘Prepare Online’ and enter the required details.

Step 10 – Click on the ‘NEXT’ button.

To file ‘NIL’ returns, individuals need to select ‘Yes’ in the very first question and continue with remaining ones.

Step 11 – Enter applicable values in displayed tiles. Fill in the interest and late fees if applicable.

To make required modifications in each tile, individuals can click on either the ‘ADD’ or ‘Delete’ option.

Step 12 – Click the ‘Confirm’ button once.

Step 13 – Click on the ‘SAVE GSTR 3-B’ button.

Step 14 – Click on the ‘SUBMIT’ button after verifying and confirming all the entered details. One can look up the status of this GSTR on the top right corner of the page.

Step 15 – To view the draft GSTR-3B return click on ‘Preview Draft GSTR-3B’.

Once the return is submitted successfully, the ‘Payment of Tax’ tile will be enabled. Taxpayers can click on the ‘Check Balance’ button to view the cash and credit balance.

Step 16 – From the drop-down, choose option ‘Authorised Signatory’.

Step 17 – Click on ‘FILE GSTR-3B WITH DSC/ FILE GSTR-3B WITH EVC’ option.

Step 18 – Click on the ‘Proceed’ button.

What are the Details Featured in GSTR 3B?

This form comprises 6 tables and requires taxpayers to provide specific information. This table focuses on the details featured in GSTR 3B –

| S.N. | Tables | Details contained |

| a) | Table – 1 | Inward supplies and outward supplies liable to reverse charge. |

| b) | Table – 2 | Interstate supplies directed towards unregistered individuals, UIN holders and composition dealers. |

| c) | Table – 3 | Input Tax Credit |

| d) | Table – 4 | Nil-rated, exempt and GST-free inward supply details. |

| e) | Table – 5 | Payment of tax |

| f) | Table – 6 | TCS/TDS credit |

What is the Relationship between GSTR 2A and GSTR 3B?

GSTR-3B and GSTR-2A must be reconciled. The reasons for it are given below in pointers –

- Through such reconciliation, room for claiming ITC based on fake invoices is eliminated.

- It gets rid of errors like recording an invoice more than once or missing its details entirely.

- One can quickly identify and rectify details provided in either GSTR-1 or GSTR-3B.

- In case outward supplies were not recorded in GSTR-1, it can be communicated to the concerned supplier to avoid discrepancy.

- Input Tax Credit reconciliation as per GSTR-3B and GSTR-2A is required to file an annual return in GSTR-9.

Nonetheless, there are cases of non-reconciliation of GSTR-3B and GSTR-2A. The same can be due to any of these following reasons –

- Input Tax Credit claim was for Integrated Goods and Services Tax on imported goods or services.

- Input Tax Credit claim was in the fiscal year in which goods or services were received.

- Transitional credit claim was under TRAN-I and II.

- ITC was availed on the paid GST amount on RCM basis.

The primary reason behind non-reconciliation is because a corresponding GSTR-1 was not filed or Input Tax Credit remains unclaimed in the meantime. Notably, if any discrepancy related to the claim of ITC is noticed in GSTR 2A and GSTR 3B taxpayers have to pay the wrongly claimed amount along with interest.

The best way to avoid discrepancy in these details of both GSTR-3B and GSTR-2A is to provide accurate information and eliminate all possible errors before submitting them.

FAQs

Should I provide invoice-wise details on the return?

Only consolidated numbers are required in GSTR-3B. Invoice-wise breakup is not required.

What is the difference between GSTR-1 & GSTR-3B?

You have to report all the sales detail in GSTR-1, whereas you have to report summarised figures of sales, ITC claimed, and net tax payable in GSTR-3B return.