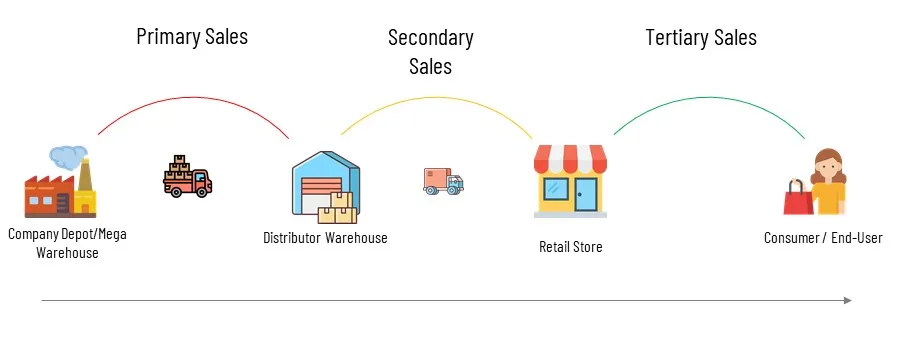

In the supply chain, before a product reaches to end customers, it will first reach at least three stakeholders: a manufacturing company or a national supplier, distributor, and retailer. The sales transactions from each level of stakeholders have different names: primary, secondary, and tertiary sales.

Primary Sales

Primary sales refer to sales from the first stakeholder—a manufacturing company or national supplier to a distributor. In other words, the transaction between a manufacturing company/national supplier to a distributor in one city/state/region called “primary sales” transaction. A company makes an invoice of the product at distributor price and the revenue from the transaction is the net revenue of the company.

Factors Determining Primary Sales

Primary sales in a company are determined by various factors, including:

- The company’s popularity

- The company’s distribution network, how large it is

- The secondary sales

- The consumption pattern of a certain product, whether it is slow or fast.

Those factors determine a Mystery Shopping company’s primary sales. The primary sales contribute to the company’s profits and revenue, thus, it is the main focus of the company. However, primary sales must be done with secondary sales to make it effective.

Secondary Sales:

After a product reaches a distributor, it will be invoiced to a retailer, thus, the transaction is called secondary sales. Distributors will keep its margin and set the product at dealer/retailer price.

In the secondary sales, a distributor sells the product to a retailer. Nevertheless, a distributor can also sell it directly to an end customer. In modern retail, it works on the two-tier concept where the primary sales are from the company to the retail outlet and the secondary sales are from retail outlets to customers.

Factors Determining Secondary Sales

Secondary sales are determined by several key factors, including:

- The company’s popularity and brand equity of the company

- Stock availability

- The involvement of distributors and retailers

- Credit and trade promotions, the better trade promotions, the higher the sales are.

Secondary sales are more important than the primary sales to a manufacturer industry because it affects the primary sales though it is not the responsibility of the manufacturer but the distributors/retailers. At this point, if the distributors do not show well performance, the companies have to find new distributors will better performance. This will ensure the fast movement of the company. In the final level of sales are tertiary levels. Tertiary sales are typically observed only if it’s on the three-tier distribution. For example, if the company sells a distributor who sells the product directly to the customers, then the tertiary sales will not exist.

Tertiary Sales

Tertiary sales are when a retailer sells the product to an end customer. On this transaction, the product is sold at MRP (maximum retail product) or MOP (market operating price).

Tertiary sales involve end costumers which are the most important sales of all. Thus, companies should focus more on these sales to maximize their tertiary sales. If the tertiary sales are high, the secondary and the primary sales will automatically happen and these all will be done by mystery shopping.

Factors Determining Tertiary Sales:

Several key factors that determine tertiary sales are:

- Customers’ convenience to buy the product

- The marketing strategies to attract customers to make a purchase

- The company’s brand equity, the more popular the company, the more the tertiary sales will be appreciated by Market Segmentation.

- Product alternatives—a cheaper or a higher quality alternative of products

- Overall market movement.

FAQs

How do tertiary sales impact the supply chain?

Tertiary sales complete the supply chain cycle, indicating the final consumption of products and influencing future production and distribution plans.

Who is responsible for secondary sales?

Distributors or wholesalers are responsible for secondary sales, selling products to retailers or consumers.

How is primary sales different from secondary sales?

Primary sales involve transactions between manufacturers and distributors, while secondary sales occur between distributors and retailers or end consumers.

Practice area's of B K Goyal & Co LLP

Income Tax Return Filing | Income Tax Appeal | Income Tax Notice | GST Registration | GST Return Filing | FSSAI Registration | Company Registration | Company Audit | Company Annual Compliance | Income Tax Audit | Nidhi Company Registration| LLP Registration | Accounting in India | NGO Registration | NGO Audit | ESG | BRSR | Private Security Agency | Udyam Registration | Trademark Registration | Copyright Registration | Patent Registration | Import Export Code | Forensic Accounting and Fraud Detection | Section 8 Company | Foreign Company | 80G and 12A Certificate | FCRA Registration |DGGI Cases | Scrutiny Cases | Income Escapement Cases | Search & Seizure | CIT Appeal | ITAT Appeal | Auditors | Internal Audit | Financial Audit | Process Audit | IEC Code | CA Certification | Income Tax Penalty Notice u/s 271(1)(c) | Income Tax Notice u/s 142(1) | Income Tax Notice u/s 144 |Income Tax Notice u/s 148 | Income Tax Demand Notice | Psara License | FCRA Online

Company Registration Services in major cities of India

Company Registration in Jaipur | Company Registration in Delhi | Company Registration in Pune | Company Registration in Hyderabad | Company Registration in Bangalore | Company Registration in Chennai | Company Registration in Kolkata | Company Registration in Mumbai | Company Registration in India | Company Registration in Gurgaon | Company Registration in Noida | Company Registration in lucknow

Complete CA Services

RERA Services

Most read resources

tnreginet |rajssp | jharsewa | picme | pmkisan | webland | bonafide certificate | rent agreement format | tax audit applicability | 7/12 online maharasthra | kerala psc registration | antyodaya saral portal | appointment letter format | 115bac | section 41 of income tax act | GST Search Taxpayer | 194h | section 185 of companies act 2013 | caro 2020 | Challan 280 | itr intimation password | internal audit applicability | preliminiary expenses | mAadhar | e shram card | 194r | ec tamilnadu | 194a of income tax act | 80ddb | aaple sarkar portal | epf activation | scrap business | brsr | section 135 of companies act 2013 | depreciation on computer | section 186 of companies act 2013 | 80ttb | section 115bab | section 115ba | section 148 of income tax act | 80dd | 44ae of Income tax act | west bengal land registration | 194o of income tax act | 270a of income tax act | 80ccc | traces portal | 92e of income tax act | 142(1) of Income Tax Act | 80c of Income Tax Act | Directorate general of GST Intelligence | form 16 | section 164 of companies act | section 194a | section 138 of companies act 2013 | section 133 of companies act 2013 | rtps | patta chitta