A merchant discount rate is the rate levied on debit and credit card transactions to a merchant for the payment processing services. Before accepting debit and credit cards as payment the merchant must set up this service and agree to the rate. The merchant discount rate is a price that merchants must take into consideration when calculating their company’s overall costs.

Most retailers will expect to pay a fee of 1% to 3% for each transaction’s payment processing. Usually, local merchants and e-commerce vendors will have different fees and service-level agreements. The payment processors have well-established systems and fee schedule arrangements in place to accommodate all forms of vendor payments.

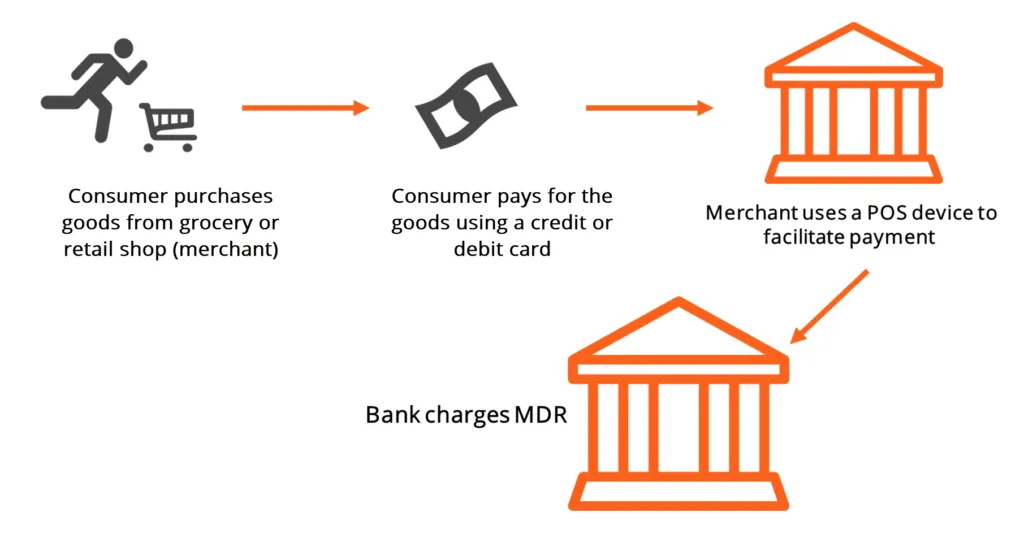

What is Merchant Discount Rate (MDR)?

The Merchant Discount Rate (MDR) is a fee charged by payment processing companies to merchant companies for each credit or debit card transaction made by customers. This fee typically ranges from 1% to 3% of the transaction amount.

The MDR fees cover a variety of costs, including:

- Payment processor fee: These fees are charged by payment processors (companies that handle transactions between merchants and banks ) for their services.

- Interchange fee: These are fees charged by card issuers (banks) to merchants for processing transactions.

- Assessment fee: These are fees charged by card networks (like Visa, RuPay and Mastercard) to merchants for using their payment processing services.

- Markup fee: These are fees that is divided among the different entities involved in the transaction

- Additional fees: Some payment processors may charge additional fees for services like fraud prevention, chargeback handling, and customer support.

MDR and Digital Economy

Moving rapidly towards Digital Economy, the Ministry of Finance (MoF) and the RBI focused on the less-cash economy. To promote a less-cash economy, MoF instructed banks to provide a platform to increase the usage of cards and install Point-of-Service (PoS) terminals. The primary importance of implementing digital transaction is to reap the benefits and set standards in cross-border trade. As a result, providing technological, equipment, infrastructure and skilled workers are required. In exchange for the services being provided for the digital transaction, the charges become applicable for the merchant.

Member Involved in MDR

Bank- The bank approves and provides a debit card or credit card for the account holders.

Merchant-Accepts to transact with the debit or credit card for the goods sold or services provided. To transact, the merchant sets up an account with the processor to accept the cards. For the services rendered by the processor, the merchant pays the agreed fee.

Processor– Processors provide support to manage complex transaction procedures. They provide services for the digital transaction by creating an account for the merchant.

FAQs

Merchant Discount Rate (MDR) Charges in India for 2025?

Payment Method | Card Network | MDR Percentage on Credit Card | MDR Percentage on Debit Card |

| Card Payments | Visa | 1% to 3% | 0.25% to 1% |

| Card Payments | Mastercard | 1% to 3% | 0.25% to 1% |

| Card Payments | RuPay | 1% to 3% | 0.25% to 1% |

| UPI Payments | UPI | 0.25% to 0.75% | 0.25% to 0.75% |

| Net banking | Various banks | 0% to 0.25% | 0% to 0.25% |

| Mobile Wallets | Various providers | 0% to 1% | 0% to 1% |

What is the Purpose of MDR?

1. Covering Payment Processing Costs

The MDR structure is designed to cover various costs associated with payment processing, including:

- Interchange fees charged by card issuers

- Network fees imposed by card networks

- International transaction fees for cross-border payments

2. Incentivizing Card Usage:

- By establishing clear fees, the MDR makes it more attractive for merchants to accept card payments. This increased acceptance benefits consumers by offering a wider range of payment options.

- It also leads to higher sales volumes and improved cash flow management for businesses.

3. Managing Risk

- The MDR includes fees that help mitigate payment risks, such as chargebacks and fraud.

- This allows merchants to set aside funds for dispute resolution and fraud prevention measures.

4. Rewarding Cardholders

- A portion of the MDR is used to fund cardholder rewards and benefits programs.

- This incentivizes card usage and fosters customer loyalty by offering perks like cashback, points, and other benefits.

5. Supporting Payment Infrastructure

- The MDR contributes to the development and improvement of payment technologies, enhancing security and user experience.

- By funding these advancements, the MDR helps create a more efficient and robust payment ecosystem.

6. Driving E-commerce Growth:

- The MDR supports the integration of various payment methods, making it more convenient for online shoppers.

- This helps drive the growth of e-commerce and digital payments.