When a company faces insolvency or enters liquidation, one of the first aspects under review is the conduct of its directors prior to the financial collapse. This scrutiny includes assessing any transactions that might have unfairly benefited certain creditors—these are termed preferential payments. In such cases, the role of the liquidator becomes crucial, as they must ensure fair distribution of the company’s assets to all creditors, giving precedence to certain dues as laid out under Section 327 of the Companies Act, 2013.

When a company faces financial distress and ultimately goes into administration or liquidation, its financial affairs are closely scrutinized to determine whether any wrongful or illegal actions were undertaken by the directors prior to insolvency. One critical aspect of this process is examining whether preferential payments were made to certain creditors over others. The role of the liquidator in such cases is to ensure the fair and lawful distribution of the company’s assets while maximizing returns for all creditors.

One of the key provisions governing the distribution of assets in liquidation is Section 327 of the Companies Act, 2013, which lays down the framework for preferential payments. It outlines which creditors are entitled to receive priority payments before settling the claims of other unsecured creditors. This provision applies to all cases of winding up except where liquidation occurs under the Insolvency and Bankruptcy Code, 2016 (IBC), in which case the IBC rules prevail.

KEY POINTS

1.

Preferential Payments: Section 327 prioritizes dues

like taxes, wages (4 months), and social security during winding-up.

2.

Limited Scope: Applies only if assets remain

after Section 326; not applicable under IBC, 2016.

3.

SC Verdict (2023): Upheld Section 327(7),

reinforcing IBC’s priority rules over Companies Act.

4.

Waterfall Mechanism: Ensures fair creditor payout;

secured creditors and workmen dues rank equally.

5.

Workmen Protection: PF, pension, and gratuity are

excluded from liquidation; 24-month dues protected.

Who qualifies as Preferential Creditors?

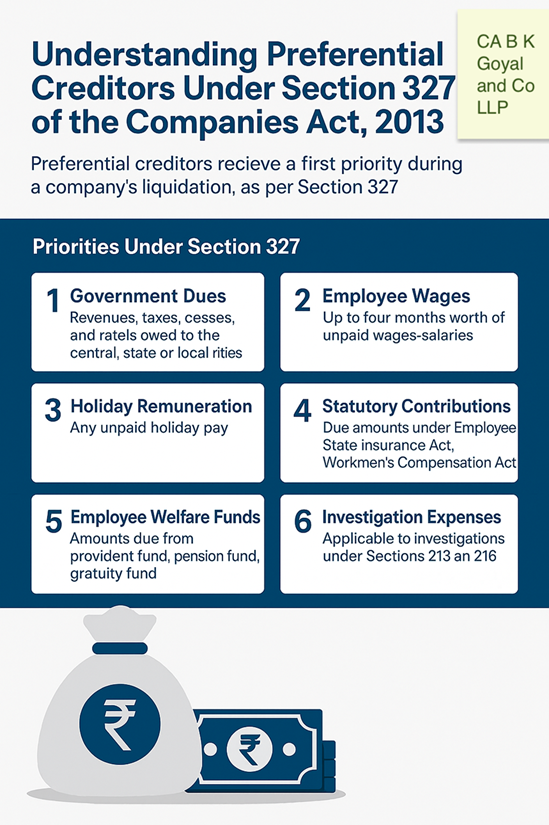

Preferential creditors are those individuals or entities that are legally entitled to be paid before other unsecured creditors when a company is liquidated. Section 327 establishes a priority order for such payments to ensure that certain obligations, especially those owed to employees and government agencies, are settled first. The following categories of creditors are included under preferential payments:

- Government Dues: Any revenue, taxes, cesses, or rates payable to the central, state, or local government that became due within one year before the winding-up order must be settled on priority.

- Employee Wages and Salaries: Employees’ wages and salaries for up to four months, provided they were earned within the 12 months preceding the winding-up order, are considered preferential.

- Accrued Holiday Remuneration: Any unpaid holiday wages due to an employee or their legal heirs must be paid. Unlike wages, there is no time limitation on holiday remuneration claims.

- Contributions to Employee State Insurance (ESI): Any outstanding amounts due for contributions under the Employee State Insurance Act, 1948, in the last 12 months are also given preferential treatment.

- Compensation for Workmen: Compensation owed under the Workmen’s Compensation Act, 1923, for injuries, disablement, or death of an employee must be paid on priority.

- Provident Fund, Pension Fund, and Gratuity Dues: Any contributions due to employees’ provident fund, pension fund, or gratuity fund maintained by the company are protected under this section.

- Expenses of Investigation: If any investigation was conducted under Section 213 or 216 of the Companies Act, 2013, and the company is liable for the investigation costs, those expenses are also considered preferential payments.

Key Highlights of Section 327 towards Preferential Creditors

- Preferential creditors have the first right to repayment when a company goes bankrupt.

- Section 327 operates in conjunction with Section 326, which means that if all assets are exhausted under Section 326 (which protects the rights of workmen), then no distribution occurs under Section 327.

- The provisions of Section 327 do not apply to companies undergoing liquidation under the Insolvency and Bankruptcy Code, 2016.

- Unpaid wages and tax obligations are of the highest priority for the liquidator.

- Unsecured creditors face the highest risk of non-repayment, as they are paid only after all secured and preferential creditors have been satisfied.

Implications for Directors and Creditors

From a director’s perspective, ensuring compliance with these provisions is essential to avoid potential legal consequences. If it is found that directors intentionally prioritized certain creditors over others outside the prescribed legal framework, they may be held personally liable for misconduct. Moreover, any fraudulent preference given to a creditor could be challenged and reversed by the court.

For creditors, understanding their position in the liquidation hierarchy is crucial. While secured creditors have the first right to claim proceeds from asset sales, preferential creditors come next, followed by unsecured creditors. This structure significantly impacts the ability of unsecured creditors to recover debts owed to them, often leaving them with little to no reimbursement after the liquidation process is complete.

Legal Interplay with Section 326 and the IBC

It’s important to note that the provisions of Section 327 operate subject to Section 326. If the company’s assets are exhausted during distribution under Section 326, then the provisions of Section 327 do not apply.

Further, Section 327 is not applicable when a company is liquidated under the Insolvency and Bankruptcy Code, 2016 (IBC). In such scenarios, the IBC’s Section 53 “waterfall mechanism” dictates the order of distribution.

The Moser Baer Case: Upholding the Constitutionality of Section 327(7)

In Moser Baer Karamchari Union v. Union of India (2023), workmen unions contested Section 327(7) for not prioritizing their dues during IBC-led liquidation. They argued that this exclusion violated the principles laid out in Sections 326 and 327 of the Companies Act.

However, the Supreme Court dismissed these petitions, affirming that the amendment introducing Section 327(7) was necessary to align the Companies Act with the IBC framework. The judgment reinforced that the waterfall mechanism under Section 53 of the IBC is constitutionally valid, ensuring a fair and systematic distribution of assets among creditors based on their contribution and risk exposure.

Why This Judgment Matters

1. Protecting the Integrity of the Waterfall Mechanism

The Court recognized that the waterfall model is essential for achieving economic balance during liquidation. It prioritizes creditors based on the level of financial risk they undertook. For example, secured creditors who relinquish their security interest are next in line after resolution and liquidation costs, as their investment involved higher financial risk. This principle enhances investor confidence and maintains legal certainty.

2. Safeguarding Workmen’s Rights

Although workmen dues don’t always take top priority, the IBC still offers them considerable protection. Section 36(4)(a) of the IBC ensures that workmen’s provident fund, pension, and gratuity funds are kept out of liquidation assets. Furthermore, Regulation 21A of the Liquidation Process Regulations mandates that secured creditors must contribute to the insolvency and liquidation costs, including dues to workmen, within 90 days if they realize their secured interests under Section 52.

Additionally, workmen dues are calculated for a period of 24 months preceding the liquidation commencement date, offering them a broader timeframe for claims—much earlier than the traditional winding-up date.

Aligning with Previous Precedents

The judgment echoes earlier Supreme Court decisions, including Sunil Kumar Jain v. Sundaresh Bhatt, where the Court affirmed that workmen’s benefits like provident and pension funds are protected and excluded from the liquidation pool. Such consistency in rulings strengthens the legal framework surrounding insolvency.

Conclusion

In a dynamic and growing economy like India, the Insolvency and Bankruptcy Code plays a pivotal role in strengthening the credit ecosystem, ensuring timely resolution of distressed assets, and balancing the interests of all stakeholders. This ruling by the Supreme Court sends a strong message—individual interests cannot override the collective good. By upholding the waterfall mechanism and reinforcing the Code’s objectives, the Court has ensured fairness, transparency, and efficiency in the liquidation process.

While every stakeholder may face some losses during liquidation, the law ensures that no group is left entirely unprotected, especially vulnerable segments like workmen. As the Court aptly stated, “some sacrifices have to be made for greater good.”

About the Author

This article is written by Advocate Shruti Goyal. Advocate Shruti Goyal has done her LLB from Dr Bhim Rao Ambedkar Law University and a Law graduate currently practicing as an Advocate in High Court and Supreme Court of India.