Key Tax Provisions for AY 2026-27

1. Revised Tax Slabs Under Section 115BAC (New Regime)

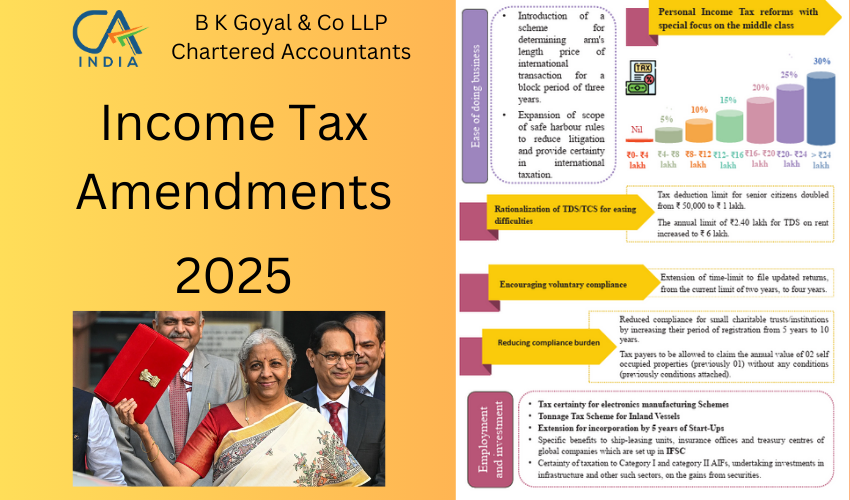

For AY 2026-27, the default tax regime under Section 115BAC will apply unless a taxpayer opts for the old tax regime. The revised tax slabs are as follows:

| Total Income | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

What’s New?

What’s New?

- The income slab up to ₹4,00,000 is now tax-free, increasing from ₹3,00,000 in AY 2025-26.

- Additional slabs have been introduced up to ₹24,00,000 before the 30% tax rate applies.

Surcharge Limits Under Section 115BAC

- The surcharge on income including dividends or long-term capital gains (under Sections 111A, 112, and 112A) is capped at 15%.

- For associations of persons (AOPs) consisting only of companies, the surcharge is similarly capped.

2. Increased Rebate Under Section 87A

For resident individuals, the rebate limit under Section 87A has been increased for AY 2026-27:

| Total Income (₹) | Maximum Rebate |

|---|---|

| Up to ₹12,00,000 | ₹60,000 |

What’s New?

- Earlier, the rebate was only available for incomes up to ₹7,00,000 with a maximum limit of ₹25,000.

- Now, income up to ₹12,00,000 will enjoy tax relief under this rebate provision.

However, the rebate does not apply to incomes taxed under special rates (such as capital gains under Sections 111A, 112, or 112A).

3. TDS & Advance Tax Changes for FY 2025-26 (Applicable from AY 2026-27)

TDS on Salaries & Advance Tax Computation

- From AY 2026-27, TDS on salaries and advance tax payments will follow the new Section 115BAC tax slabs mentioned earlier.

- TDS on insurance commission has been reduced from 5% to 2%, effective April 1, 2025.

Marginal Relief on Surcharge & Cess

- Surcharge rates remain unchanged, but marginal relief provisions have been rationalized to prevent excessive tax burdens when a taxpayer crosses an income threshold.

- Health & Education Cess at 4% continues to apply, but there is no marginal relief on this cess.

Key Tax Provisions for AY 2025-26

1. Income Tax Rates for Regular Taxpayers

For AY 2025-26, taxpayers can choose between:

- The default Section 115BAC (New Regime)

- The old regime (as per Part I of the First Schedule)

(a) Tax Slabs Under Section 115BAC (Old Rates)

| Total Income (₹) | Tax Rate |

|---|---|

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 to ₹7,00,000 | 5% |

| ₹7,00,001 to ₹10,00,000 | 10% |

| ₹10,00,001 to ₹12,00,000 | 15% |

| ₹12,00,001 to ₹15,00,000 | 20% |

| Above ₹15,00,000 | 30% |

(b) Tax Slabs Under Regular (Old) Regime

| Category | Slab (₹) | Tax Rate |

|---|---|---|

| Individuals & HUFs (<60 Yrs) | Up to ₹2,50,000 | Nil |

| ₹2,50,001 to ₹5,00,000 | 5% | |

| ₹5,00,001 to ₹10,00,000 | 20% | |

| Above ₹10,00,000 | 30% | |

| Senior Citizens (60-79 Yrs) | Up to ₹3,00,000 | Nil |

| Super Senior Citizens (80+ Yrs) | Up to ₹5,00,000 | Nil |

2. Surcharge & Cess for AY 2025-26

For individuals with income exceeding ₹50 lakh, surcharge rates are:

- ₹50 lakh – ₹1 crore: 10%

- ₹1 crore – ₹2 crore: 15%

- ₹2 crore – ₹5 crore: 25%

- Above ₹5 crore: 37% (unless opting for Section 115BAC, where the max is 25%)

Health & Education Cess:

- A uniform 4% is applied on total tax payable (including surcharge).

3. Rebate Under Section 87A for AY 2025-26

- For total income up to ₹7,00,000 (under Section 115BAC) → Max rebate of ₹25,000

- For income up to ₹5,00,000 (under the old regime) → Full tax rebate

Conclusion

The Finance Bill, 2025 has introduced major changes to the income tax regime to simplify tax compliance and provide relief to taxpayers. Here are the key takeaways:

New Tax Regime (115BAC) is the default from AY 2026-27 Tax-free income increased from ₹3,00,000 to ₹4,00,000 in AY 2026-27 Rebate under Section 87A extended up to ₹12,00,000 in AY 2026-27 Lower TDS rates on insurance commissions (5% to 2%) from FY 2025-26 Surcharge on dividend/capital gains capped at 15% under 115BAC

New Tax Regime (115BAC) is the default from AY 2026-27 Tax-free income increased from ₹3,00,000 to ₹4,00,000 in AY 2026-27 Rebate under Section 87A extended up to ₹12,00,000 in AY 2026-27 Lower TDS rates on insurance commissions (5% to 2%) from FY 2025-26 Surcharge on dividend/capital gains capped at 15% under 115BAC

Taxpayers should review these updates carefully and plan their tax filings accordingly. Consulting a tax professional can help optimize tax savings under the new rules.

For more details, refer to the official text of the Finance Bill, 2025.