GSTR 9C is an annual audit form for all the taxpayers having the turnover above 5 crores in a particular financial year. Along with the GSTR 9C audit form, the taxpayer will also have to fill up the reconciliation statement along with the certification of an audit.

Pre-requisites to prepare and file GSTR-9C

- The taxpayer must have a valid GSTIN and must be registered under GST.

- The login credentials of the taxpayer (Username and password) must be valid.

- The taxpayer should have filed Form GSTR-9 (Annual Return) for that financial year.

- The taxpayer’s business must have an aggregate turnover exceeding Rs.5 crore.

53rd GST Council Meeting Updates for Annual Return Form

- The 53rd GST Council has announced the relaxations provided in FY 2023-24 for FORM GSTR-9 and FORM GSTR-9C. This includes the exemption from filing the annual return for taxpayers with an aggregate annual turnover of up to two crore rupees. The Council has made these changes to ease the compliance burden on smaller taxpayers.

GST Burden Reduced for FY 2023-24

| Sales | GSTR 9 | GSTR 9C |

|---|---|---|

| Up to 2 Cr | Optional | N/A |

| More than 2Cr. – 5 Cr | Filling is mandatory | Optional (Benefit Given) |

| More than 5Cr | Filling is mandatory | Filling is mandatory |

How Many Types of GST Audits are There?

Turnover-Based GST Audit: CA or the cost accountant used to implement it and the CA is arranged by the assessee they shall execute the audit if the turnover of the assessee is more than Rs 5 cr under the CGST act, then he shall need to get his accounts audited through the same people.

Normal Audit Under GST: It gets executed through the commissioner of the CGST/SGST or any Officer who has been permitted by the commissioner. The audit in these types of cases will get executed by giving 15 days’ notice before the commissioner.

Special GST Audit: The audit beneath this shall be taken by the CA or the cost accountant who gets appointed through the commissioner. To execute the audit the professional needs to get the order of the Deputy or Assistant Commissioner and indeed the permission of the commissioner.

Steps to generate form GSTR-9C JSON file from the offline utility?

Step 1: Log in to the GST portal and download the GSTR-9 form.

Step 2: Next, download the GSTR-9C tables derived from GSTR-9.

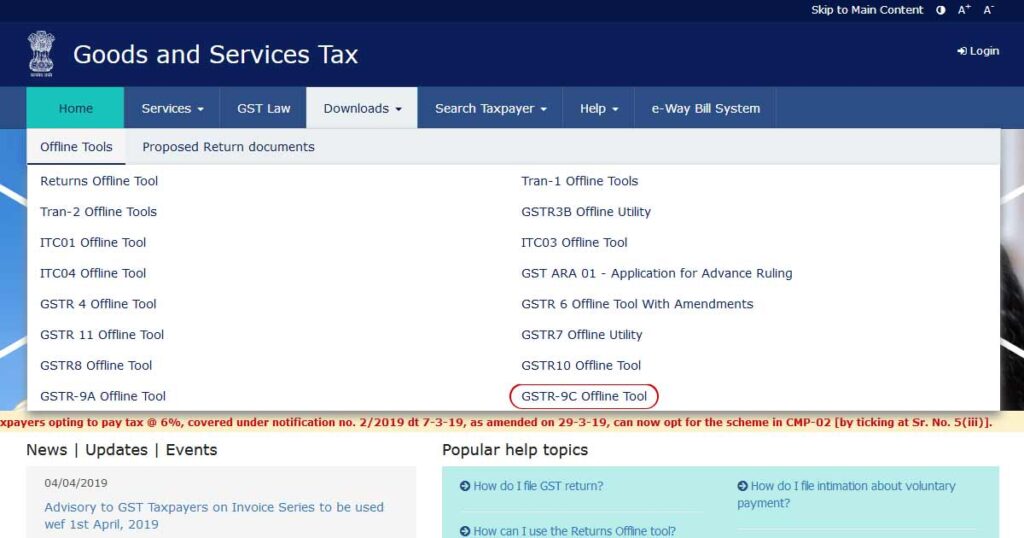

Step 3: The GSTR-9C Offline Tool must also be downloaded. This may be done from the downloads tab by selecting “Offline Tools”, and then selecting “GSTR-9C Offline Tool”.

Step 4: With the help of the GSTR-9C Offline Tool, the following steps may be done to prepare the GSTR-9C:-

- Open the GSTR Offline Utility Worksheet and then feed in the relevant data into the tables on the worksheet.

- To then view the draft version of Form GSTR-9C, the preview PDF file has to be generated.

- Once this is done, the JSON file can be generated.

Steps to file the form GSTR-9C on the GST portal

Step 1: Once the generated JSON file is uploaded on the GST portal, the user may then proceed towards adding the financial statements such as the balance sheet, profit and loss statement and other necessary documents after the necessary verification.

Step 2: The documents to be uploaded must be uploaded in PDF format. The file size limit is 5 MB per file and a maximum of 2 files can be uploaded in each section.

Step 3: At the time of uploading the necessary documents, the “SAVE” button must be clicked on after the upload of each document which shows the status as “Processed”. If the “SAVE” button is not clicked with each upload, an error message will be displayed if the user clicks on “PROCEED TO FILE”.

Step 4: The “PROCEED TO FILE” button will be enabled only once the following documents are successfully uploaded:

- Generated JSON file

- Balance Sheet in the PDF format

- Profit and Loss Account in the PDF Format

Step 5: The user can choose to view the draft of the GSTR-9C by clicking on the “PREVIEW DRAFT GSTR-9C (PREVIEW)” button.

Step 6: Clicking on the “PROCEED TO FILE” button will then take the user to the verification page. Once the verification details are confirmed, the “FILE GSTR-9C” button will be enabled, indicating that it is the final step where the form is ready to be filed once the user clicks on it.

FAQs

Does ‘aggregate turnover’ deals with topics such as stock transfers/ cross charges effected between branches located in two different states?

Aggregate Turnover has been defined in Section 2(6) of CGST/ SGST Act and the definition of aggregate turnover includes ‘inter-state supplies of a person having the same PAN’. Thus, we see that stock transfers/ cross-charges of services provided from a branch, located in one state to a branch located in another state is included in the definition of Aggregate turnover of the related branch supplying goods/ services.

Should the Form GSTR 9 and Form GSTR 9C get filed separately?

As per Section 44(2) of the CGST/ SGST Act 2017, a Registered person is required to file his Annual return in Form GSTR 9 along with this he has to provide a reconciliation statement through Form GSTR 9C. Thus we see, Form GSTR 9C is required to be filed along with Form GSTR 9 where the turnover exceeds Rs. 2 crores.