ITR U or Updated Income Tax Return form is a rescue for those who have not filed their ITR or missed or incorrectly reported income in previous returns. ITR-U is a form that allows taxpayers to correct errors or omissions on their ITRs up to four years (as announced in Budget 2025) from the end of the relevant assessment year to update their return. These four years are calculated from the end of the relevant assessment year.

For instance, if you have missed filing ITR for AY 2022-23 (FY 2021-22), the last date to file an updated return is 31st March 2027. Missing this last chance can lead to legal consequences. File ITR-U.

Regardless of whether the taxpayer has filed an original, belated, or revised ITR or has completely missed filing the ITR in a specific financial year, he/she can file an ITR-U upto 2 years of the relevant assessment year. Please note that ITR-U filing for AY 2024-25 has started from 1st January 2025.

What is ITR-U?

ITR-U or Updated Income Tax Return, is a form that allows taxpayers to update their ITRs by correcting errors or omissions or allows a taxpayer to file ITR if they have not filed ITR within the due date and also missed to file the belated return, within two years from the end of the relevant assessment year. For example, if you filed an ITR for AY 2023-24 and missed the revised/belated return filing window, you can file an ITR-U after the end of the assessment year, i.e. 31 March 2024 but within two years from there, i.e. 31 March 2026. Please note that ITR-U filing for AY 2023-24 has started from 1st January 2024.

Section 139(8A) under the Income Tax Act allows you a chance to update your ITR within two years. Two years will be calculated from the end of the year in which the original return was filed. ITR-U was introduced to optimise tax compliance by taxpayers without provoking legal action.

Who is Eligible to File Form ITR-U?

Any taxpayer can file an updated return u/s 139 (8A) whether he has furnished/not furnished an original return, revised return, or belated return in case of any omission, error, or wrong statement in his earlier return of income.

An Updated Return can be filed if:

- Return previously not filed

- Income not reported correctly

- Wrong heads of income chosen

- Reduction of carried forward loss

- Reduction of unabsorbed depreciation

- Reduction of tax credit u/s 115JB/115JC

- Wrong rate of tax

Who is Not Eligible to File Form ITR U u/s 139 (8A)?

- Updated return is already filed

- For filing nil return/loss return

- For claiming/enhancing the refund amount.

- When updated return results in lower tax liability

- Search proceeding u/s 132 has been initiated against you

- A survey is conducted u/s 133A

- Books, documents or assets are seized or called for by the Income Tax authorities u/s 132A.

- If assessment/reassessment/revision/re-computation is pending or completed.

- If there is no additional tax outgo (when the tax liability is adjusted with TDS credit/ losses and you do not have any additional tax liability, you cannot file an Updated ITR)

- Note: If the loss or any part thereof carried forward or unabsorbed depreciation carried forward or tax credit carried forward is to be reduced for any subsequent previous year as a result of furnishing an updated return of income for a previous year, an updated return is required to be furnished for each subsequent previous year.

ITR-U Filing Deadline: Time Limit & Due Dates

The time limit to file an updated return u/s 139 (8A) is extended to 4 years from 2 years starting April 2025 (as announced in budget 2025-26) from the end of the relevant assessment year. Hence, the updated return of FY 23-24 (AY 2024-25) can be filed till 31st March 2029.

For example,

| Assessment Year | Last Date of Updated ITR Filing |

|---|---|

| FY 2021-22 (AY 2022-23) | 31 March 2027 |

| FY 2022-23 (AY 2023-24) | 31 March 2028 |

| FY 2023-24 (AY 2024-25) | 31 March 2029 |

FAQs

How to File Form ITR-U?

As per the Income tax rules, the updated return (ITR-U) has to be furnished along with an updated version of the applicable ITR form (ITR 1 – 7).

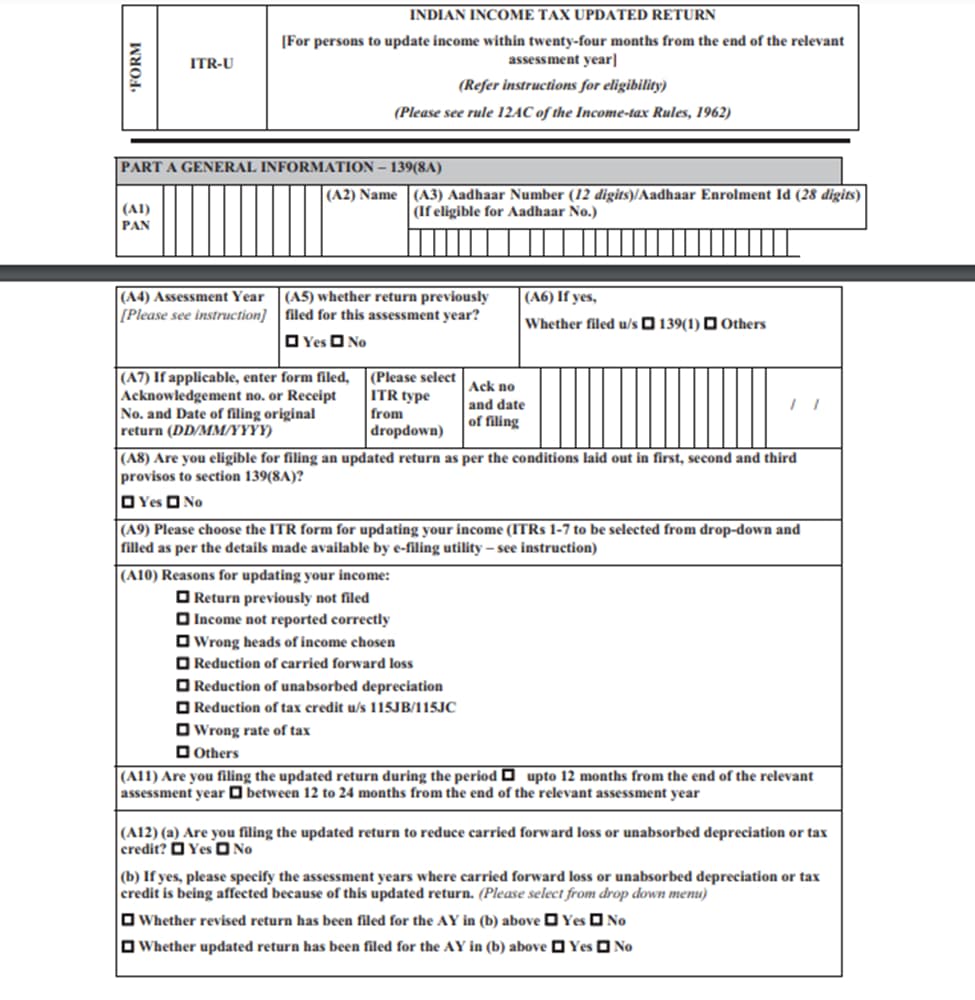

ITR-U seeks the following additional details from the taxpayers:

- PAN

- Aadhaar Number

- Assessment Year

- Whether return previously filed for this assessment year? (Yes/No)

- If yes, Whether filed u/s 139(1) Others

- If applicable, enter form filed, Acknowledgement no. or Receipt No. and Date of filing the original return (DD/MM/YYYY)

- Are you eligible to file an updated return? i.e., a person is not falling in such circumstances wherein an updated return can’t be filed.

- Selecting the ITR form for filing an updated return

- Reasons for updating income. This includes reasons such as returns previously not filed, income not reported correctly, wrong heads of income chosen, etc.

- Are you filing an updated return within 12 months from the end of the relevant AY or between 12 to 24 months from the end of the relevant AY?

- Are you filing an updated return to reduce carried forward loss, unabsorbed dep., or tax credit?

Part B – Computation of updated income and tax payable (ITR-U)

- 1 (A) Head of income under which additional income is being returned as per Updated Return

- 1 (B) Total income as per last valid return (only in cases where the Income Tax Return has previously been filed)

- Total income as per Part B-TI

- The amount payable, if any (To be taken from the ―Amount payable of Part B-TT of the updated ITR)

- Amount refundable, if any (To be taken from ―Refund‖ of Part B-TTI of the updated ITR

- The amount payable on the basis of last valid return (only in applicable cases)

- 6. (i) Refund claimed as per last valid return if any

- 6. (ii) Total Refund issued as per last valid return, if any (including interest u/s 244A received

- Fee for default in furnishing return of income u/s 234F

- Regular Assessment Tax, if any

- Aggregate liability on additional income

- Additional income-tax liability on updated income [25% or 50% of (9-7)]

- Net amount payable (9+10)

- Tax paid u/s 140B

- Tax due (11-12)

- Details of payments of tax on updated return u/s 140B

- Details of payments of Advance Tax / Self-Assessment Tax / Regular Assessment Tax, credit for which has not been claimed in the earlier return (credit for the same is not to be allowed again under section 140B(2) )

- Note: Credit for the above is not to be allowed again under section 140B(2)

- Relief u/s 89, which is not claimed in earlier return [relief for the same is not to be allowed under section 140B(2)]

ITR-U Late Filing Penalty – How Much Extra Tax Will You Pay?

Starting April 2025, the timeline for filing an Updated Income Tax Return (ITR-U) has been extended from two years to four years. Late filing of the ITR-U incurs penalties: If filed within 12 months, an additional 25% of the tax and interest is charged; within 24 months, it’s 50%; within 36 months, it’s 60%; and within 48 months, it’s 70%. The new timeline gives taxpayers more time to stay compliant, but filing early will help avoid these extra costs.

For example:-

| ITR-U filed within | Additional Tax |

|---|---|

| 12 months from the end of the relevant AY | 25% of additional tax (tax + interest ) |

| 24 months from the end of the relevant AY | 50% of additional tax (tax + interest ) |

| 36 months from the end of the relevant AY | 60% of additional tax (tax + interest ) |

| 48 months from the end of the relevant AY | 70% of additional tax (tax + interest ) |